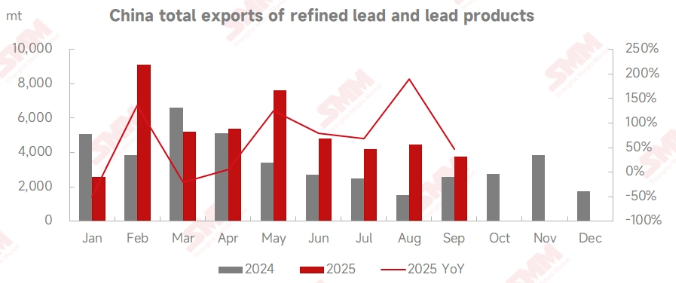

According to customs data, China's refined lead exports in September 2025 totaled 1,486 mt, down 46% MoM but up 66.1% YoY. Total exports of refined lead and lead products from January to September reached 47,175 mt, up 41.38% YoY. On the import side, China imported 1,508 mt of refined lead and 13,864 mt of lead alloy in September. Total imports of refined lead and lead products in the first nine months amounted to 121,945 mt, down 34.87% YoY.

In September, both supply and demand in the domestic lead ingot market declined. In contrast, downstream markets such as e-bike and automotive lead-acid batteries entered their traditional peak consumption season, with lead-acid battery producers showing higher operating enthusiasm compared to August. Lead prices fluctuated rangebound in early September, then rose firmly in mid-month, with the SHFE lead 2511 contract hitting a high of 17,220 yuan/mt, opening the import arbitrage window for lead ingots. Approaching October, expectations of lead ingot inventory buildup during the National Day & Mid-Autumn Festival holiday, combined with planned concentrated production resumptions at secondary lead smelters, prompted bulls to reduce positions on fears of price declines. SHFE lead weakened, giving back most of its gains, while import lead trading activity slowed.

In early October, macro sentiment turned bearish, coupled with a buildup in LME lead inventories, which increased by over 10,000 mt week-on-week. LME lead fell below the 2,000 psychological mark, with its overall trading center shifting lower. Short-term macro uncertainties remain high, and overseas lead consumption has underperformed compared to the domestic market, raising the possibility of more lead ingots being diverted to the Chinese market in October.

As maintenance at primary lead smelters in north China has not yet concluded, and the pace of production resumptions at secondary lead producers has been slower than expected, regional tightness in domestic lead ingot supply persisted in mid-October. Spot market availability remained limited, and smelters generally refused to budge on prices. Some companies reported that import lead ingot offers rose compared to September. For example, material that was offered at a discount of 150-100 yuan/mt against the SMM #1 lead average price for delivery-to-factory in September required parity in October; some material rich in metals such as antimony and tin required a premium of around 100 yuan/mt for delivery.

Data Source Statement: Except for publicly available information, other data are derived by SMM based on public information, market communication, and SMM's internal database model, and are for reference only, not constituting decision-making advice.