SMM November 19 News:

Highlights: Phosphate ore maintained a tight supply-demand balance with firm prices. Sulfur raw material prices surged 46% due to tight global supply, pushing up the costs of sulfuric acid and downstream products. Coupled with robust demand from the new energy sector for phosphoric acid and industrial-grade MAP, prices of phosphorus chemical products rose across the board, resulting in a stronger-than-usual off-season market.

In Q4 2025, the phosphorus chemical market experienced a strong rally. Upstream phosphate ore maintained a tight balance supported by winter fertilizer stocking and new energy demand; midstream sulfur raw material prices soared due to international supply shortages, significantly raising production costs of core product sulfuric acid. At the same time, robust demand from the LFP industry strongly boosted phosphoric acid and industrial-grade MAP. Driven by both cost and demand factors, prices across the phosphorus chemical industry chain rose comprehensively.

I. Phosphate Ore: Firm Prices and Tight Supply-Demand Balance

Phosphate ore prices remained firm, influenced by winter fertilizer stocking and strong new energy demand.

Supply side, periodic mining suspensions in some regions affected supply, while newly commissioned mines ramping up capacity helped alleviate tightness. Due to high cross-regional sales costs, supply-demand imbalances persisted in various regions. Demand side, robust demand from the new energy sector increased demand for iron phosphate, LFP, and LiPF6, driving up phosphate resource consumption.

II. Phosphorus Chemical Products: Rising Sulfur Raw Material Prices and Strong Downstream Demand Drive Broad-Based Price Increases

In Q4 2025, the phosphorus chemical market saw some changes in winter fertilizer stocking due to the later timing of the Chinese New Year holiday; on the new energy side, strong demand from the LFP industry for phosphoric acid and industrial-grade MAP led to a stronger-than-usual off-season for phosphorus chemical products. Simultaneously, rising production costs of sulfuric acid driven by sulfur price increases contributed to a wave of price hikes across phosphorus chemical products.

