- Policy and Demand Drive Dual Improvements in Steel Mills' Production Structure

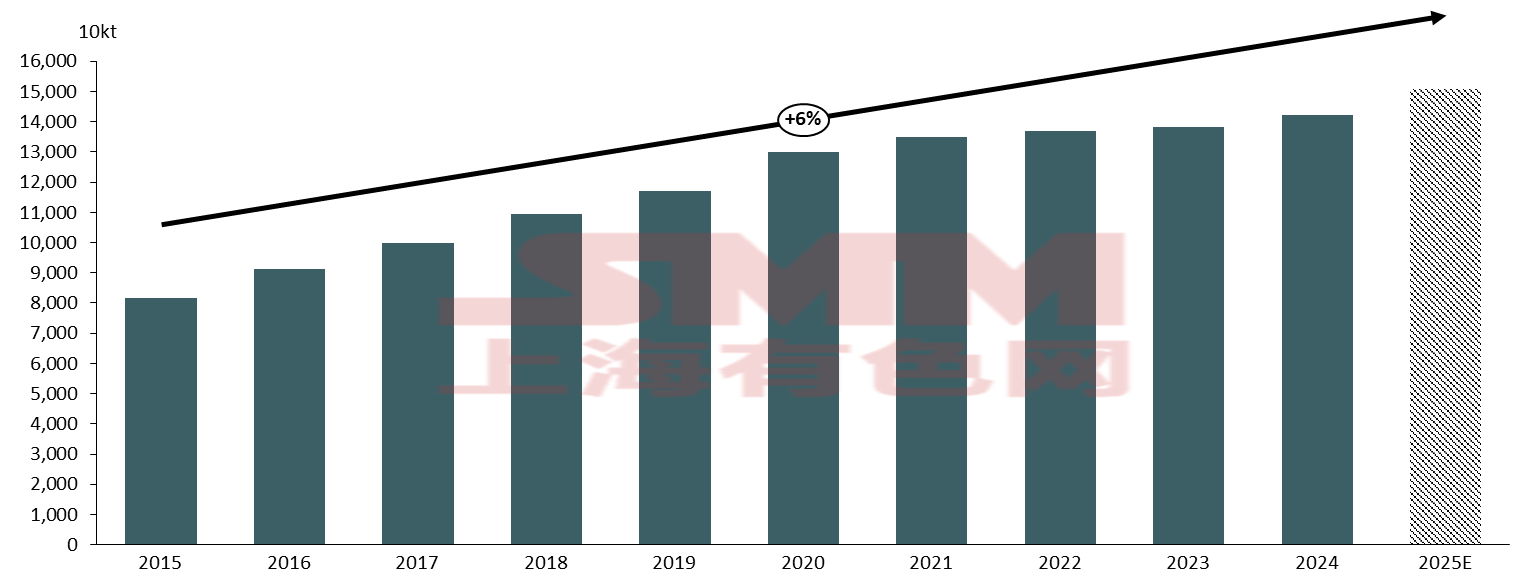

Cold rolling capacity increased by 60% over the past decade. From 2015 to 2020, cold rolling capacity grew steadily and rapidly, with an average annual growth rate of 9.7%, peaking at around 11% in 2020. Starting in 2021, the Implementation Measures for Capacity Replacement in the Steel Industry promoted an increase in the cold rolling capacity utilization rate, leading to a significant rise in cold rolling production, while the growth rate of cold rolling capacity slowed down, with the average annual growth rate from 2021 to 2024 slowing to 2.9%. This shift reflects the industry's transition from capacity expansion to competition for market share, while also driving steel mills to produce higher-end products to capture market share. Subsequently, starting in 2022, MIIT's "Advanced Steel Materials" initiative provided subsidies for ultra-high-strength automotive steel; in 2023, the Ministry of Commerce included cold-rolled silicon steel and high-strength automotive sheets in the "High Value-Added Steel Products" white list; and rapid development in downstream sectors, especially NEVs, significantly boosted demand for high-end cold-rolled automotive steel. Stimulated by both policy and demand, steel mills improved their production structure. According to an SMM survey, profits from specialty steel are higher than those from general cold-rolled products, and order intake for specialty steel is stronger. As a result, steel mills prioritize specialty steel in their production schedules and reduce general cold-rolled production when appropriate.

