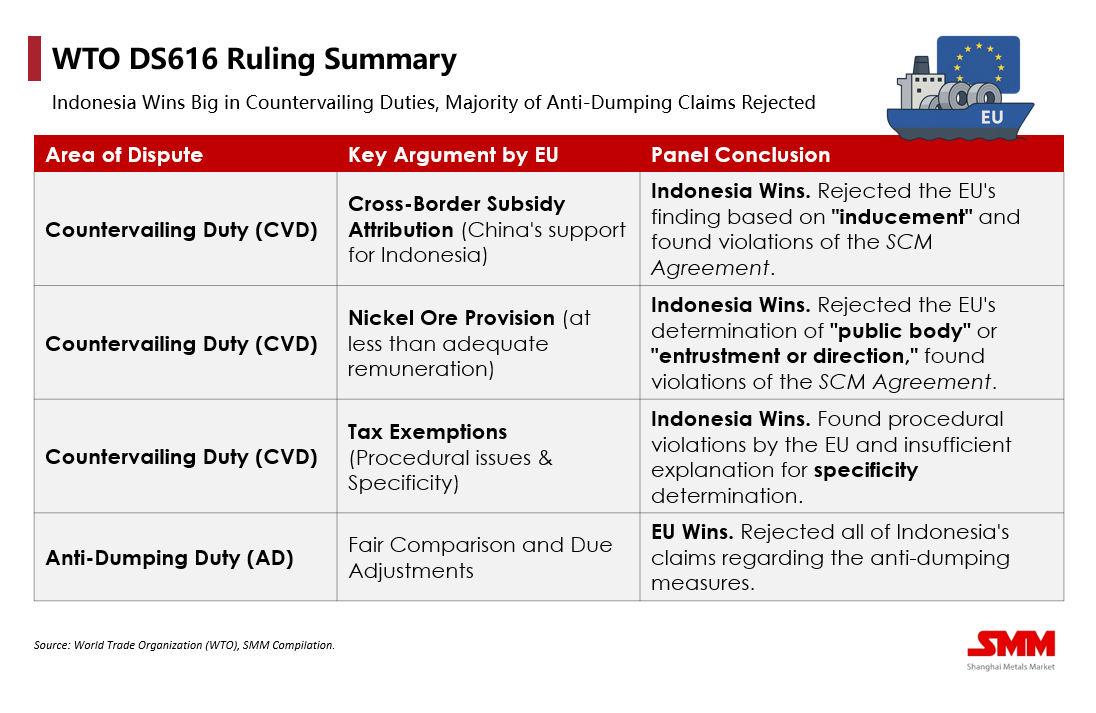

The World Trade Organization (WTO) panel, in its DS616 ruling announced on October 2, 2025, found the European Union (EU) to be in violation of key provisions concerning its anti-subsidy duties on Indonesian cold-rolled stainless steel. On the surface, this represents a significant triumph for Indonesia in a traditional trade dispute. However, we view the win as a "Pyrrhic Victory": the ruling’s benefits are immediately nullified by procedural obstacles, and the entire episode is overshadowed by the imminent structural shock of the Carbon Border Adjustment Mechanism (CBAM). This is not the end of a trade era, but the dawn of a far more challenging one.

Panel Verdict Highlights: EU's "Triple Failure" on Subsidy Claims

The WTO panel's report decisively rejected three key accusations made by the EU in determining the existence of countervailable subsidies, handing Indonesia a majority of substantive victories:

Cross-Border Subsidy Attribution: The EU's "Inducement Theory" Overturned

-

Point of Contention: The EU sought to attribute preferential financing and support provided by foreign sources (China) to Indonesian stainless steel producers back to the Indonesian government for the purpose of levying countervailing duties.

-

Panel Ruling: The panel explicitly stated that the EU's reliance on the mere theory of "inducement" to attribute a foreign financial contribution (from China) to the Indonesian government was inconsistent with Article 1.1(a)(1) of the SCM Agreement (Agreement on Subsidies and Countervailing Measures).

