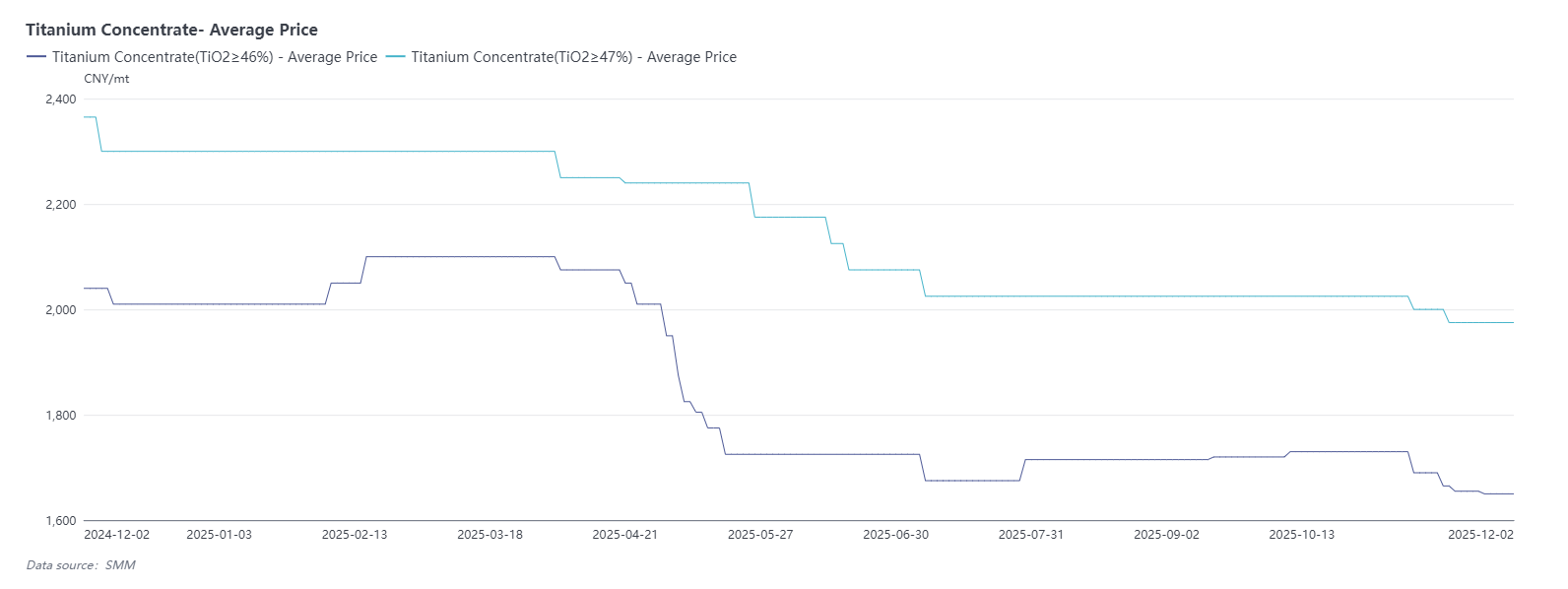

Titanium Concentrate: Prices Continue Downward Trend, Weakening Downstream Demand Intensifies Pressure

As of November 28, the quoted price range for domestic titanium concentrate (TiO₂ ≥46%) is 1620-1680 yuan/ton, with an average price of 1650 yuan/ton, down 80 yuan compared to the previous month. The quoted price range for TiO₂ ≥47% is 1900-2050 yuan/ton, with an average price of 1975 yuan/ton, down 50 yuan compared to the previous month.

In November, titanium concentrate prices continued their downward trend, with market demand showing clear signs of weakness. The main reasons are the continuous decline in prices of its primary downstream product, titanium dioxide, and the industry-wide predicament of cost-price inversion. Weak demand and cost pressures are gradually being transmitted upstream, leading to reduced enthusiasm for titanium concentrate procurement. Simultaneously, downstream sectors have shown stronger intentions to push down raw material prices, jointly driving the decrease in titanium concentrate prices.

