I. Cathode Materials: Significant Order Revival, Strong Year-end Demand Support

In November, the production end of sodium-ion battery cathode materials performed impressively, with production up 50% MoM and 54% YoY, indicating a continuous recovery in industry prosperity. In terms of product structure, poly-anion NFPP remains the market mainstream, accounting for 76% of total production, an increase of 4 percentage points from October, further highlighting the leading effect.

The revival in orders is the core driver of this growth: on one hand, the compatibility issues between battery cell manufacturers and systems that previously plagued the industry have been properly resolved, coupled with the completion of inventory digestion by battery cell enterprises, allowing top NFPP cathode companies to restore their shipments to Q3 levels; on the other hand, as the year-end approaches, some ESS projects are accelerating installations to secure subsidy windows, directly boosting demand for NFPP cathodes.

Layered oxide O3 routes also maintained growth momentum. With the initial implementation of layered oxide technology in heavy truck projects, the demand for cathode raw material reserves continues to be released, along with stable demand from small-scale ESS applications, keeping the production of layered oxide cathodes at a high level in November. Looking ahead to December, based on current order support, expectations for sodium-ion cathode production are optimistic, with a forecasted 3% MoM growth and a 139% YoY increase.

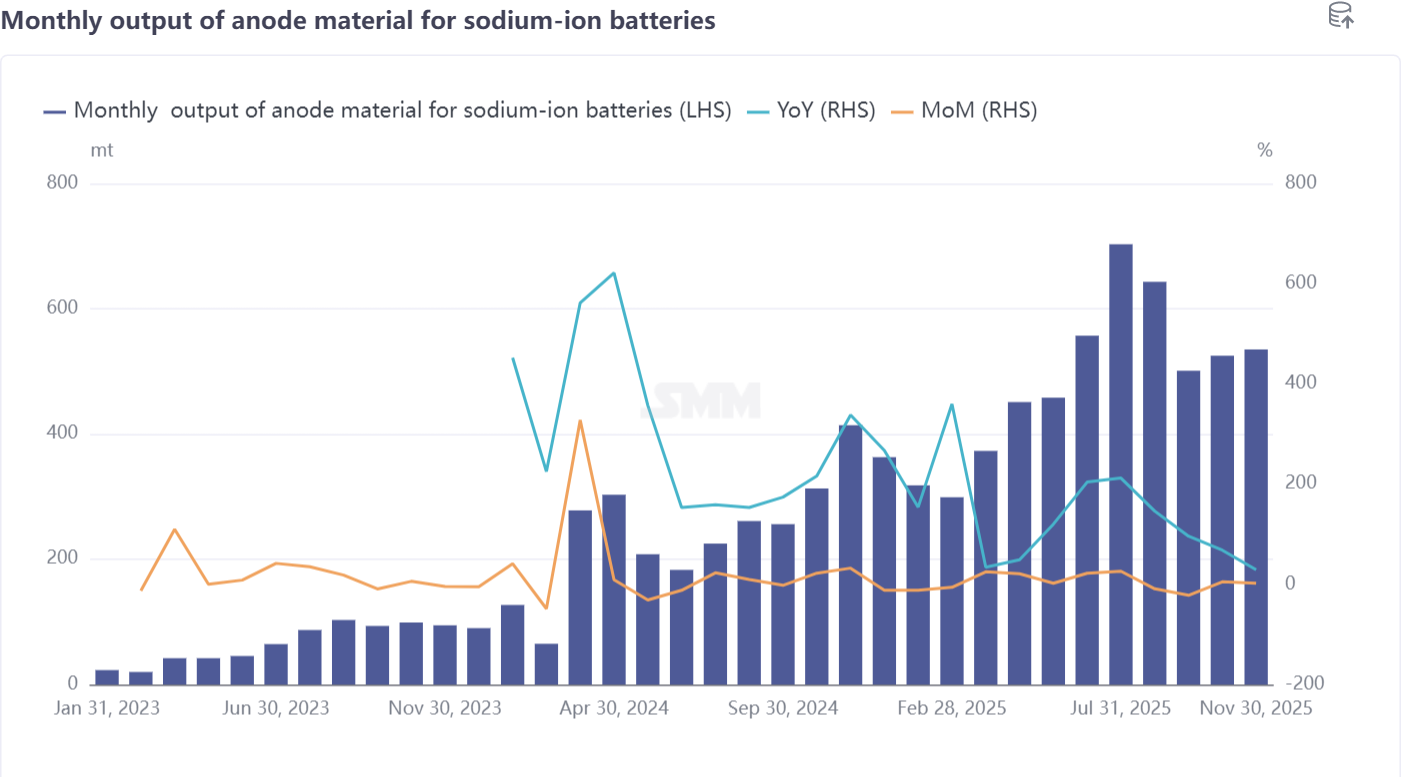

II. Hard Carbon Anode: Focus on Quality Improvement During Development Phase, High Capacity Concentration Maintained

In November, the production of sodium-ion anode materials increased 5% MoM and 68% YoY, although the growth rate was lower than that of cathodes, the effects of industry adjustments are gradually becoming evident. This month, hard carbon anode enterprises carried out a series of optimization adjustments focusing on production raw materials, cost control, and product pricing, driving marginal improvements in shipment conditions. The industry consensus is clear, the sector is still in its nurturing stage, and it is not advisable to prematurely fall into price involution; quality improvement and technological iteration remain the core directions.

The iteration of the raw material system has become a significant trend. Since 2025, influenced by the continuous rise in coconut shell carbon prices, the domestic hard carbon industry has gradually transitioned towards a bamboo-based hard carbon system to reduce cost dependency. From the application perspective, hard carbon products have formed three core scenarios: two-wheeled small power, start-stop power supply, and ESS. Different scenarios have distinct requirements for the cycle performance, low-temperature characteristics, and C-rate of hard carbon, resulting in a differentiated price system that cannot be generalized.