-

Significance: This ruling curtails the EU's attempts to broaden the definition of "subsidy" and trace cross-border financial contributions in its trade investigations, establishing an important constraint on subsidy determination in today's complex global supply chains.

Nickel Ore Case: Failure to Prove Public Body Status or Entrustment/Direction

-

Point of Contention: The EU alleged that the Indonesian government provided nickel ore to domestic stainless steel producers at less than adequate remuneration.

-

Panel Ruling: The panel ruled that the EU failed to provide sufficient evidence that all Indonesian nickel mining companies were "public bodies," nor did it prove that the Indonesian government "entrusted or directed" private bodies to provide the nickel ore. This directly refuted the EU's finding on the existence of a financial contribution, violating SCM Agreement Article 1.1(a)(1).

Tax Exemptions: Procedural Flaw and Insufficient Specificity

-

Key Findings: The panel found a procedural violation, determining that the EU did not grant the Indonesian government an opportunity for "further review" when treating import duty exemptions as a subsidy. Furthermore, the EU's finding on the "specificity" of income tax allowance schemes lacked a rational and sufficient explanation, constituting another violation.

Verdict Summary: Anti-Subsidy Duties Must Be Adjusted, Anti-Dumping Retained

While the panel rejected most of Indonesia's claims regarding the anti-dumping measures, the report dismantled the key pillars supporting the EU’s anti-subsidy determination. This implies the EU must amend or re-substantiate the relevant anti-subsidy measures. However, with the EU set to appeal and the WTO Appellate Body paralyzed, the report is currently unadopted, meaning the existing duties will not automatically lapse in the short term.

SMM Analysis: The "Appellate Black Hole" and the Real Game Changer

Due to the ongoing paralysis of the WTO Appellate Body, the EU can simply appeal the decision, effectively consigning the case to an "appellate black hole" indefinitely. This ensures the 21.4% anti-subsidy duty remains in effect, rendering the ruling commercially irrelevant for the immediate future. Even without the anti-subsidy tariff, Indonesian stainless steel still faces the double constraint of the upheld anti-dumping duties and safeguard quotas in the EU market.

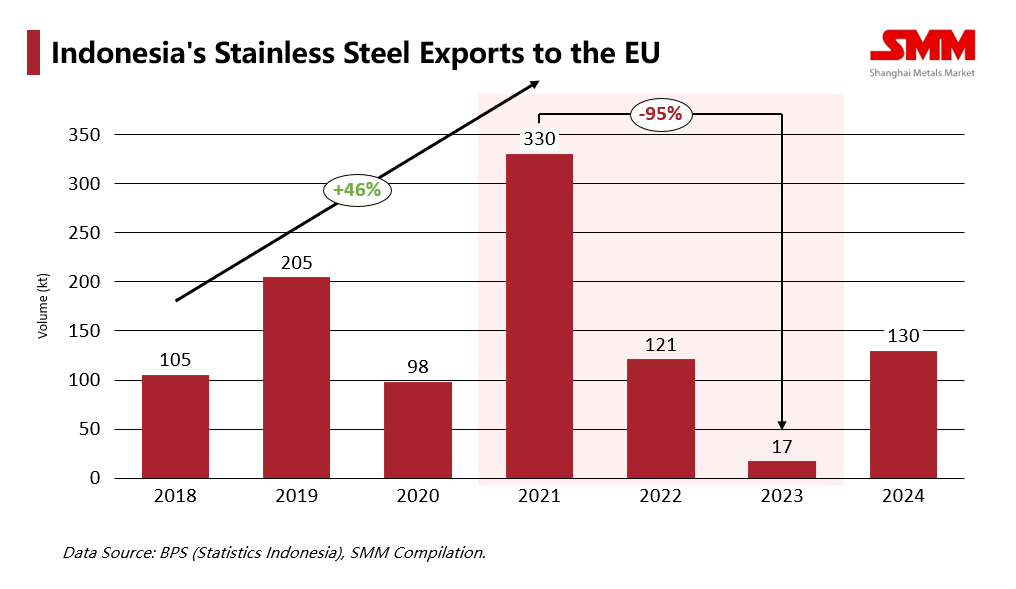

1. SMM Insights: Export recovery remains constrained as the "policy handbrake" is still partially engaged.

Under the combined impact of the EU's safeguard measures and the "double-duties" (anti-dumping/anti-subsidy), Indonesian stainless steel exports to the EU plummeted to a trough of just 17,100 tonnes in 2023. Even with a rebound in 2024, volumes remain at only about 39% of the 2021 peak (330,000 tonnes).