Titanium Dioxide: Weak Supply-Demand Dynamics and Cost-Price Inversion Coexist, Year-End Price Support by Enterprises Faces Test

As of November 28, anatase titanium dioxide is quoted at 11,800-12,200 yuan/ton, averaging 12,000 yuan/ton. Rutile titanium dioxide is quoted at 12,300-13,700 yuan/ton, averaging 13,000 yuan/ton, with an FOB average price of $1890/ton. Chloride-process titanium dioxide domestic quotes are 14,000-16,000 yuan/ton, averaging 15,000 yuan/ton, with an FOB average price of $2080/ton.

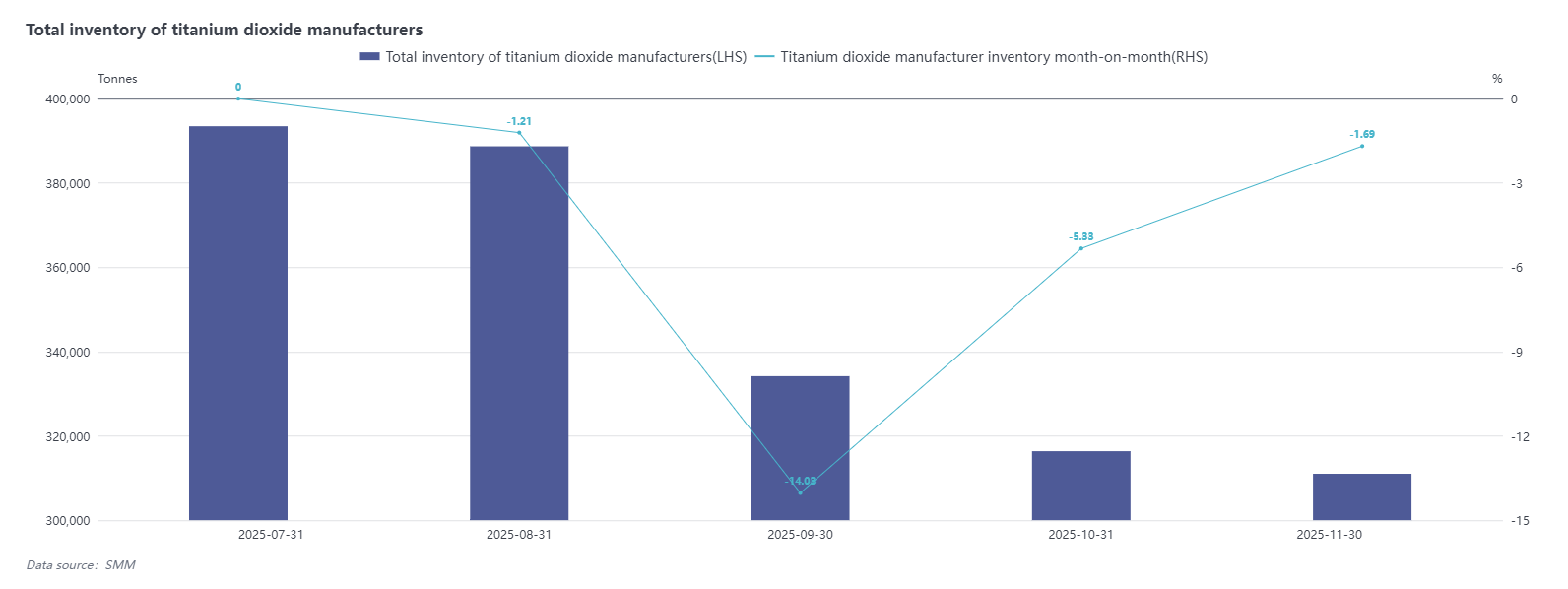

According to SMM survey data, China's titanium dioxide production in November 2025 remained generally stable overall, with some enterprises operating at full capacity. Monthly output increased by 4.33% month-on-month, and producer inventory decreased by 1.69% month-on-month. From the perspective of the supply-demand structure, since the industry gradually resumed production in September, the expansion trend in titanium dioxide capacity has been evident. However, downstream demand has remained consistently weak overall. Currently, enterprise shipments mainly involve fulfilling previous orders, promoting a gradual reduction in inventory. Nevertheless, the number of new orders is limited, and market acceptance of high-priced resources is generally low.

In early November, titanium dioxide market prices showed a covert downward trend, primarily due to overall weak order performance in October and persistently sluggish domestic demand. The attempted second round of price hikes earlier did not achieve the expected effect, leading to a gradual price correction across brands again. In the international market, affected by anti-dumping policies, Chinese titanium dioxide faces significant sales resistance in key markets such as Europe, Brazil, and India. Consequently, enterprises are also in a state of oversupply and fierce competition in overseas markets.

Specifically, the sulfuric acid process titanium dioxide market is characterized by an overall oversupply and prominent product homogeneity, with enterprises facing intense competition in both domestic and export markets. Regarding chloride-process titanium dioxide, Chinese products are primarily positioned in the mid-to-low-end segments in the international market. Therefore, since October, chloride-process prices have also fallen sharply and have gradually approached the price levels of sulfuric acid process products.