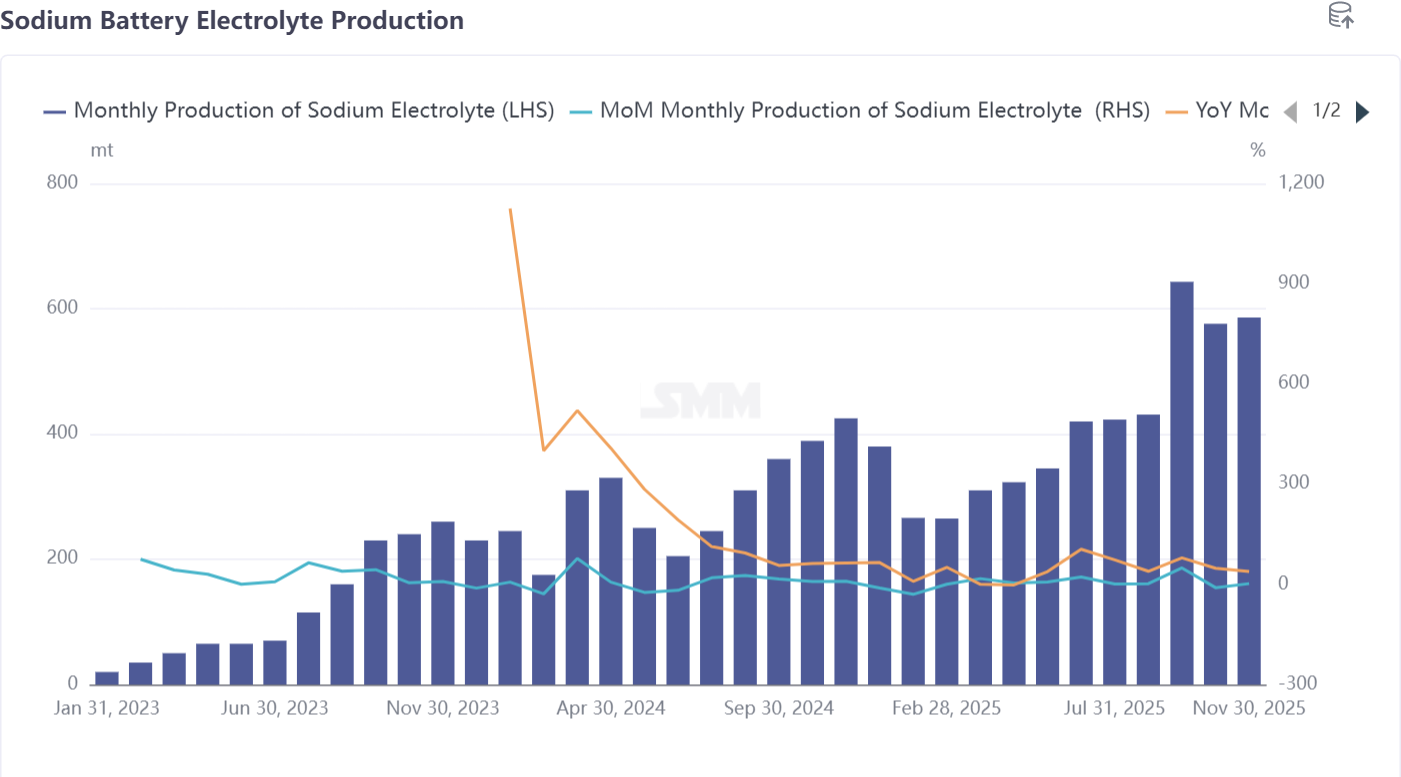

III. Electrolyte: Overall Stable Prices with Minor Cost Fluctuations from Additives

In November, sodium-ion battery electrolyte production increased by 2% MoM and 38% YoY, showing steady expansion in production scale. Prices remained stable. Compared to the sharp price surge of LiPF6, a key raw material for lithium battery electrolyte, the price of NaPF6, a critical raw material for sodium-ion battery electrolyte, remained stable, supporting industry profitability.

Cost side, minor fluctuations occurred due to price increases in some additives shared by lithium and sodium batteries, which slightly impacted sodium-ion battery electrolyte costs. However, these increases have not yet been passed on to end selling prices, and overall sodium-ion battery electrolyte prices remain stable. In terms of enterprise collaboration, sodium-ion battery electrolyte production is currently dominated by lithium battery electrolyte enterprises. Battery cell manufacturers and electrolyte producers engage in deep cooperation, enabling precise formula R&D tailored to the performance requirements of sodium-ion battery cells and enhancing product compatibility. Given the order-driven nature of the industry, electrolyte production in December is expected to decrease by 4% MoM but still increase by 48% YoY.