The WTO ruling theoretically removes the primary "policy handbrake" by rejecting the dominant 21.4% anti-subsidy duty, opening a potential path for nickel downstream products to re-enter the European market.

However, the appeal mechanism means this theoretical "handbrake release" cannot be realized quickly. Exports remain legally bound by current tariffs, and any actual trade flow recovery must await the EU's legal or political action.

2. The True "Game Changer": CBAM's Structural Challenge

The real threat to the Indonesian stainless steel sector is no longer traditional trade litigation, but the EU's CBAM, a novel green trade barrier. This poses a fundamental, potentially existential, challenge. Indonesia’s core competitive advantage—abundant nickel resources and low-cost energy primarily from captive coal-fired power plants—is precisely its carbon cost Achilles' heel. The dominant Nickel Pig Iron (NPI) production method (RKEF) is notoriously high-energy and high-emission.

Core Challenge: CBAM will officially impose charges starting in 2026. Preliminary estimates suggest the "carbon tariff" Indonesia's high-carbon-footprint products must pay could easily equal or even exceed the controversial 21.4% anti-subsidy duty. This perfectly illustrates the current predicament: clearing a relatively small roadblock (the anti-subsidy tariff) only to find the opponent is building a higher, stronger wall (CBAM) right in front of you.

3. Overall Market Implications: Noise vs. Strategic Value

What we are witnessing is not a market fluctuation caused by a single trade ruling, but a profound global industrial restructuring driven by the environmental agenda. The WTO ruling is not the climax, but an interlude in a much larger overture of change.

-

Short-Term Impact: Market "Noise." Since the EU will inevitably use the appeal mechanism to delay implementation, current tariffs will remain unchanged, and the market fundamentals will not shift. Expectations for a full-scale return of Indonesian stainless steel to Europe cannot be met, and actual international trade flows will not be substantively altered. This only serves to heighten market uncertainty in the short run.

-

Strategic Value: Negotiating Chip. The ruling’s true value lies outside the market—it provides Indonesia with a crucial strategic bargaining chip. Its most important application will be to strengthen Indonesia’s hand in the ongoing Indonesia-EU Comprehensive Economic Partnership Agreement (CEPA) negotiations. Indonesia can leverage this official WTO finding as proof of EU protectionism, securing a more favourable position and potential concessions at the negotiating table.

-

Long-Term Redefinition: Ultimately, neither the ruling nor the anti-subsidy duties will redefine the market. That role belongs to CBAM and the rise of green trade barriers. This shift will irreversibly push the global market towards fragmentation and fundamentally rewrite the asset valuation standard for stainless steel—in the future, energy structure and carbon efficiency will matter more than sheer production capacity.

—Written by Bruce Chew (bruce.chew@metal.com)

![[SMM Stainless Steel Daily Review] Funds Drive Up SS Futures, Strengthening the Market; Stainless Steel Spot Market Trading Sluggish](https://imgqn.smm.cn/usercenter/SduBz20251217171716.jpg)

![[SMM Stainless Steel Daily Review] SS Futures Bottomed Out, Stainless Steel Market Inquiry Activity Improved](https://imgqn.smm.cn/usercenter/LSkpO20251217171720.jpg)

![Stainless Steel Costs and Prices Pull Back Synchronously, Steel Mill Profits Remain Basically Stable [SMM Analysis]](https://imgqn.smm.cn/usercenter/SEwWP20251217171716.jpg)