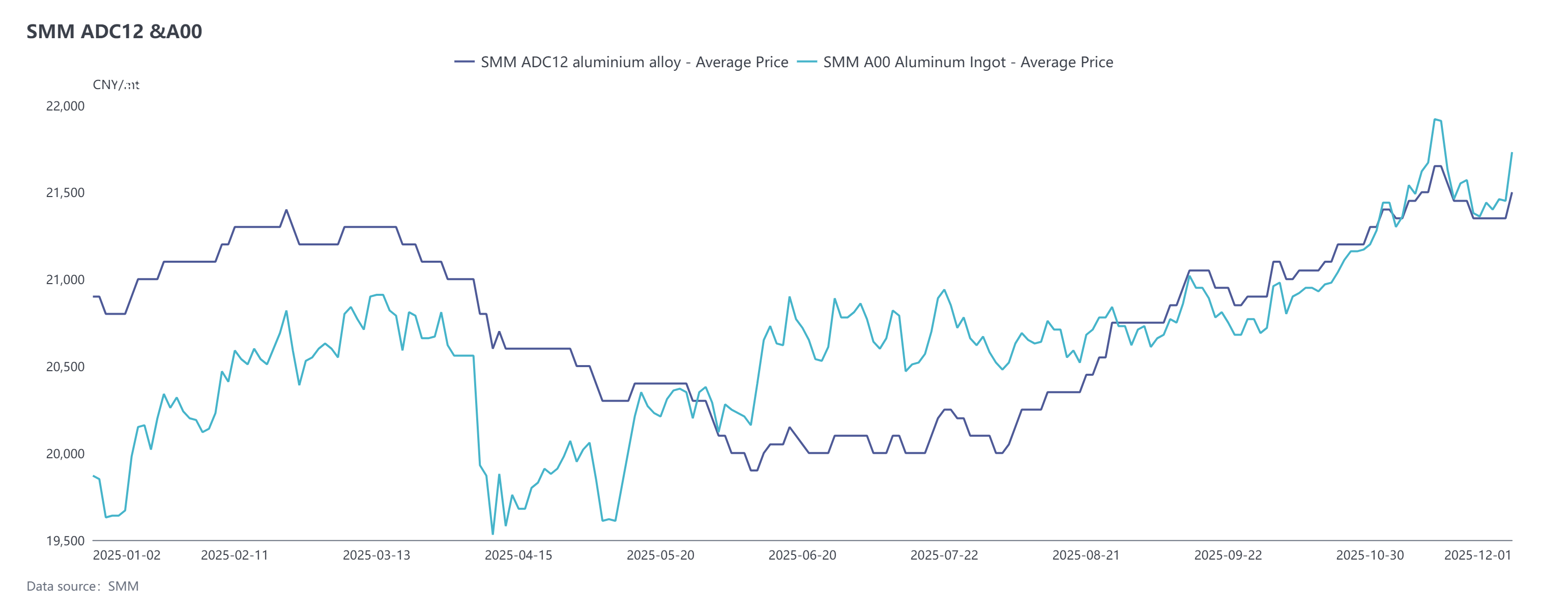

First, a review of the secondary aluminum alloy price trend in November: In the futures market, the most-traded cast aluminum alloy contract opened at 20,920 yuan/mt at the beginning of the month. Driven by macro tailwinds and capital inflows, it continued to strengthen, hitting a post-listing high of 21,390 yuan/mt in mid-month. Subsequently, as market sentiment digested, prices quickly corrected to around 20,225 yuan/mt. By month-end, prices fluctuated rangebound, with the trading range gradually narrowing, and finally closed at 20,800 yuan/mt.

