SMM Report, October 31

The domestic molybdenum market in China saw a trend of first rising and then falling in October. Supported by the limited output release from mines, the price of molybdenum concentrate dropped only slightly. However, the ferromolybdenum market witnessed a sharp price decline due to the negative factors of weak downstream demand and loosened cost support, leading to significant industry losses. The operating rate in October fell to around 48%, a new low for the year, and once again diverged from the operating trend of molybdenum concentrate mines, resulting in intense market games.

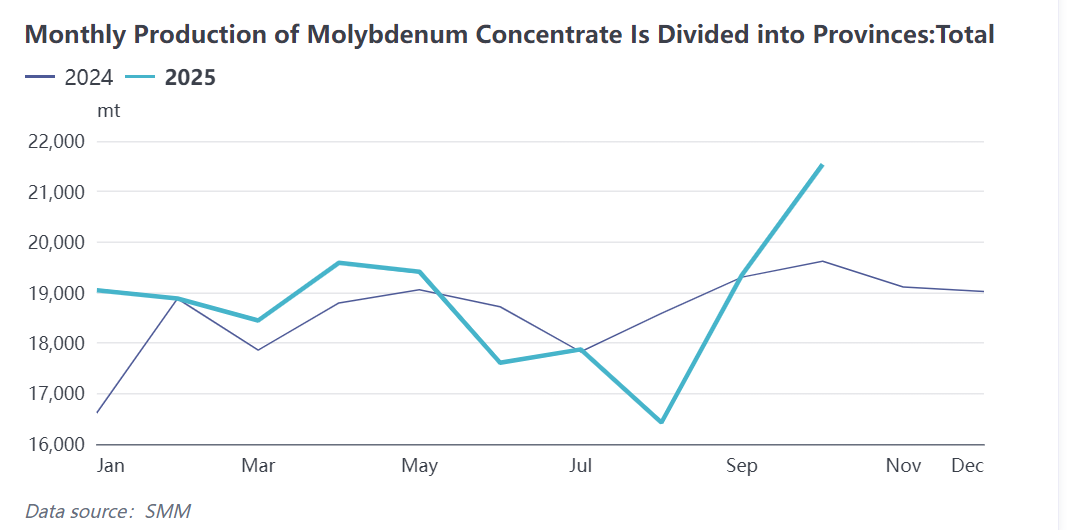

According to SMM data, the domestic output of molybdenum concentrate in China maintained a growth momentum in October 2025, with a month-on-month increase of 11.3% and a year-on-year increase of 13.9%. From January to October 2025, the total output of molybdenum concentrate rose by 3.6% year-on-year.

In October, most domestic molybdenum mines maintained stable production. Only some small mines in regions such as Shaanxi conducted maintenance and reduced production during the month, which had a minimal impact on the overall output. By province, the output of molybdenum concentrate in Henan, Inner Mongolia, and Heilongjiang increased slightly in the month. This was mainly due to the expansion and resumption of production by some mines in the early stage, which pushed the output higher than that in September. The price of molybdenum concentrate first rose and then fell in October. Major mines concentrated on selling goods in the first ten days of October; later, driven by weak demand, the market price declined, the willingness of mines to sell decreased, and the implicit inventory in the industry increased.

In October, most domestic molybdenum mines maintained stable production. Only some small mines in regions such as Shaanxi conducted maintenance and reduced production during the month, which had a minimal impact on the overall output. By province, the output of molybdenum concentrate in Henan, Inner Mongolia, and Heilongjiang increased slightly in the month. This was mainly due to the expansion and resumption of production by some mines in the early stage, which pushed the output higher than that in September. The price of molybdenum concentrate first rose and then fell in October. Major mines concentrated on selling goods in the first ten days of October; later, driven by weak demand, the market price declined, the willingness of mines to sell decreased, and the implicit inventory in the industry increased.

Looking at the ferromolybdenum market, SMM data shows that China's domestic ferromolybdenum output in October 2025 decreased by 11.2% month-on-month and 14.2% year-on-year. From January to October 2025, the total output of ferromolybdenum increased by 6% year-on-year.

