On October 21, the APAC (10th) Ni-Cr-Mn Stainless Steel & New Energy Conference 2025, hosted by SMM Information & Technology Co., Ltd. (SMM), successfully concluded in Xiamen, Fujian!

This conference featured a wealth of insights and unprecedented scale, bringing together global authoritative experts, representatives from leading enterprises, and industry elites in the nickel-chromium-manganese and new energy sectors. Centered on the theme of "Exploring Development Directions and Solving Industry Challenges Together," it established an efficient and practical platform for industry exchange.

During the event, participants engaged in in-depth discussions on key topics such as cutting-edge industry trends, breakthroughs in technological innovation, and the evolution of market dynamics, fostering strategic consensus. This injected intellectual momentum into addressing industry bottlenecks and planning long-term development blueprints. The successful hosting of this conference not only significantly promoted synergy across the global industry chain but also laid a solid foundation for building a stable, efficient, and resilient supply chain system. Furthermore, it will provide crucial support for improving a price mechanism that is closely aligned with industry needs, possesses credibility and guidance, thereby assisting the industry in embarking on a new journey of collaborative win-win and high-quality development.

》Click to View On-site Conference Photos

Opening ceremony

Speaker

Logan Lu, CEO, SMM

2025 Outstanding Refined Nickel Price Submitter Release

2025 Outstanding NPI Price Submitter Release

October 20

Speech Session

Keynote: Indonesia's Policy Landscape: Roadmap and Future Prospects

Guest Speaker: Septian Hario Seto, National Economic Counci Republic of Indonesia

【Keynote】Lithium Carbonate Market: Price Fluctuations Driven by Supply-Demand Dynamics and Industry Prospects

Guest Speaker: Martin Ma, China GM, International Lithium Association

Global Lithium Resources Distribution

Based on comprehensive market survey data, driven by demand from power batteries, ESS batteries, and other factors, global lithium demand is expected to maintain an average annual growth rate of about 20% until 2030, reaching 4 million mt.

● South America and Australia account for about 60%-70% of global lithium reserves and nearly 80% of global production, and are expected to continue dominating resource supply until 2030.

● The lithium supply chain is still in its early stages of development and is growing at a double-digit rate. At the same time, achieving sustainability and green development across the entire supply chain presents challenges.

● Lithium plays a central role in the transition to renewable energy and the decarbonization of the global economy.

China's Lithium Carbonate Processing Landscape

According to the 2024 China Lithium Industry Development Report and the 2023 Jinxin Futures Research Institute Lithium Carbonate Special Report:

Lithium carbonate production locations and enterprise distribution are relatively concentrated. Jiangxi, Sichuan, and Qinghai provinces, as important sources of lepidolite, spodumene, and salt lake lithium, respectively, contributed to China's total lithium carbonate production exceeding 700,000 mt in 2024. By quality, battery-grade products accounted for over 50%. By raw material, raw ore smelting was the primary source of lithium carbonate production.

● Battery-grade lithium carbonate is primarily sourced from spodumene, with some derived from lepidolite, which is unique to China.

● Salt lake brine is primarily used to produce lithium carbonate.

【Keynote】Lithium Carbonate Market: Price Fluctuations Driven by Supply-Demand Dynamics and Industry Prospects

Guest Speaker: Zihan Wang, Senior Lithium Battery Analyst, SMM

【Panel】Nickel & Cobalt Supply Chain Reshuffle: Survival Strategies for DRC, Indonesia, and Chinese Players

Moderator: Wenhao Xiao, Cobalt Industry Researcher, SMM

Panelists:

Mamoko Egyul, CTCPM (Cellule Technique de Coordination et de Planification Minière)

Yiting Liu, Business Manager, Lygend Resources & Technology Co., Ltd.

Ines Kaempfer, Steering Committee Chair, Fair Cobalt Alliance (FCA)

【Keynote】Lithium Innovation at SQM Driving Electrification

Guest Speaker: Stefan Debruyne, Director of External Affairs, SQM

【Panel】The New Landscape of Lithium: South America's Lithium Triangle vs. Africa’s Lithium Belt

Moderator: Charlie Zhou, Senior Lithium Battery Analyst, SMM

Panelists:

Stefan Debruyne, Director of External Affairs, SQM

Shiyi Chen, Lithium Mine Operations, C&D Logistics Group Co., Ltd.

Xiangqi Qin, Deputy Director of Overseas Sales, Shenzhen Chengxin Lithium Group Co., Ltd.

【Keynote】Development of Lithium-ion Battery Industry in China in 2025

Guest Speaker: Yanlong Liu, Former Secretary-General, China Industrial Association of Power Sources

China is the world's largest producer of lithium-ion batteries.

Global lithium-ion battery production is primarily dominated by enterprises from China, Japan, and South Korea.

Driven by China's vigorous policies promoting new energy vehicles, the country's lithium-ion battery industry began rapid expansion starting in 2015, surpassing South Korea and Japan to become the global leader that year and gradually widening the gap.

In 2021, China's total lithium-ion battery production was 324 GWh, accounting for 57% of the global total. In 2022, production reached 738 GWh, increasing the global market share to 68.3%. In 2023, production was 910 GWh, with a global share of 71%. In 2024, production reached 1,170 GWh, up 28.6% YoY, expanding the global market share to 76%. From January to July 2025, China's lithium-ion battery production was approximately 940 GWh, up about 68% YoY, with a global share exceeding 80%.

【Keynote】Lithium Hydroxide: Next-Level Competition—From Single Transactions to Comprehensive One-Stop Service

Guest Speaker: Yu Sun, Deputy General Manager, Tianjin Greenway New Material Co., Ltd.

【Keynote】The Evolving Nickel World: Trends, Risks, and the Road Ahead

Guest Speaker: Thomas Feng, Head of Nickel Industry Research, SMM

【Keynote】The Current Status and Expansion of Global Nickel Product Market Applications

Guest Speaker: Pierre Derieux, Market Development Director, Nickel Institute

Nickel Consumption Uses

Analysis of Nickel's Main Application Areas

Stainless steel is the largest primary use sector for nickel, followed by batteries, which have been the fastest-growing area over the past decade.

Analysis of Nickel in Various End-Use Applications

Nickel has a very wide range of uses, spanning almost all industries, including consumer goods, catering and food processing, mobility and transportation, as well as construction, building and infrastructure, and energy sectors.

【Keynote】Overview of Global Nickel Market

Guest Speaker: Brian, Asian Area Nickel Analyst, Norilsk Nickel Metals Trading (Shanghai) Co., Ltd.

(This presentation is not publicly available at the speaker's request)

【Panel】ESG Transformation in the Battery Industry: From Green Metals to Circular Practices

Moderator:

Weichao Chen, Chief representative of China, Nickel Institute

Panelists:

Elwin Meng, Global Intelligence Manager, Umicore

Killian Xu, General Manager of ESG Office, Rept Battero Energy Co., Ltd

Aslan Liu, Senior Manager of ESG, Sunwoda Electronic Co., Ltd.