China's Cold Rolling Capacity, 2015-2025E

Source: SMM

- Long-Term Planning Required to Address "Eastern Materials Transported West"

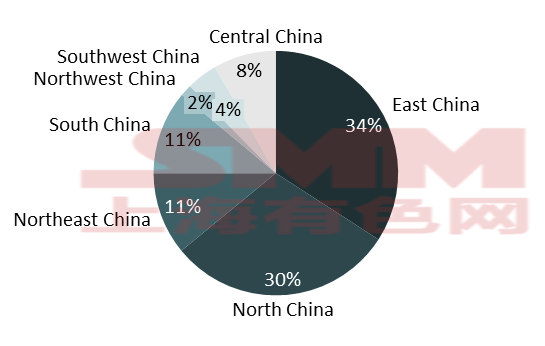

In terms of cold rolling capacity distribution, east China and north China account for over 60% of total capacity, making them the two major cold rolling hubs that firmly control supply dominance. South China and northeast China follow in scale, but their capacity is only one-third that of east and north China. Central, southwest, and northwest China together account for less than 15%, with low capacity density but significant manufacturing demand, making them clear net importers of cold rolling resources. Overall, cold rolling capacity is concentrated in the Yangtze River and coastal regions, while western China is severely marginalized.

Looking ahead, with the agglomeration and development of the automotive and home appliance industries in the western region, demand is driving a westward shift in cold rolled coil (CRC) capacity. Moreover, the "Western Region Encouraged Industry Catalog (2025 Edition)" supports electric furnace production, while blast furnaces still need to comply with capacity replacement requirements. Changing the pattern of "eastern materials transported west" still requires long-term planning.

Distribution of China's CRC Capacity in 2025

Source: SMM

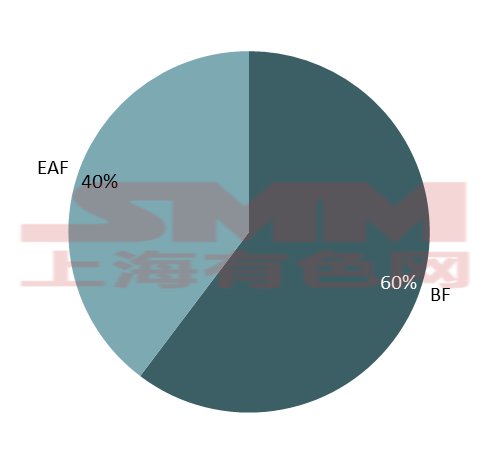

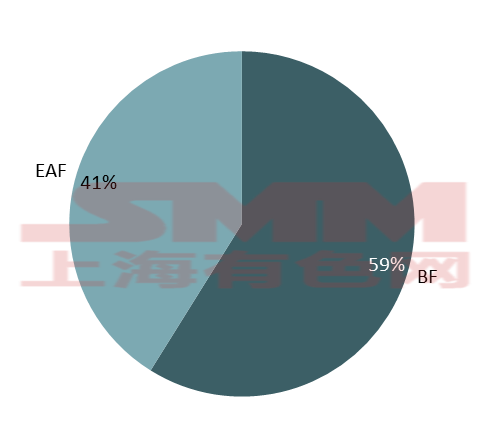

- The "BF Six, EAF Four" Pattern Appears Unchanged, but Holds Hidden Complexities

Examining the changes in the share of BF and EAF CRC capacity from 2020 to 2025, the "BF six, EAF four" pattern remained unchanged for six years, confirming our earlier point that the 2021 CRC capacity replacements shifted CRC steel mills from capacity expansion to competing for existing market share. Consequently, while the overall CRC capacity showed little apparent fluctuation from 2020 to 2025, significant internal changes have already occurred within the CRC capacity landscape.