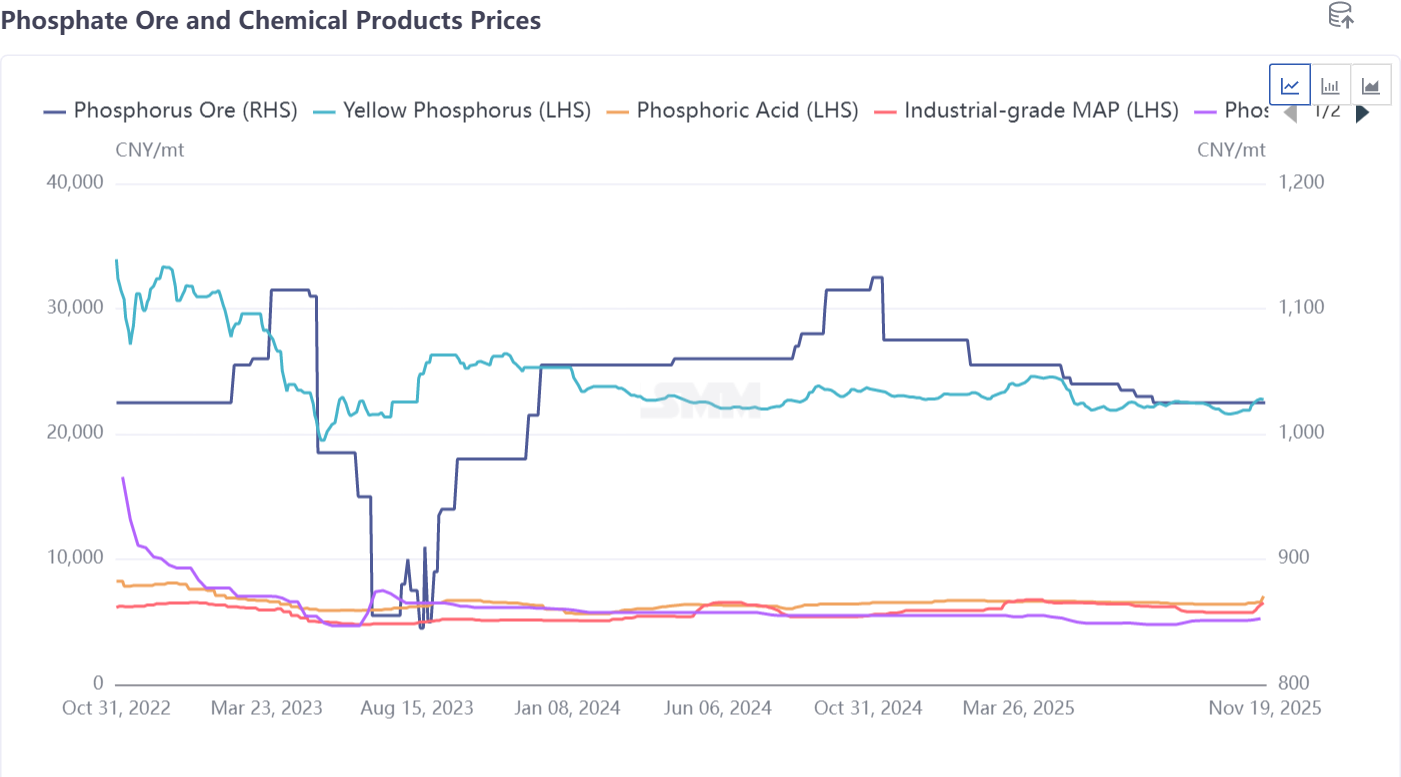

Sulfur prices surged 46%, rising from 2,600 yuan/mt in October to 3,800 yuan/mt currently, transforming sulfur from a mild performer into a sharp riser.

The continuous climb in sulfur prices increased sulfuric acid prices, with 1 mt of sulfur producing 3 mt of 98% sulfuric acid. For every 100 yuan/mt increase in sulfur, the per-ton cost of sulfuric acid rose by 33 yuan; from October to present, sulfuric acid costs increased by 400 yuan/mt.

Sulfur supply: Supply tightened due to production cuts at Russian refineries, reducing sulfur availability as a by-product. In other regions, slight production decreases at Canadian sulfur mines and in the Middle East affected global sulfur market demand. Sulfur's main downstream use is in producing sulfuric acid via the thermal process; sulfuric acid is a fundamental chemical raw material with high demand and broad applications.

