The 2025 Asia Copper Week has concluded, yet the benchmark for 2026 copper concentrate long-term contracts remains unresolved. Market concerns persist over the current landscape of negative TCs. On the cathode side, long-term contract offers for 2026 have shocked the market, with the significant gap between expectations and reality making negotiations extremely challenging. Below is SMM’s consolidated analysis of long-term contract information gathered during CESCO.

A fundamental shift has taken place in the pricing logic for 2026 registered copper long-term contracts, compared with 2025. Nearly all COMEX-registered brands have incorporated the LME–COMEX arbitrage spread into their quotations.

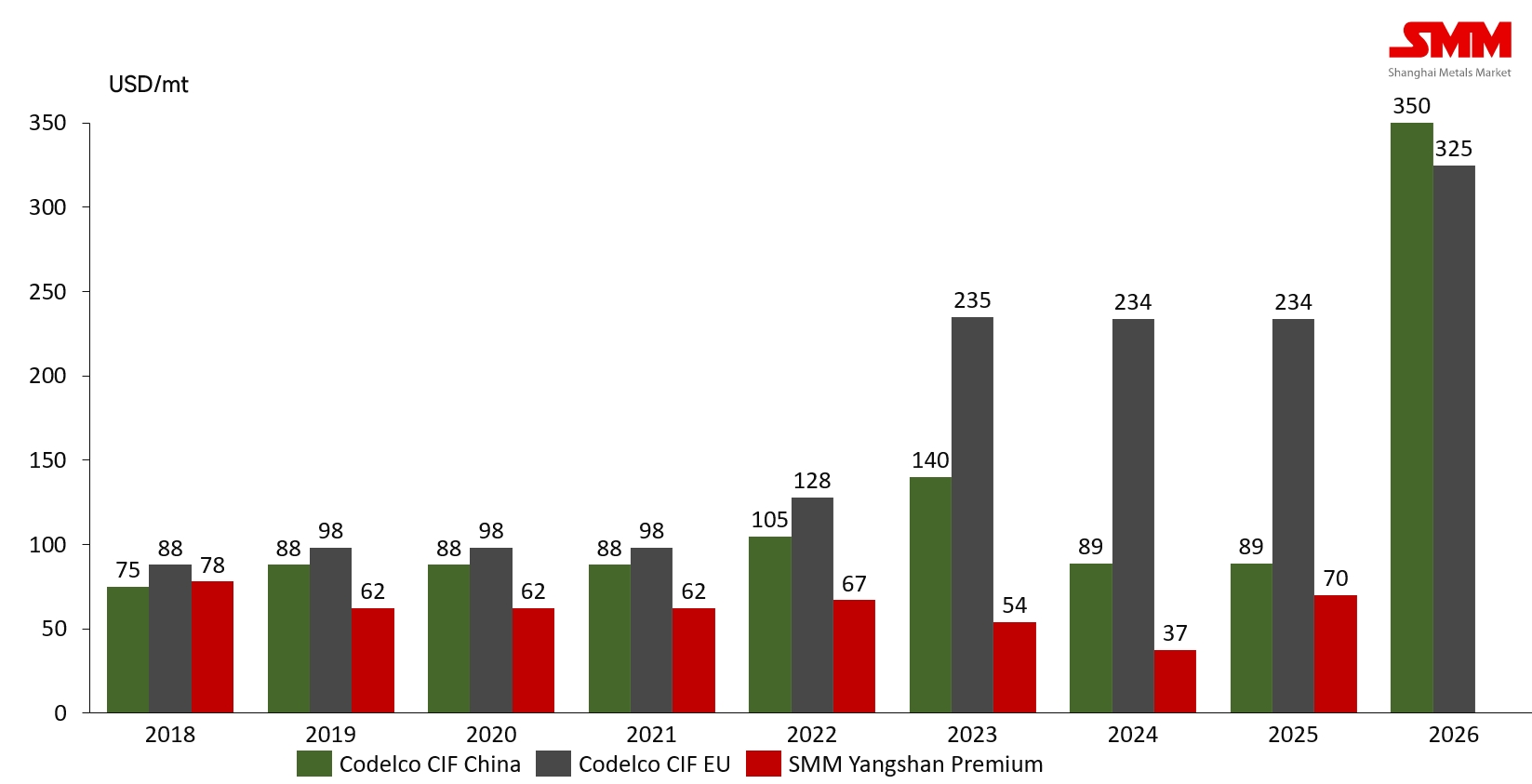

According to SMM, Codelco has offered:

-

USD 330/mt CIF Korea & Taiwan for 2026, up USD 245/mt from USD 85/mt in 2025;

-

USD 325/mt CIF Europe, up USD 91/mt from USD 234/mt in 2025;

-

USD 350/mt CIF China, up USD 261/mt from USD 89/mt in 2025.

FOB Chile premiums are reportedly above USD 500/mt.

With Poland, South Korea, Australia and other origins becoming eligible COMEX brands in 2025, the sharp increase in related long-term contract premiums has become increasingly evident.

Against this backdrop of overseas registered copper premiums “soaring rocket” Asian traders and downstream buyers have naturally shifted their attention toward EQ cathode sources—which represent a larger share of imports—as well as long-term export contracts from Chinese smelters.

From January to October 2026, African copper cathodes are estimated to account for approximately 1.47 million tonnes, nearly half of China’s total cathode imports, and the share is expected to rise further. As a result, negotiations for 2026 EQ long-term contracts have intensified. According to SMM, 2026 CIF Shanghai EQ long-term contracts are currently offered in small volumes at USD 80–110/mt, mostly quoted on QP=arriving month M+1, representing an increase of roughly USD 80/mt from 2025 levels.

Meanwhile, DRC-based smelters have also begun preliminary discussions, with highly fragmented offers:

-

In the Kolwezi region, large-scale mining groups have not yet issued formal LT offers; smaller producers are quoting FCA –USD 400 to –USD 380/mt, with QP = loading month M+2.

-

In the Likasi region, some medium-sized smelters are quoting FCA –USD 370 to –USD 360/mt, with QP =loading month M+2 to M+1.

During the CESCO week, certain long-term offers rose to above –USD 300/mt, with freight indexed to 2025 Q4 levels.Depending on the prepayment and other side contract, the DRC FCA premium is more diversified. SMM will continue to track further developments.

Overall, overseas smelter quotations for 2026 long-term contracts have increased sharply compared with 2025, intensifying negotiation pressures for traders. In the current distorted environment—where 2026 import parity is expected to be weak while import availability remains tight—downstream consumers have expressed difficulty accepting such elevated premiums in the short term.

No floating-price long-term contract offers have been reported so far, and discussions between buyers and sellers remain ongoing. SMM will continue to monitor the progress of 2026 USD-denominated copper long-term contract negotiations.

![The Price Spread Between High-Quality Copper and Standard-Quality Copper Continued to Narrow, While SHFE Copper Spot Discounts Gradually Stabilized [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/YIaMU20251217171711.jpg)

![Inventory Continued to Decline, Suppliers Held Prices Firm Accordingly, and Spot Trades Were Better Than Yesterday [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/KtfdC20251217171713.jpeg)