Zhonghui Zhu, Manager of ESG Management Department, GEM Co., Ltd.

Keynote: The Global Battery Alliance Battery Passport: Meeting International Stakeholder Expectations for Sustainability and Supply Chain Traceability

Guest Speaker: Graham Lee, Head of the Battery Passport Programme, Global Battery Alliance

October 21

Speech Session

Keynote: China's Ferrochrome Supply & Demand Balance and Outlook for 2026

Guest Speaker: Junhong Zhang, General Manager, Shanghai Liying Industry Co., Ltd.

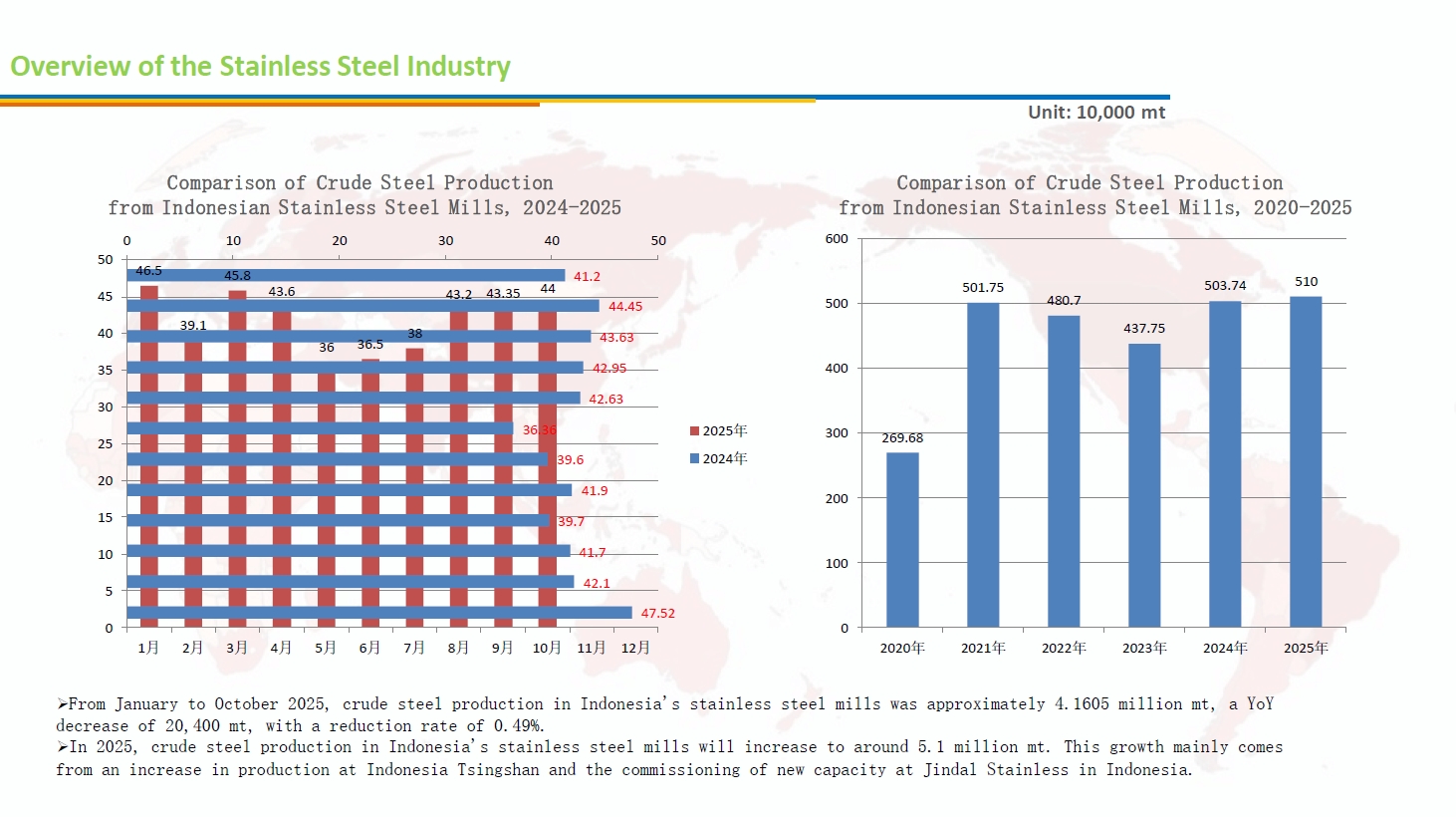

Stainless Steel Industry Overview

ØFrom January to October 2025, the crude steel production of 43 stainless steel enterprises in China was approximately 32.4897 million mt, an increase of 950,500 mt, or up 3.01% YoY.

ØChina's stainless steel crude steel production is expected to reach 41-41.5 million mt in 2025.

ØFrom January to October 2025, Indonesia's stainless steel crude steel production was approximately 4.1605 million mt, a decrease of 20,400 mt compared to the same period last year, down 0.49% YoY.

ØIndonesia's stainless steel crude steel production is expected to increase to around 5.1 million mt in 2025, primarily driven by increased production from Indonesia Tsingshan and the commissioning of new capacity at Indonesia Jindalai.

Brief Analysis of China's Stainless Steel Import and Export Data

ØChina's Stainless Steel Import Data

CISA: From January to August 2025, stainless steel imports were approximately 1.0176 million mt, a decrease of 30.94% (down 23.32% YoY). The main country contributing to the decline was Indonesia.

ØChina's Stainless Steel Export Data

CISA: From January to August 2025, stainless steel exports were approximately 3.3642 million mt, an increase of 100,900 mt, up 3.09% YoY. Major export destinations: Vietnam, Russia, Turkey, South Korea, etc.

China's Net Exports Data

CISA: Stainless steel net exports totaled 1.6726 million mt from January to August 2025, an increase of 410,300 mt YoY; the YoY growth rate was 21.19%.

