- SMM Cold Rolling Production Schedule: Cold Rolling Production at Steel Mills Edged Down in November

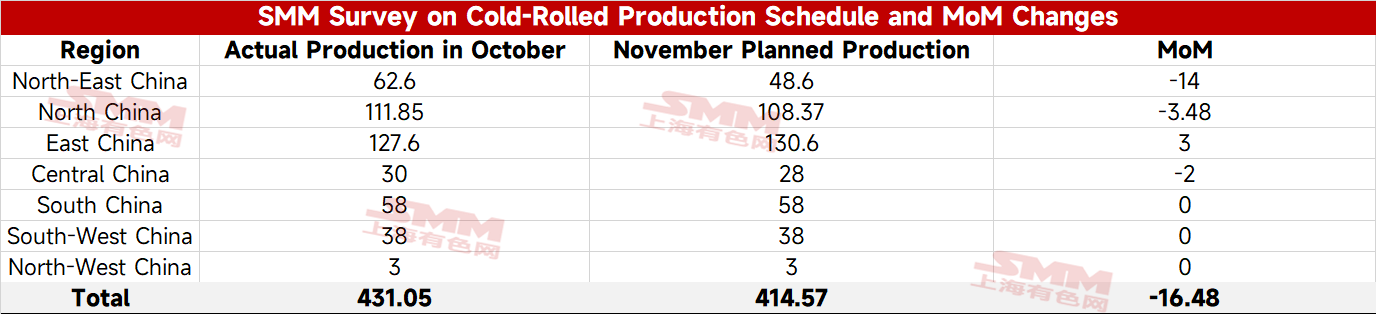

According to the latest SMM tracking, the planned production volume of cold-rolled commercial material from 31 mainstream steel mills totaled 4.1457 million mt in November, down 164,800 mt MoM from the actual production in October, a decrease of 3.8%.

On a daily average basis, November has one fewer day than October. The daily average production schedule of cold-rolled commercial material in November was 138,200 mt, down 0.6% MoM from the daily average actual production in October.

- SMM HRC Production Schedule: November HRC Production Down 2.2% MoM, Daily Average Up 1.0% MoM

According to the latest SMM tracking, the total planned volume of HRC commercial material from 39 mainstream steel mills in November is 14.0503 million mt, a decrease of 321,500 mt MoM compared to the actual HRC commercial material production in October, down 2.2%.

On a daily average basis, with November having one fewer day than October, the daily average HRC commercial material production schedule for this month is 468,300 mt, up 1.0% MoM compared to the daily average actual production in October.

Summary: In November, the production schedule for hot-rolled commercial steel from steel mills decreased by 2.2% MoM. Since November has fewer days than October, the daily average production schedule for hot-rolled products this month actually increased slightly by 1.0% MoM compared to the actual production of the previous month. Hot-rolled coil production continued to fluctuate at high levels in November. Demand side, entering November, construction activity in the real estate and infrastructure sectors is expected to gradually weaken, while performance in the manufacturing sector is diverging. For the home appliance sector, according to the latest production schedule report for the three major white goods released by ChinaIOL, the total scheduled production for air conditioners, refrigerators, and washing machines in November 2025 reached 28.47 million units, down 17.7% YoY compared to the actual production in the same period last year. For the automotive sector, the phase-out of the purchase tax policy is expected to boost market performance in Q4, and demand in the automotive industry still has strong expectations towards the year-end. In November, hot-rolled coil is expected to maintain high supply, with demand showing moderate resilience but lacking strong momentum. The inventory drawdown rate may be slower than the same period in previous years.

In other aspects, the impact from a macro perspective weakened in November. Cost side, hot metal production in November is expected to decline MoM. Overall, the fundamentals for hot-rolled coil in November still show contradictions, making it difficult to form strong upward momentum for prices. Hot-rolled coil prices may continue to move sideways, with attention on the deviation in expectations for hot metal production cuts and the impact of domestic and international news.

![[SMM Steel] SMS Group wins SAIL Durgapur billet caster modernization project](https://imgqn.smm.cn/usercenter/JSngP20251217171719.jpg)

![[SMM Steel] US drawn wire exports rise 12.5% MoM in January 2026](https://imgqn.smm.cn/usercenter/VgxkU20251217171719.jpg)

![[SMM Steel] Eurofer urges EU to act fast as global steel overcapacity hits record 2.4 billion mt](https://imgqn.smm.cn/usercenter/exdqc20251217171717.jpg)