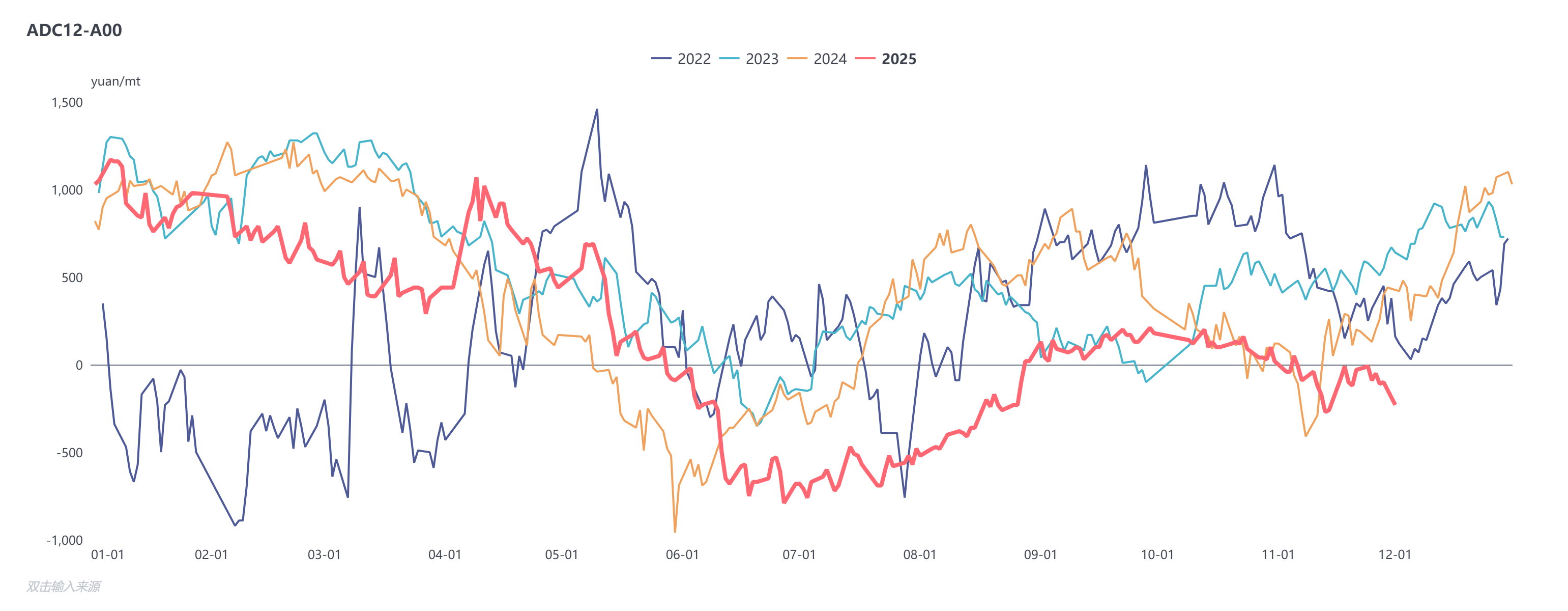

In the spot market, the SMM ADC12 price trend rose initially then fell, with overall volatility weaker than that of aluminum prices. ADC12 shifted to a discount against A00 aluminum, with the discount widening early in the month and narrowing by month-end. Later, influenced by another surge in aluminum prices in December, the discount widened again, with the price spread between the two reaching its lowest level in nearly four years. As of December 2, the SMM ADC12 offer increased by 100 yuan/mt from early November to 21,500 yuan/mt, and the average price for November was up 1.4% MoM. Throughout the month, prices were influenced by a mix of cost support and demand changes, maintaining a pattern of holding up well.