Industry Status

Continuous Expansion → Supply-Demand Imbalance → Profit Decline

Ferrochrome Industry Overview

Ferrochrome Industry Summary

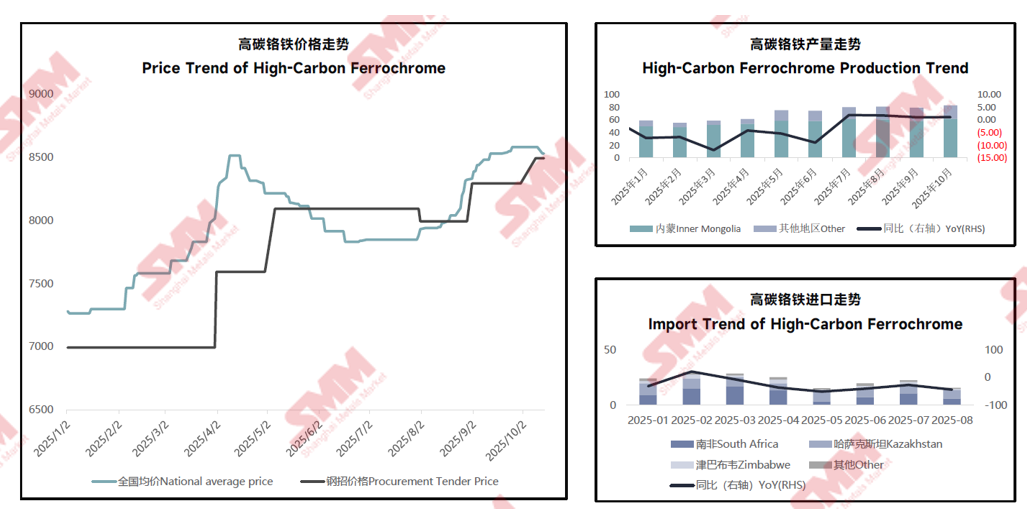

High-carbon ferrochrome production in China was 6.5406 million mt from January to September 2025, a decrease of 192,700 mt YoY.

China's high-carbon ferrochrome capacity was 15.61 million mt in 2025, with an expected increase of 600,000 mt in Q4.

Inner Mongolia's high-carbon ferrochrome production was 5.0034 million mt from January to September 2025, an increase of 431,800 mt YoY, accounting for 76.5% of the national total.

China's high-carbon ferrochrome imports were 1.8293 million mt from January to August 2025, a decrease of 701,800 mt YoY, a YoY decline of 27.73%. Among them, imports from South Africa were 830,500 mt, accounting for 45.4%.

Additionally, he also elaborated on the tender price of high-carbon ferrochrome by Chinese stainless steel mills in 2025, the tender price of high-carbon ferrochrome in Europe in 2025, the comparison of supply increments between Chinese stainless steel and high-carbon ferrochrome in 2024, the comparison of supply between Chinese stainless steel and high-carbon ferrochrome in September 2025, the comparison of high-carbon ferrochrome exports from selected countries from 2024 to 2025, the comparison of high-carbon ferrochrome imports for selected countries (South Korea, Japan, US, Indonesia) from 2024 to 2025, and the comparison of high-carbon ferrochrome production by country from 2023 to 2024.

Keynote: India’s Chrome Industry Overview and Its Position in the Future International Market

Guest Speaker: Vivek Nishant Nath, Chief General Manager, Odisha Mining Corporation Ltd

Keynote: Outlook for Chinese Stainless Steel Export Market

Guest Speaker: Lily Li, Stainless Steel Procurement Manager, Trasteel Trading Holding SA

Current Status of China's Stainless Steel Export Business

In January 2025, Shanghai Metals Market (SMM) released the following statistics for China's crude stainless steel production, import and export volume, and apparent consumption for 2024:

I. China's Crude Stainless Steel Production

In 2024, the crude steel production of 34 domestic stainless steel mills was 37.8513 million mt, an increase of 1.1121 million mt, or 3.03%, YoY. Specifically: the 200-series output was 10.6039 million mt, down 109,700 mt, or 1.02%, YoY, with its share decreasing by 1.15 percentage points to 28.01%; the 300-series output was 19.8927 million mt, up 527,800 mt, or 2.73%, YoY, with its share decreasing by 0.15 percentage points to 52.55%; the 400-series output was 7.3547 million mt, up 694,000 mt, or 10.42%, YoY, with its share increasing by 1.3 percentage points to 19.43%.

II. China's Stainless Steel Import and Export Volume

In 2024, China's total stainless steel imports were 1.8777 million mt, a decrease of 193,500 mt, or 9.3%, YoY. Among these, China's total stainless steel imports from Indonesia were 1.5642 million mt, down 130,500 mt, or 7.7%, YoY.

In 2024, China's total stainless steel exports were 5.0172 million mt, an increase of 999,600 mt, or 24.88%, YoY.

In 2024, China's net stainless steel exports totaled 3.1395 million mt, an increase of 1.1931 million mt, or 61.3%, YoY.

III. China's Stainless Steel Apparent Consumption

In 2024, China's apparent consumption of stainless steel was 34.7118 million mt, a decrease of 81,000 mt, or 0.23% YoY.

In 2024, China's actual consumption of stainless steel was 34.2104 million mt, a decrease of 264,800 mt, or 0.77% YoY.

Keynote: Stainless Steel: The Indian Growth Story and Future Outlook

Guest Speaker: Mr. Rajamani Krishnamurti, President, India Stainless Steel Development Association

Overview

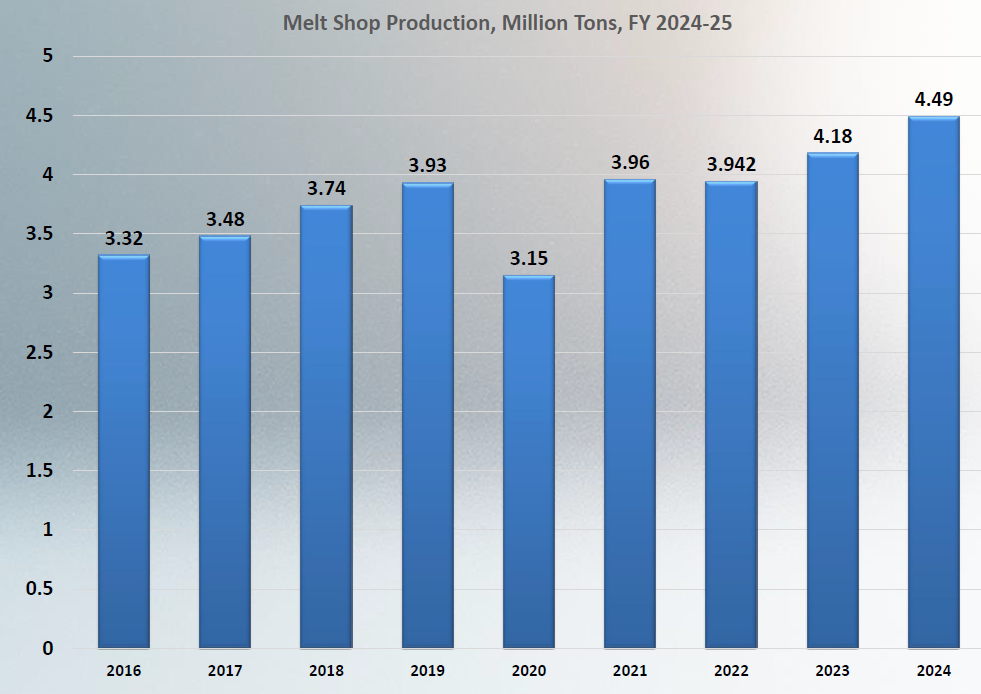

Current Status of India's Melt Shop Production

• India's melt shop production grew by over 7% in 2024;

• India ranks third globally in melt shop production, behind only China and Indonesia.