In mid-to-late November, sulfuric acid costs experienced a significant increase, with the latest delivered price exceeding 1000 yuan/ton. It is understood that the rise in sulfuric acid prices is mainly driven by stronger sulfur prices: firstly, significant incremental demand for sulfuric acid/sulfur from Indonesia's nickel industry; secondly, increased demand due to domestic winter fertilizer preparation; and thirdly, reduced supply of by-product sulfur due to operational reductions at Russian refineries.

As costs continue to rise while product prices remain depressed and market demand weak, titanium dioxide enterprises are generally caught in a dilemma of cost-price inversion. In response, multiple enterprises successively issued price adjustment notices in late November, raising both domestic and foreign trade quotations simultaneously, aiming to curb the downward trend in market prices. The effectiveness of these price adjustments still awaits further market feedback. In the short term, with output likely remaining stable, titanium dioxide inventories may accumulate again. Sulfuric acid process enterprises might opt for production reduction or even shutdown due to cost pressures. SMM will continue to monitor price and production adjustments by other titanium dioxide enterprises and the implementation status following the announced price increases.

Sponge Titanium: Weak Domestic and External Demand Constrains Prices, Market Continues Weak but Stabilizing

As of November 28, the mainstream price for Grade 0 sponge titanium is 46,000-47,000 yuan/ton, FOB $6650/ton; Grade 1 sponge titanium is quoted at 45,000-46,000 yuan/ton; Grade 2 sponge titanium is quoted at 44,000-45,000 yuan/ton.

According to SMM survey data, China's sponge titanium production in November 2025 was approximately 24,000 tons, a month-on-month increase of 3.42%, with overall production operating smoothly.

Since the second half of the year, the sponge titanium market has generally shown a weak and sluggish trend, with persistently insufficient demand follow-through. Although some enterprises issued price adjustment notices in mid-November to stabilize prices, overall market confidence remains weak currently. Downstream acceptance of the price adjustments is limited, with most orders still executed at original prices. The market overall shows signs of stabilizing after the decline.

In the domestic market, demand gradually weakened after the traditional peak season of "Golden September and Silver October," lacking sustained upward momentum. The foreign trade market has remained sluggish since the second half of the year, with order volumes shrinking, resulting in a supply-exceeds-demand pattern and gradually accumulating inventory pressure. Against this backdrop, sponge titanium production in December is expected to see a certain degree of reduction to support price stabilization.