Looking at the ferromolybdenum market, SMM data shows that China's domestic ferromolybdenum output in October 2025 decreased by 11.2% month-on-month and 14.2% year-on-year. From January to October 2025, the total output of ferromolybdenum increased by 6% year-on-year.

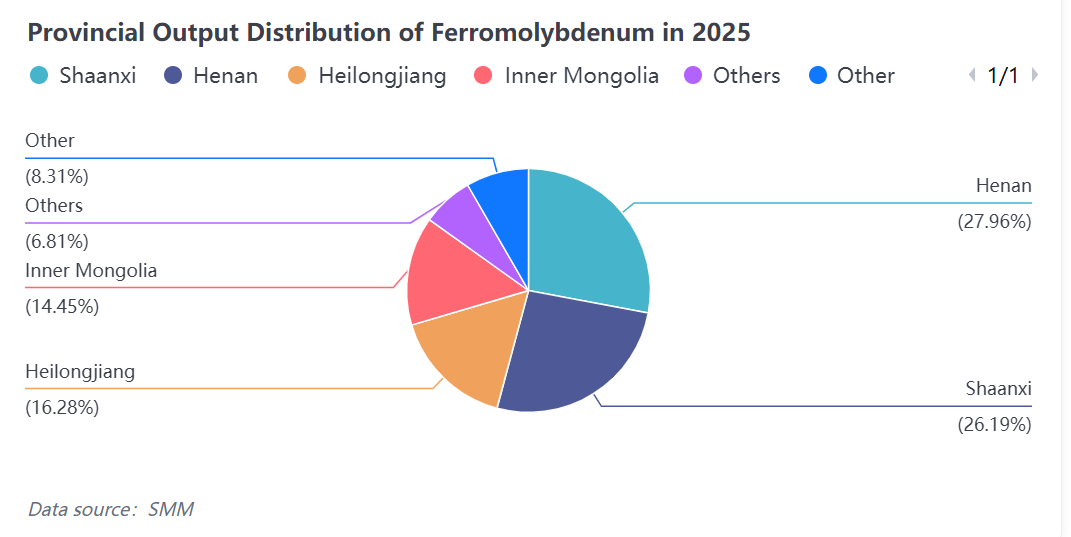

In October, the domestic ferromolybdenum industry suffered obvious losses, and coupled with weak demand from downstream steel mills, the operating rate of domestic ferromolybdenum enterprises generally declined. Most enterprises arranged production and delivery based on early orders, showing low willingness to accept new orders, and production scheduling mainly decreased. By province, the operating rate of ferromolybdenum in Liaoning, a major production area, dropped significantly in October. The operating rate of ferromolybdenum in Liaoning Province in October was about 44%, a month-on-month decrease of 4 percentage points, leading the decline. In contrast, major ferromolybdenum plants in Henan and Shaanxi have their own molybdenum ore resources, so their operation was relatively stable, and the overall operating rate in the provinces fluctuated slightly. SMM data shows that the operating rate of the domestic ferromolybdenum industry in October was about 49%, a month-on-month decrease of 6 percentage points, marking the lowest operating rate of the year. In terms of cost, domestic ferromolybdenum plants generally suffered losses in October. According to SMM data, the monthly average price of 45% molybdenum concentrate in China in October was about 4,379.7 yuan per ton-degree, and the average cost of 60% ferromolybdenum was about 282,000 yuan per ton. However, the average price of the ferromolybdenum industry in October was about 276,700 yuan per ton, with an average monthly loss of 5,100 yuan per ton in the industry.

In October, the domestic ferromolybdenum industry suffered obvious losses, and coupled with weak demand from downstream steel mills, the operating rate of domestic ferromolybdenum enterprises generally declined. Most enterprises arranged production and delivery based on early orders, showing low willingness to accept new orders, and production scheduling mainly decreased. By province, the operating rate of ferromolybdenum in Liaoning, a major production area, dropped significantly in October. The operating rate of ferromolybdenum in Liaoning Province in October was about 44%, a month-on-month decrease of 4 percentage points, leading the decline. In contrast, major ferromolybdenum plants in Henan and Shaanxi have their own molybdenum ore resources, so their operation was relatively stable, and the overall operating rate in the provinces fluctuated slightly. SMM data shows that the operating rate of the domestic ferromolybdenum industry in October was about 49%, a month-on-month decrease of 6 percentage points, marking the lowest operating rate of the year. In terms of cost, domestic ferromolybdenum plants generally suffered losses in October. According to SMM data, the monthly average price of 45% molybdenum concentrate in China in October was about 4,379.7 yuan per ton-degree, and the average cost of 60% ferromolybdenum was about 282,000 yuan per ton. However, the average price of the ferromolybdenum industry in October was about 276,700 yuan per ton, with an average monthly loss of 5,100 yuan per ton in the industry.