Current Status of Consumption in India

• India is the world's second-largest consumer of stainless steel.

• Consumption reached 4.8 million mt in FY 2024-2025, an increase of nearly 8% from the previous year.

• Robust consumption growth was seen in building and construction, infrastructure projects, structural steel and rebar, process industries, railways, and transportation.

Current Status of Production by Grade in India

• The 300-series showed good growth;

• The 200-series remains dominant in pipes, tubes, and utensils;

• The 400-series grew in railways and infrastructure.

Current Status of End-Use Applications in India

ABC sector growth was robust, increasing by over 12% last year.

India's development pace is accelerating, with unlimited potential.

Keynote: Trends, Challenges, and Future Outlook of Demand and Supply in the Japanese Stainless Steel Industry

Guest Speaker: Yuji Tanamichi, CEO, Iruniverse

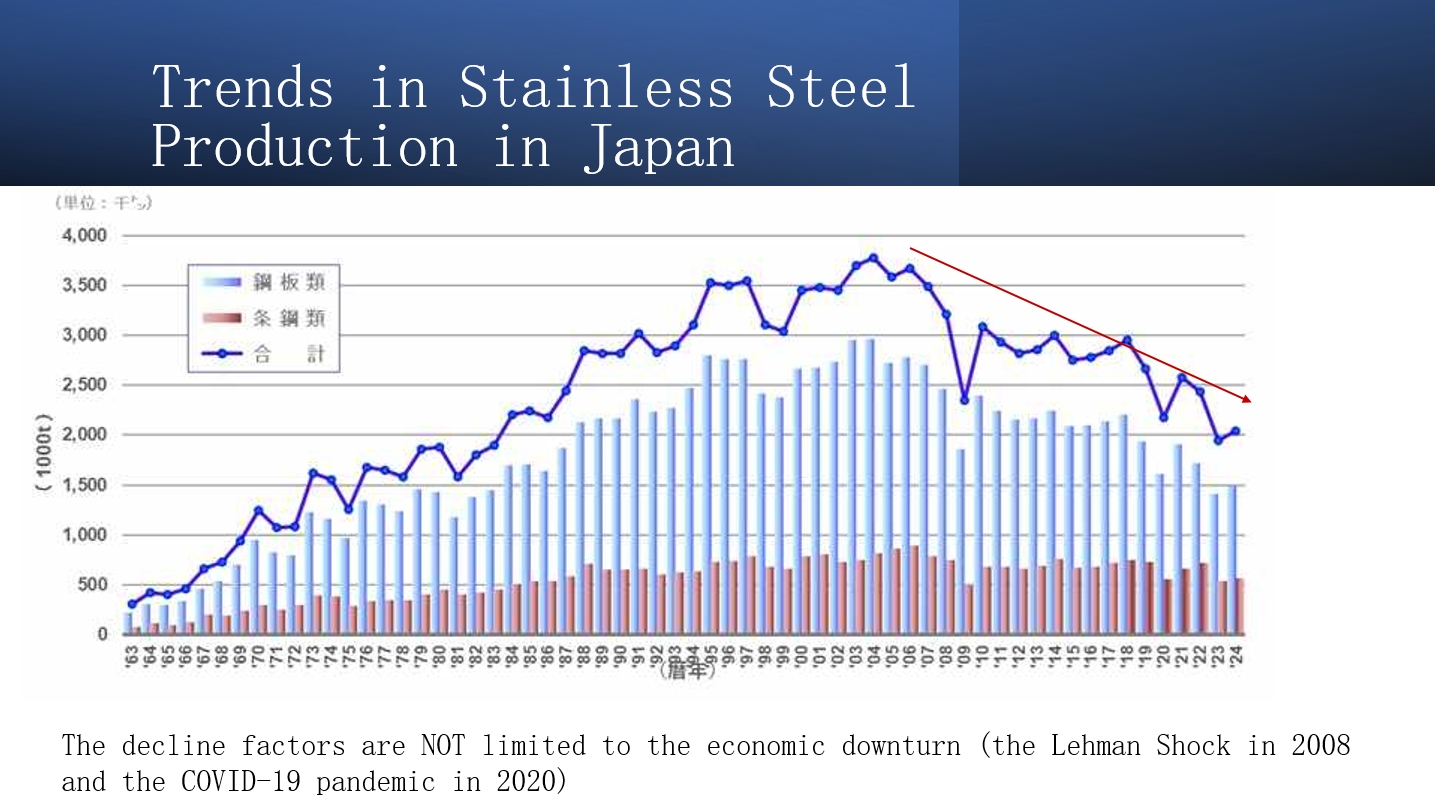

Trend in Japanese Stainless Steel Production

Japan's stainless steel production has fallen below 2 million mt. Due to increased stainless steel imports, this downward trend is expected to continue.

Keynote: The Use of Molybdenum in High Strength Stainless Steels

Guest Speaker: Fabio Ries, Senior Analyst, International Molybdenum Association

Addressing Challenges

Globally, humanity faces increasingly severe challenges: the increase in climate change and extreme natural disasters; the need to enhance efficiency and productivity to make optimal use of limited resources; the depletion of natural resources and the necessity to survive in harsh environments (space, deep sea, deserts, extreme climates...).

Technological Development: Geopolitical Competition and Economic Uncertainty.

Pursuing Excellent Performance

One of the answers to these challenges is technology: becoming bigger, faster, and stronger at an astonishing pace:

- Trains can reach speeds of 1,000 km/h, and cars can travel at 500 km/h;

- Space travel has become a reality

- Humans are settling in deserts, Antarctica..., and even Mars

- Power transmission speed has increased by more than 10 years compared to a decade ago.

- A single wind turbine now generates more power than an entire wind farm did 20 years ago…

Enhancing Steel Performance

Optimizing Drivers: Economic Drivers; Same Performance, Lower Cost.

Performance Drivers: Improved Performance at Equal Cost; Enhanced Performance at Higher Cost to Meet New Demands.

Ecological/Social/Political Drivers: Reducing Carbon Dioxide Emissions.

Molybdenum Enhances Stainless Steel Performance

When standard grades of stainless steel fall short, molybdenum serves as a high-quality upgrade alloying element.