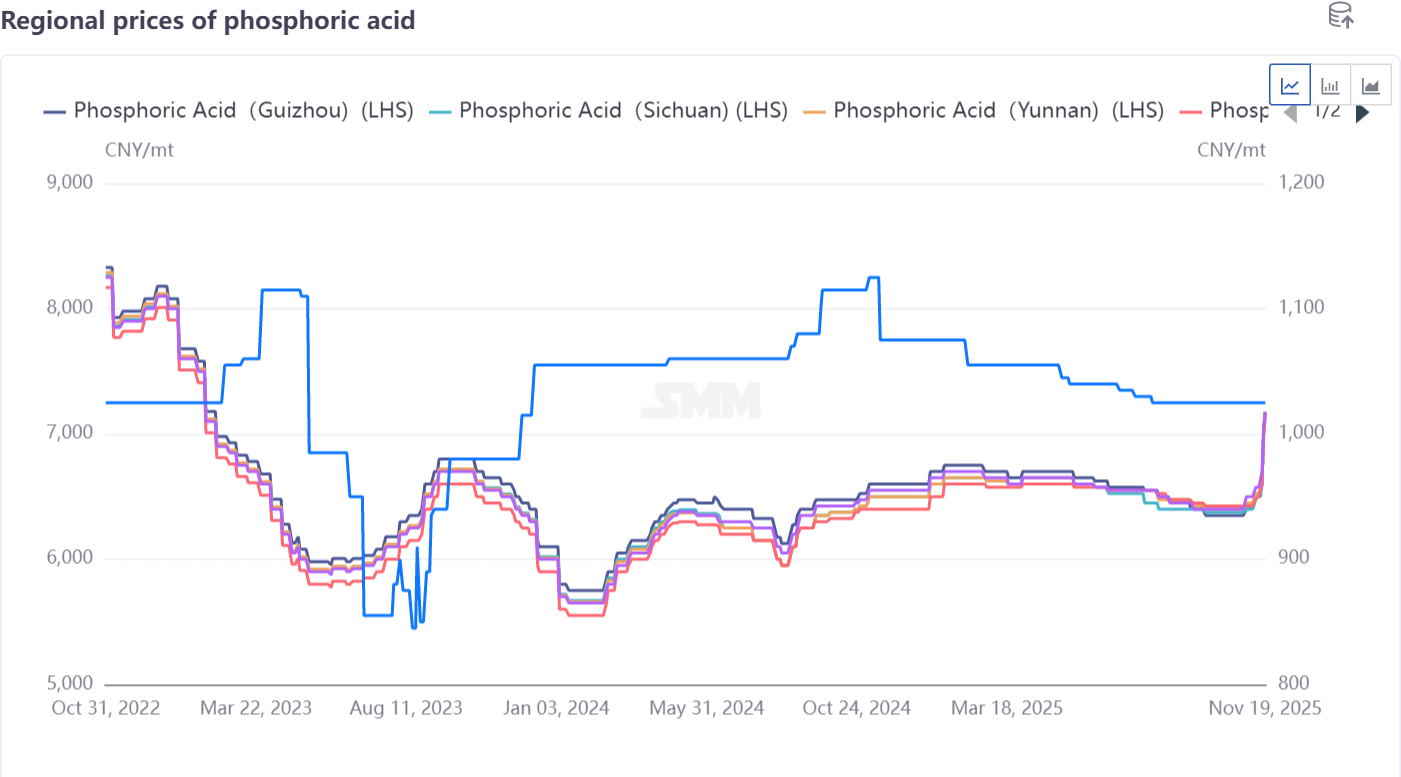

Due to rising costs and strong new energy demand, the price of 85% phosphoric acid increased from 6,400 yuan/mt in October to 7,000 yuan/mt in November.

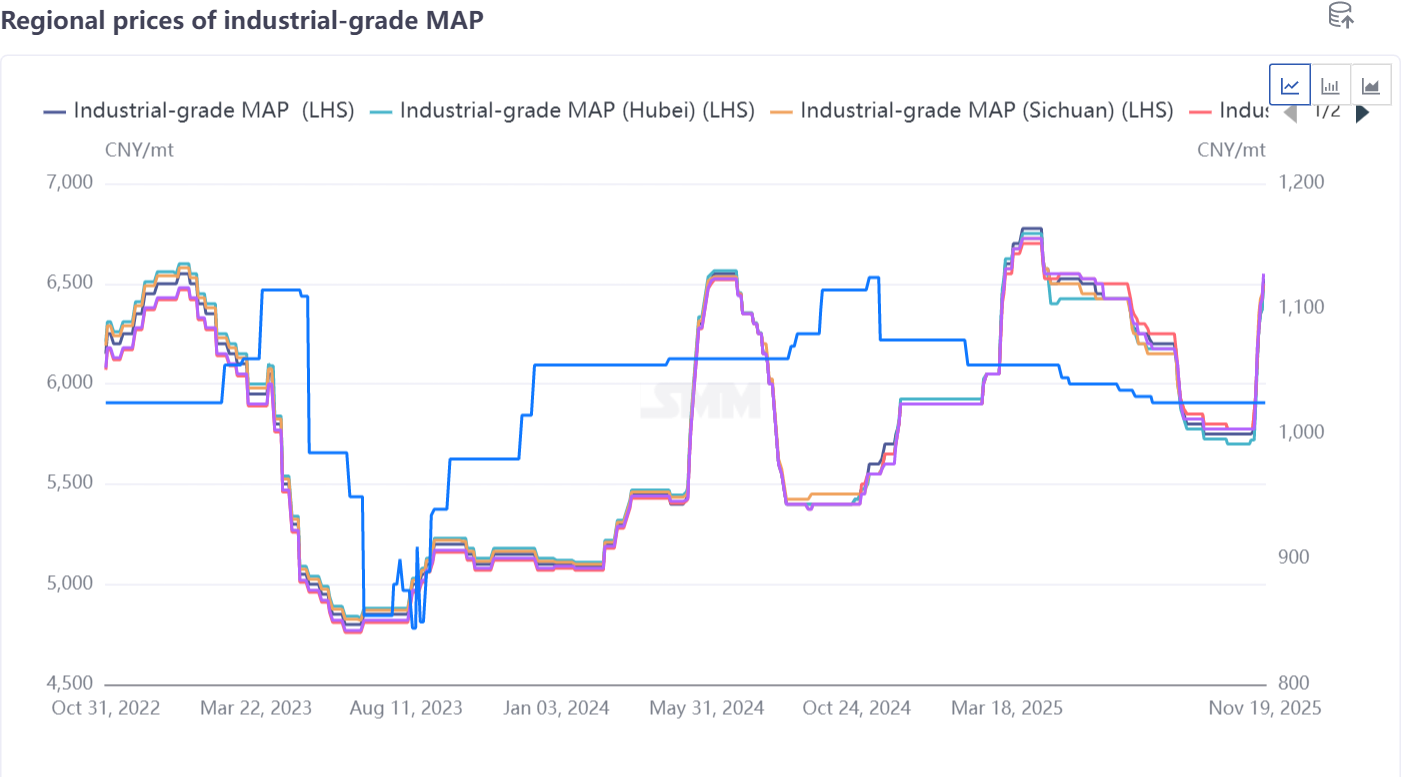

The price of industrial-grade MAP rose from 5,700 yuan/mt in October to 6,300 yuan/mt in November.