Overall, the domestic molybdenum market in China showed obvious structural differentiation characteristics in October. The output of molybdenum concentrate maintained steady growth, while the output of ferromolybdenum declined significantly. The difference in their market performance stemmed from the mismatch between supply and demand caused by the expansion of upstream mines and weak downstream demand. Since the beginning of this year, the molybdenum concentrate market has fluctuated in a relatively strong range, with uneven profit distribution in the industrial chain. Industry profits have concentrated on the mining end, while downstream molybdenum products have performed poorly in terms of profitability, and even generally faced losses. Against the background of slow adjustment in the demand structure, the profit distribution of the molybdenum market is difficult to reverse in the short term. Based on the calculation of domestic mine output and import data from September to October, the total supply of domestic molybdenum concentrate has recovered significantly compared with the previous period, while the downstream demand trend has decreased month-on-month. SMM estimates that the supply and demand of domestic molybdenum concentrate shifted to a surplus of about 1,900 metal tons in September, and the industry inventory was effectively replenished. In October, the international molybdenum oxide price weakened, and the import window for domestic molybdenum raw materials remained open. In addition, the supply of domestic molybdenum concentrate market increased, so SMM estimates that the supply and demand of domestic molybdenum concentrate maintained a slight surplus in October. In November, molybdenum concentrate mines are not expected to have much technical transformation or maintenance, so the industry output is expected to maintain slight fluctuations. However, the production scheduling of end-user stainless steel and special steel will decrease compared with October, and the demand for the molybdenum market will weaken. It is expected that the output of ferromolybdenum will be difficult to recover. Overall, the domestic molybdenum concentrate market in November is expected to mainly maintain the previous inventory accumulation trend.

Overall, the domestic molybdenum market in China showed obvious structural differentiation characteristics in October. The output of molybdenum concentrate maintained steady growth, while the output of ferromolybdenum declined significantly. The difference in their market performance stemmed from the mismatch between supply and demand caused by the expansion of upstream mines and weak downstream demand. Since the beginning of this year, the molybdenum concentrate market has fluctuated in a relatively strong range, with uneven profit distribution in the industrial chain. Industry profits have concentrated on the mining end, while downstream molybdenum products have performed poorly in terms of profitability, and even generally faced losses. Against the background of slow adjustment in the demand structure, the profit distribution of the molybdenum market is difficult to reverse in the short term. Based on the calculation of domestic mine output and import data from September to October, the total supply of domestic molybdenum concentrate has recovered significantly compared with the previous period, while the downstream demand trend has decreased month-on-month. SMM estimates that the supply and demand of domestic molybdenum concentrate shifted to a surplus of about 1,900 metal tons in September, and the industry inventory was effectively replenished. In October, the international molybdenum oxide price weakened, and the import window for domestic molybdenum raw materials remained open. In addition, the supply of domestic molybdenum concentrate market increased, so SMM estimates that the supply and demand of domestic molybdenum concentrate maintained a slight surplus in October. In November, molybdenum concentrate mines are not expected to have much technical transformation or maintenance, so the industry output is expected to maintain slight fluctuations. However, the production scheduling of end-user stainless steel and special steel will decrease compared with October, and the demand for the molybdenum market will weaken. It is expected that the output of ferromolybdenum will be difficult to recover. Overall, the domestic molybdenum concentrate market in November is expected to mainly maintain the previous inventory accumulation trend.

![Baiyin Nonferrous Group Co., Ltd. Copper Tendered 1 mt of Tellurium Ingots [SMM Report]](https://imgqn.smm.cn/usercenter/cgspx20251217171725.jpg)