Keynote: From Sand to Cells: Building an Indonesia–China Silica Corridor for Stainless, Glass, & EV Value Chains

Guest Speaker: Umar Rivaldy Pulukadang, Secretary General, PERTAMISI

Keynote: Analysis of the Current Market Status and Trends of Metal Feedstock Such as Chromium, Manganese, and Molybdenum

Guest Speakers: Sia Mao, Senior Chromium Analyst, SMM

Sophie Zang, Senior Manganese Analyst, SMM

Lindy Lee, Senior Tungsten and Molybdenum Industry Analyst, SMM

Brief Analysis of the Molybdenum Market Supply-Demand Dynamics Driven by New Energy and Other Sectors

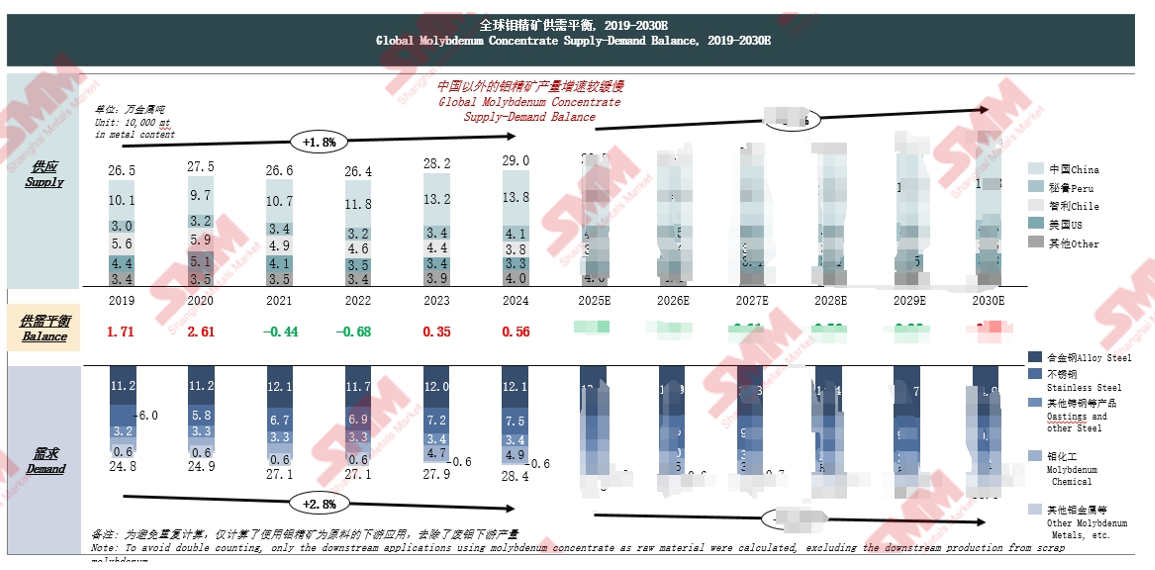

Global Molybdenum Concentrate Supply-Demand Balance: Supply Gap to Narrow Over the Next Five Years

This conclusion is based on the global molybdenum concentrate supply-demand balance from 2019 to 2030E. From the supply side, molybdenum concentrate production growth outside China is relatively slow.

A Panoramic View of Molybdenum-Related Policies in Major Global Economies: Divergent Strategic Orientations Drive Restructuring of the Global Molybdenum Industry Chain

It introduces the policy directions, specific policies, and impacts for China, the European Union, the US, Peru, Chile, Japan, South Korea, and others.

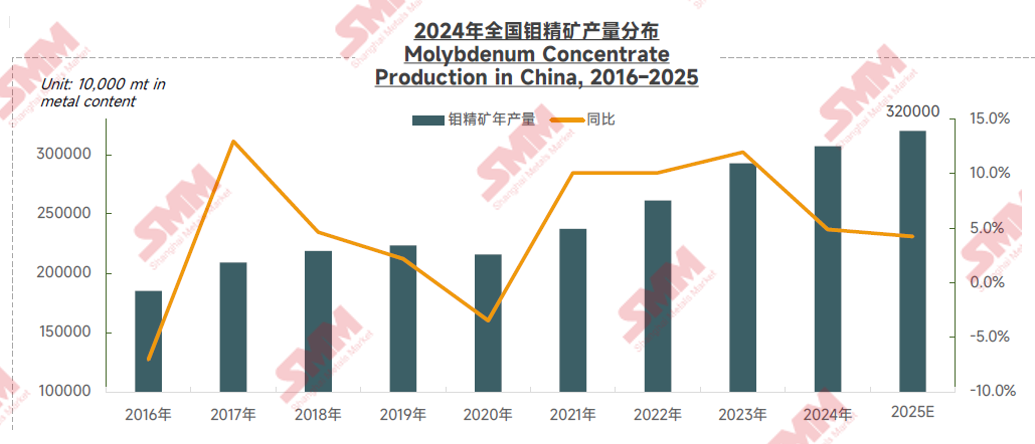

Slowing Growth in China's Molybdenum Concentrate Production and Declining Mine Grade Constrain Global Molybdenum Supply Growth

China is a major global supplier and consumer of molybdenum. In 2024, China's molybdenum concentrate production was approximately 138,000 mt, accounting for 47.7% of global production and ranking first worldwide. However, since 2024, environmental protection checks on molybdenum concentrate mines and rising mining costs due to low ore grades have constrained industry production growth. In 2025, technological transformations at some mines mid-year, coupled with declining operating rates at others, led to a further slowdown in domestic molybdenum concentrate production growth. SMM expects China's total molybdenum concentrate production to reach 320,000 mt in physical content, or approximately 143,000 mt in metal content, in 2025, up 3.4% YoY, while global supply growth is projected to be about 1.9%.

Dual Drivers of Global New Energy and Steel Industry Upgrades Fuel Expansion of Molybdenum Demand in the Chinese Market

The Chinese Market Amid Global Chromium Resource Pattern Transformation

High-Carbon Ferrochrome Prices Show Significant Fluctuations in 2025, Overall Trend Fluctuates Upward Amid Tight Supply

She covers topics such as high-carbon ferrochrome price trends, production trends, and import trends.

Overseas Production Cuts Create Short-Term Supply Gap in Ferrochrome, but New Capacity Additions Expected to Maintain Overall Market Surplus

Stainless Steel Manganese Raw Material: Market Development Status and Future Outlook

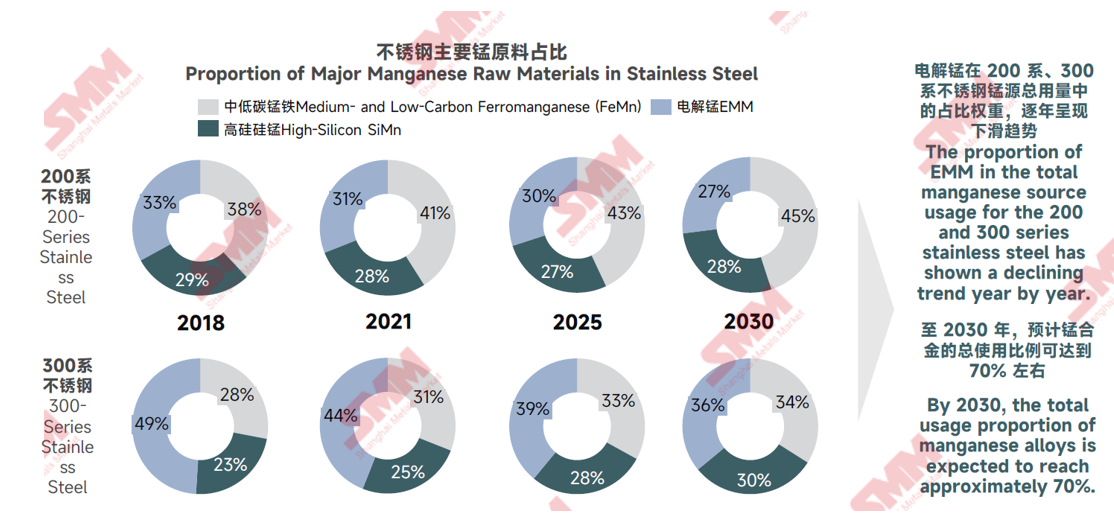

Stainless Steel Manganese Source Selection: Proportion of Ferromanganese and SiMn Alloy May Continue to Increase