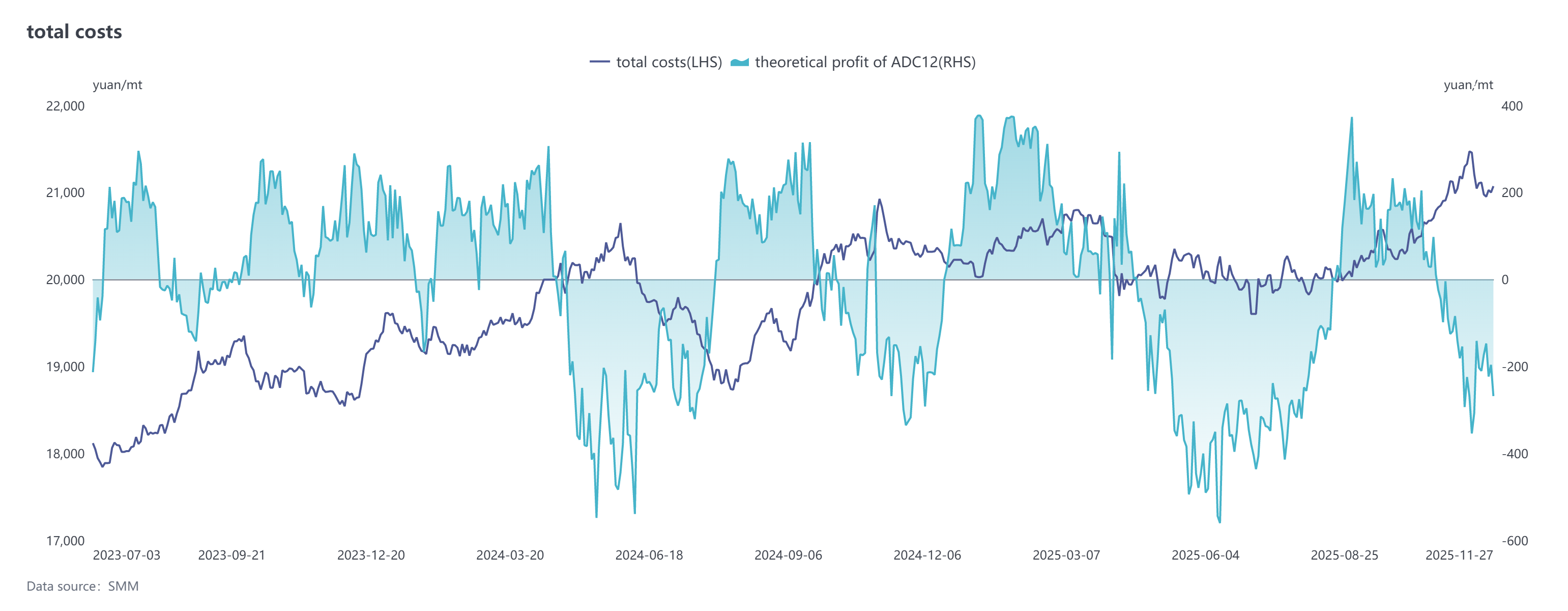

Cost side, the cost trend of secondary aluminum alloy in November was mainly driven by tight aluminum scrap supply. Spurred by the rapid rise in aluminum prices, aluminum scrap prices followed with a notable increase, causing a sharp rise in cost pressure for secondary aluminum alloy producers and pushing the industry into losses. Although subsequent aluminum price pullbacks led aluminum scrap prices to drop back slightly, due to the persistent tight supply situation and traders' reluctance to sell, cost support remained strong. In November, the per-mt cost of aluminum scrap for ADC12 rose to 19,008 yuan, up 2.4% MoM, accounting for nearly 90% of the total cost. Meanwhile, average prices of auxiliary materials such as silicon and copper, as well as natural gas prices, all rose, further pushing up the overall cost of secondary aluminum alloy. As the price increase of finished alloy ingots lagged, enterprise losses widened. Additionally, processing fees for aluminum alloy products with higher copper content, such as A380, continued to increase, with the premium over ADC12 expanding to 1,400-1,600 yuan/mt. Due to persistently high costs, enterprises generally adopted an order-based production model, largely maintaining low inventory levels.

Demand side showed divergence, with consumption resilience in end-use sectors such as automotive providing support. Particularly, expectations for year-end adjustments to the NEV purchase tax policy stimulated a concentrated release of car purchase demand, and automakers' push for sales targets drove robust order books for secondary aluminum enterprises. However, export orders remained weak, with enterprises generally reporting sluggish external demand in November. Additionally, sharp fluctuations in aluminum prices led to more cautious downstream procurement—aluminum prices surged rapidly to 22,000 yuan/mt in early November before pulling back significantly, suppressing some order releases. As prices stabilized toward month-end, market transactions saw a slight recovery. Entering December, the rapid price surge again caused temporary disruptions to downstream cargo pick-up pace, but the fundamental demand-side trend remained stable. Coupled with stockpiling demand from year-end performance pushes in end-use sectors, orders for secondary aluminum enterprises continued to receive support.

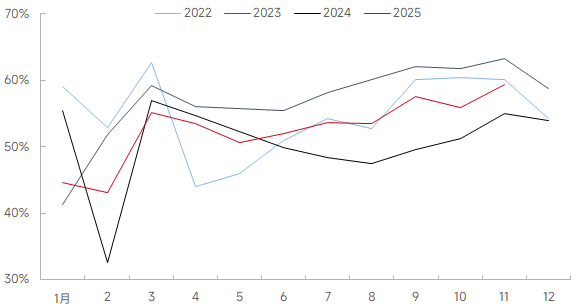

Supply side, the operating rate for the secondary aluminum alloy industry in November rose 3.57 percentage points MoM to 59.41%, up 2.01 percentage points YoY. The increase was mainly driven by two factors: first, production quickly returned to normal after the holiday period; second, end-use market demand recovered, especially among top-tier enterprises with automotive-focused orders accelerating capacity release, effectively boosting the industry's overall operating level. However, constrained by raw material prices fluctuating at highs and persistent tight supply of aluminum scrap, the growth in the industry's operating rate fell short of expectations, and capacity release still faced bottlenecks. Additionally, detailed implementation rules for fiscal subsidy policies for the secondary aluminum industry in provinces such as Jiangxi and Henan have yet to be clarified, creating uncertainty and leading some local secondary aluminum enterprises to maintain cautious operations, including production halts or cuts. Looking ahead to December, while stable demand is expected to support maintaining a relatively high operating rate, factors such as raw material supply deficits, potential losses from production costs, anticipated regional seasonal environmental protection-driven production restrictions, and tax policy uncertainties will continue to constrain capacity release. The industry's operating rate in December is projected to show a slight pullback from highs.

Entering December, secondary aluminum alloy prices are expected to continue fluctuating at highs. Although aluminum scrap traders have shown an increased willingness to sell recently, improving market liquidity, overall supply remains relatively tight, providing support on the cost side. Demand side presents a mixed picture: on one hand, year-end rush to deliver orders from end-users will lend resilience to the market; on the other hand, high prices' dampening effect on downstream procurement, coupled with seasonally weaker demand, may limit consumption. Supply side, constrained by raw materials, is unlikely to see significant increases, while low industry inventory provides a floor for prices. Overall, ADC12 prices have limited downside room, but a breakthrough to the upside would depend on further cost-driven increases or stronger-than-expected demand release. Prices are anticipated to trade in a narrow range at high levels in December, with key focus on the progress of aluminum scrap supply improvements, actual policy implementation, and changes in downstream enterprises' procurement pace.