Comparison of BF and EAF Steel Mill CRC Capacity: 2020 vs. 2025

Source: SMM

Over the six years, although the EAF share increased by only 1%, notable internal shifts occurred. EAF steel mills phased out low-annual-production lines, replacing them with higher-annual-output, more efficient lines, thereby reducing energy consumption per metric ton of steel and boosting profits. Simultaneously, BF steel mills further optimized their internal production systems, extended production line lengths, and gradually formed an internal closed loop from molten iron to HRC to CRC, securing profits from base materials internally.

- When Carbon Costs Meet Green Electricity Premiums: Where is the Steel Industry Headed?

Furthermore, green development is currently a key focus for the steel industry. BFs have high coal consumption and low electricity consumption, whereas EAFs primarily consume electricity. However, against the backdrop of the "dual carbon" goals, deep decarbonization of the steel industry inevitably requires a decrease in the BF share and an increase in the EAF share. According to SMM, many BF steel mills are already advancing green electricity production models. For example, since the start of the "14th Five-Year Plan" period, JISCO launched a 2,400 megawatt (MW) smart grid and a new energy local consumption demonstration project, achieving a green electricity share of 31.2% and an annual reduction of 2.1 million metric tons of standard coal. Baosteel Zhanjiang is expected to complete China's first near-zero carbon production line for high-grade thin steel sheets using a "hydrogen-based shaft furnace + electric furnace" short process by the end of 2025, with an estimated annual production of approximately 1.8 million metric tons of zero-carbon sheets & plates and an annual carbon emission reduction exceeding 3.14 million metric tons. Baosteel initiated green electricity trading in 2018 and can now achieve prices for some externally purchased green electricity that are lower than thermal power prices, among other initiatives.

From the perspective of carbon costs, according to the national carbon emissions trading information released by the Shanghai Environment and Energy Exchange, the comprehensive price closing price of the national carbon market in 2024 fluctuated between 69 yuan/mt and 106 yuan/mt, stabilizing at 97.49 yuan/mt by the end of 2024. Based on calculations by the China Iron and Steel Association (CISA) and further computations by SMM, the carbon emissions per metric ton of cold-rolled steel produced by blast furnace steel mills are approximately 2.2 metric tons of CO2, while for EAF steelmaking, the figure is about 0.7 metric tons of CO2, resulting in a difference of 1.5 metric tons of CO2 per metric ton. Combining this with the comprehensive closing price of the carbon market at the end of 2024, the EAF process incurs approximately 146 yuan/mt less in carbon costs compared to the blast furnace process. Regarding the green electricity premium, producing one metric ton of cold-rolled steel using green electricity via the EAF process is influenced by the energy consumption of the steel mill's EAF cold-rolling process and green electricity prices, and varies depending on the mill's technology and regional policies. The market price of cold-rolled steel produced with green electricity is also higher than that of ordinary cold-rolled steel, exhibiting a significant percentage range premium.

Considering both carbon costs and the green electricity premium, with the continued implementation of the "dual carbon" policy, the cost of green electricity production is expected to gradually decrease, while carbon costs are expected to rise. The production curves for BF and EAF processes will gradually shift, and the share of EAF capacity is projected to further increase in the future.

In summary, over the past decade, the development focus of China's cold-rolled industry has clearly shifted from "quantitative expansion" to "quality improvement." The slowdown in capacity growth coupled with rising utilization rates signals that industry competition has formally entered a stage centered on technology, structure, and efficiency. Driven by precise policy guidance and downstream high-end demand, capacity replacement has promoted internal structural optimization and upgrading, and the trend towards product premiumization is irreversible. Meanwhile, the "dual carbon" goals are reshaping the industry's production logic and cost curves, opening up broad development space for the EAF process and green smelting technologies. Looking ahead, key challenges for the industry will be resolving the "eastern materials transported west" dilemma caused by imbalanced regional capacity distribution, and balancing the costs and benefits of the green transition.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)