In the analysis of the proportion of main manganese raw materials in stainless steel from 2018 to 2030: The share of EMM in the total manganese source usage for 200-series and 300-series stainless steel is expected to show a declining trend year by year. By 2030, the total usage proportion of manganese alloys is projected to reach around 70%.

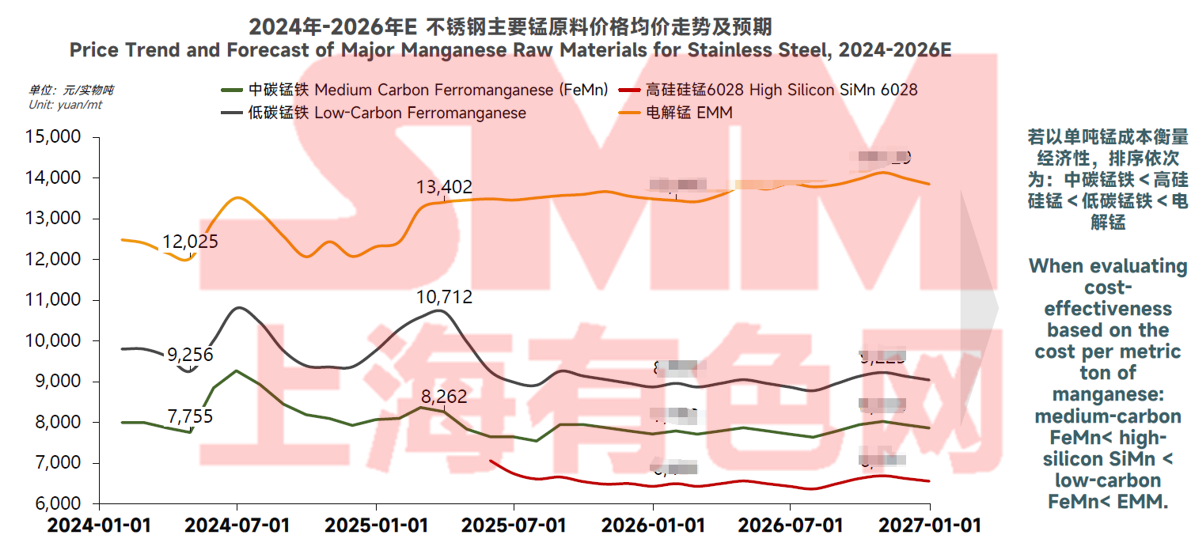

Stainless Steel Manganese Source Price Trends: Economic Advantage of Medium-Carbon Ferromanganese Becomes Prominent

When combining the average price trends and expectations of main manganese raw materials for stainless steel from 2024 to 2026, it was indicated that: If measuring economics based on single mt manganese cost, the order is as follows: medium-carbon ferromanganese < high-silicon SiMn < low-carbon ferromanganese < EMM.