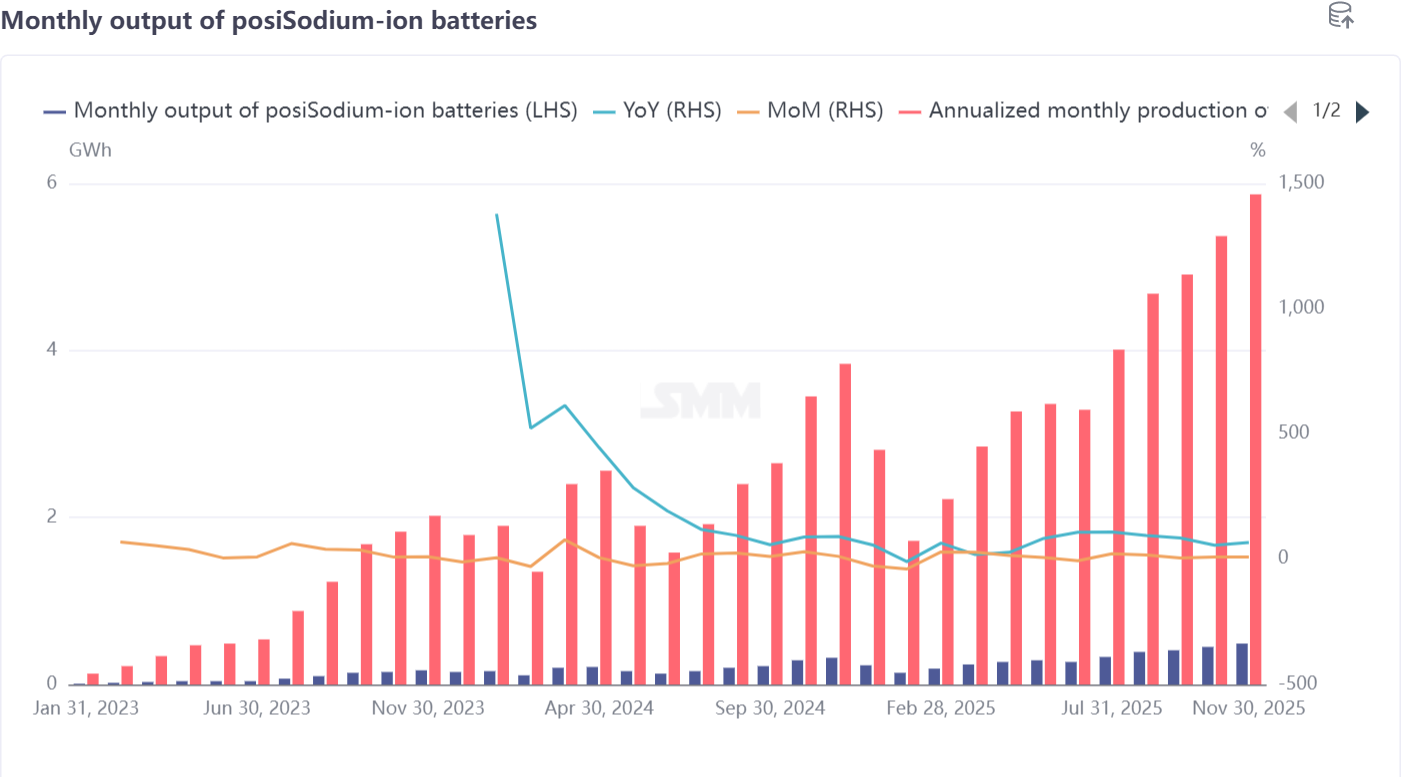

IV. Battery Cells and End-Use: Expanding Application Scenarios and Steady Growth in Production and Sales

In November, sodium-ion battery cell production increased by 9% MoM and 67% YoY, indicating strong production and sales. According to SMM survey, battery cell enterprises maintained high production schedules this month, driven primarily by rush to meet deadlines for energy storage projects. In the electric two-wheeler sector, production progress for sodium-ion battery cells significantly recovered following the implementation of solutions for problematic cells after the new national standards took effect.

End-use applications continue to broaden, serving as a core engine for industry growth: in the electric two-wheeler sector, sodium-ion battery penetration rate is about 3% in 2025, and leading battery cell producers plan to increase this proportion to 10% next year; in the start-stop power supply sector, the market currently focuses on the secondary market for replacing lead-acid batteries in internal combustion engine vehicles, with no breakthrough yet in pre-installation by OEMs in the primary market—short-term demand will still rely mainly on replacement of existing stock; additionally, exploratory efforts for sodium-ion battery cells in new scenarios such as heavy-duty trucks, extended-range plug-in hybrids, and data center backup power supplies have achieved phased progress. As December is a critical period for annual volume push, sodium-ion battery cell production outlook is positive, projected to increase by 3% MoM and 116% YoY. V. Summary of Sodium-Ion Battery Industry Chain Operations in November

In November, the sodium-ion battery industry chain demonstrated a positive trend characterized by recovering demand, simultaneous growth in production and sales, and structural optimization, with notable synergistic development across all segments. On the production side, except for hard carbon anodes, which experienced relatively moderate growth due to industrial adjustments, cathode materials, electrolyte, and battery cell production all achieved dual growth both MoM and YoY. Among them, cathode materials posted the most significant increase, up 50% MoM, reflecting strong demand-side momentum.

Demand side, multiple favorable factors converged: the year-end installation rush for ESS projects and the recovery of electric two-wheeler capacity following issue resolutions directly boosted orders for core materials and battery cells; initial deployment in new applications such as heavy-duty trucks and data centers opened up long-term growth opportunities for the industry.

Industry side, structural features became increasingly distinct: the dominance of the NFPP route in cathode materials was reinforced, hard carbon anodes shifted toward bamboo-based raw materials, and electrolyte benefited from technological spillover from lithium battery enterprises, with all segments advancing through technological iteration and cost optimization. Overall, the industry chain overcame previous bottlenecks in November, laying a solid foundation for the year-end push and development in 2026.