Presentation Topic: Global Stainless Steel Market Outlook

Guest Speaker: Tim Collins , Secretary-General, World Stainless Association

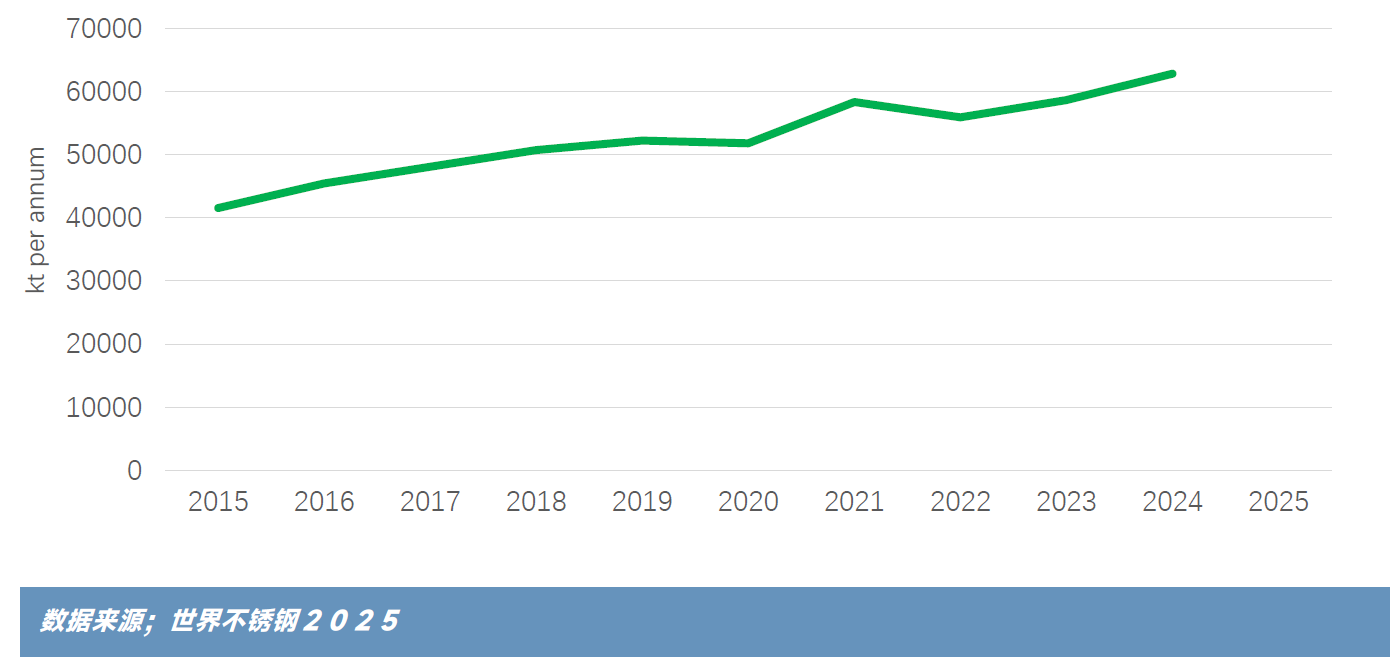

Background: Global Stainless Steel Melt Shop Production Over the Past 10 Years

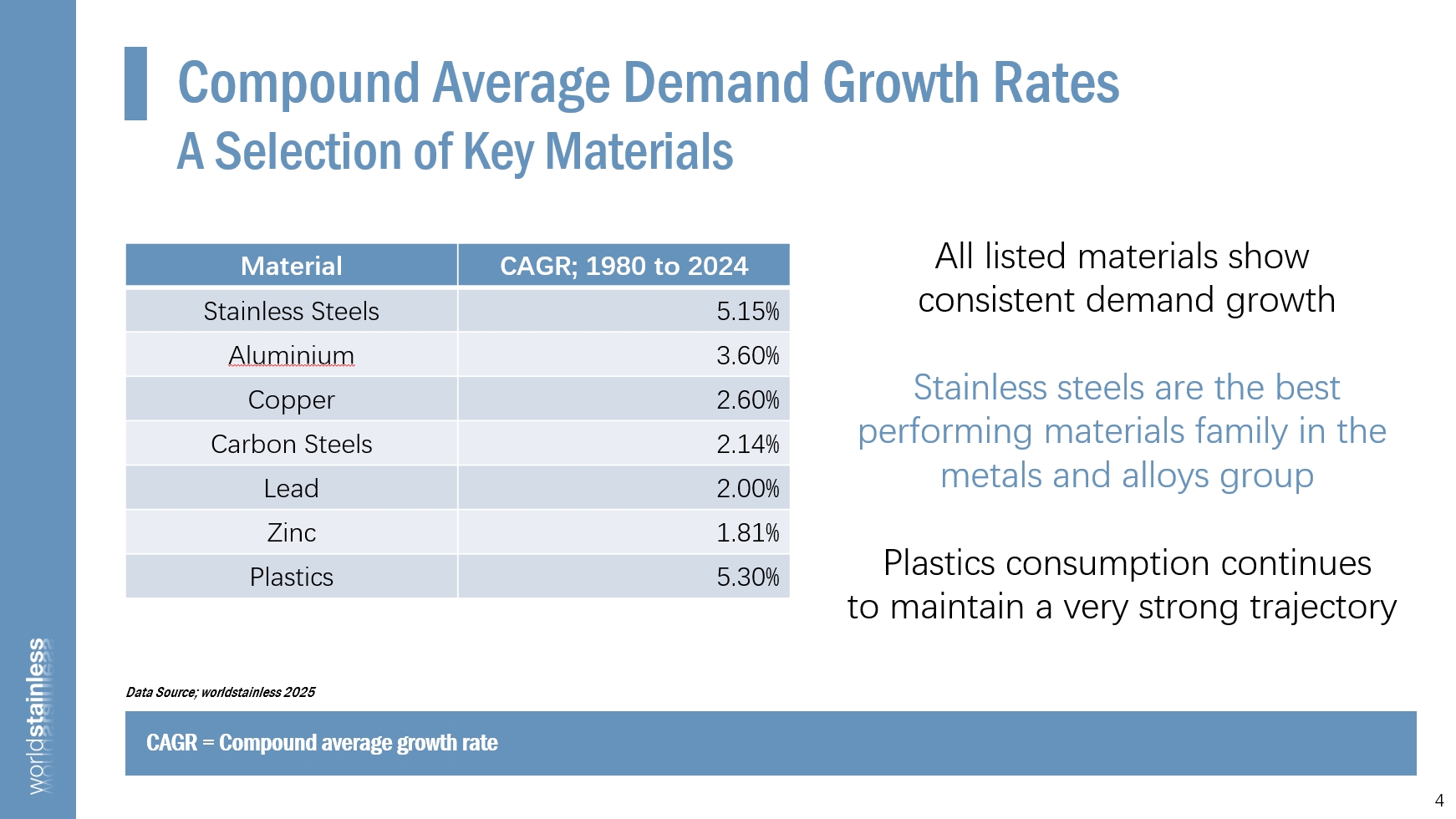

Compound Annual Demand Growth Rate

Some Key Materials

All listed data show a continuously growing demand.

Stainless steel is the best-performing material in the metal and alloy group.

Plastic consumption continues to maintain a very strong growth trajectory.

Stainless Steel Production; Grade Group Distribution

Austenitic, especially 300-series grades, still dominate total production.

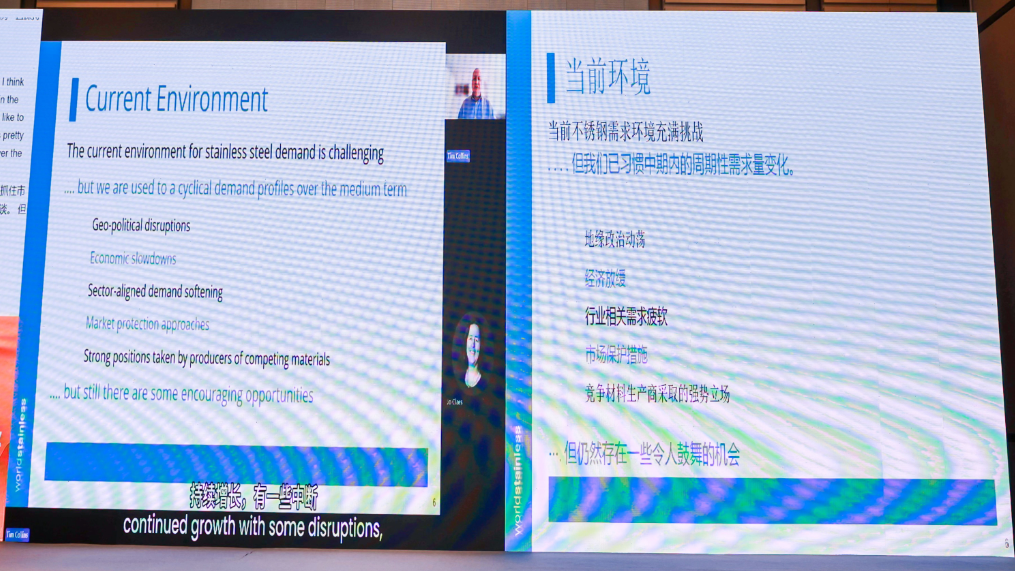

Current Environment

The current stainless steel demand environment is challenging... but we are accustomed to cyclical demand changes in the medium term.

Geopolitical turmoil, economic slowdown, weak industry-related demand, market protection measures, aggressive stances by competing material producers…

However, there are still some encouraging opportunities.

Do We Know Our Competitors?

►Although there are always new growth markets for stainless steel

Driven by megatrends, new technologies, and major developments, such as small modular reactors

►Some of these market opportunities may develop slowly

Stainless steel has the potential to substitute other materials in existing markets

Keynote: Global Stainless Steel Market: Supply and Demand Forecast and Material Substitutability Analysis

Guest Speaker: Sibyl Yang, Senior Nickel Analyst, SMM

Recent Review of the Stainless Steel Market

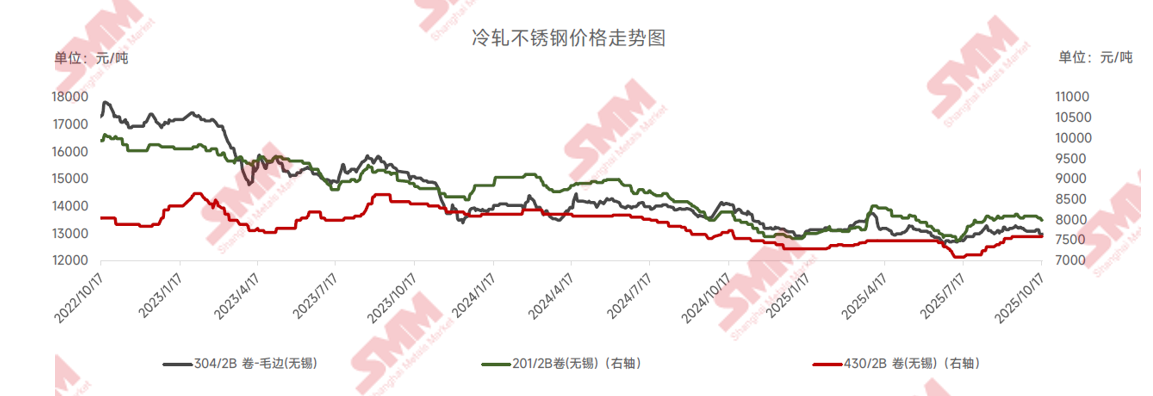

Cold-Rolled Stainless Steel Prices: Weak Traditional Demand and Overcapacity Lead to Continued Price Decline

►SMM Analysis

• In recent years, stainless steel prices have generally weakened. Since 2022, cumulative declines for 201, 304, and 430 stainless steel were 16%, 24%, and 10%, respectively. Reasons include weak traditional demand due to a sluggish real estate sector, expanded stainless steel, nickel, and chromium alloy capacity leading to looser supply and insufficient cost support, and industry profits shifting to the mine segment.

• Analyzing the market situation within the year, stainless steel prices were already at relatively low levels at the beginning of this year, against the backdrop of sustained high production schedules in 2024. In early 2025, affected by Indonesia's nickel ore quota approvals, NPI prices climbed. Combined with maintenance carried out by stainless steel mills at the beginning of the year, market supply decreased, leading to a rebound from low prices. However, by March, stainless steel mills gradually completed maintenance, and production broke through historical peaks, keeping supply at high levels. Furthermore, in April, the US's reciprocal tariff policy sparked market concerns, causing prices to weaken again, with prices for 200-series, 300-series, and 400-series stainless steel all falling to near five-year lows. Currently, amid rising global trade protectionism and recurring trade frictions, the US Fed has begun an interest rate cut cycle and stopped balance sheet reduction. Simultaneously, China's implementation of "anti-involution, stable growth" policies and increased infrastructure investment stimulus have led to an increasingly intense tug-of-war between longs and shorts in the stainless steel market, intertwined with strong expectations and weak reality, resulting in prices fluctuating.

Price Spread Between Cold-Rolled and Hot-Rolled Stainless Steel: Cold-Rolled Capacity Rises, Market Competition Intensifies, and the Spread Gradually Narrows

► SMM Analysis

• In recent years, domestic cold-rolled capacity has grown rapidly. Enterprises represented by Yongjin Shares and Hongwang Group have continued to expand, making the supply of cold-rolled resources increasingly abundant. At the same time, the overall increase in social inventory of stainless steel in recent years has led to a gradual flattening of the fluctuation in the price spread between cold-rolled and hot-rolled stainless steel.

• The demand for cold-rolled products is closely related to the prosperity of industries such as home appliances and architectural decoration. In recent years, demand in these areas has been relatively weak, thereby increasing sales pressure for cold-rolled products and making it difficult to maintain high prices. In contrast, hot-rolled products, as industrial basic materials, have maintained relative stability in some demand areas such as chemical energy and equipment manufacturing. Additionally, hot-rolled is also the raw material for cold-rolled, and the expansion of cold-rolled capacity has, to some extent, supported the rigid demand for hot-rolled. Furthermore, advancements and popularization of cold-rolling technology have significantly reduced processing costs, thereby compressing the premium of cold-rolled over hot-rolled.

Stainless Steel Supply-Demand Balance: Dual Growth in Supply and Demand with Narrowed Balance Fluctuations, Market Adjustments Amid Overcapacity

► SMM Analysis

• In recent years, both supply and demand in the stainless steel industry have maintained growth, but the fluctuation range of market balance has narrowed. Despite weak demand in traditional downstream sectors such as real estate, demand in areas like home appliances and automobiles continues to grow, driven by domestic policies such as trade-in programs. At the same time, emerging application fields including water supply systems, new energy, and high-end equipment are continuously expanding, coupled with the rapid industrial development in Southeast Asia boosting export demand for equipment and machine tools, collectively supporting stainless steel consumption.

• Before 2024, domestic stainless steel capacity continued to expand, while demand growth gradually slowed down, leading to a prolonged state of supply surplus in the industry. Profit margins significantly narrowed, with some enterprises facing minimal profits or even losses. Combined with persistently high inventory levels, steel mills no longer blindly pursued full-capacity operation, instead flexibly adjusting supply through measures such as maintenance, production cuts, and demand-based production scheduling.

• In addition, declining profit margins have also affected the trade sector, reducing speculative stockpiling and shifting toward low-inventory, high-turnover business strategies. Steel mills regulate the pace of shipments through large agents, further promoting dynamic adjustments in market supply and demand.

Check-in & Highlights

》Click to View Conference Highlights

With this, the APAC (10th) Ni-Cr-Mn Stainless Steel & New Energy Conference 2025 concluded successfully!

We extend our gratitude to all our industry colleagues for your assistance and support.Let us reconvene next year.

![[SMM Analysis] This Week, the MHP and High-Grade Nickel Matte Markets Showed a Pattern of Weak Supply and Demand on Both Sides, with the Coefficient Remaining Stable](https://imgqn.smm.cn/usercenter/qLeLR20251217171733.jpg)

![[SMM Nickel Midday Commentary] On April 3, nickel prices moved sideways, as Iran and Oman drafted an agreement on the regulation of the Strait of Hormuz](https://imgqn.smm.cn/usercenter/GmHLU20251217171733.jpg)

![[SMM Nickel Flash] Iran and Oman to Jointly Manage the Strait of Hormuz](https://imgqn.smm.cn/usercenter/yUOUz20251217171732.jpg)