I. Rincian Pasar: Kontraksi Produksi Mencerminkan Permintaan Yang Lemah

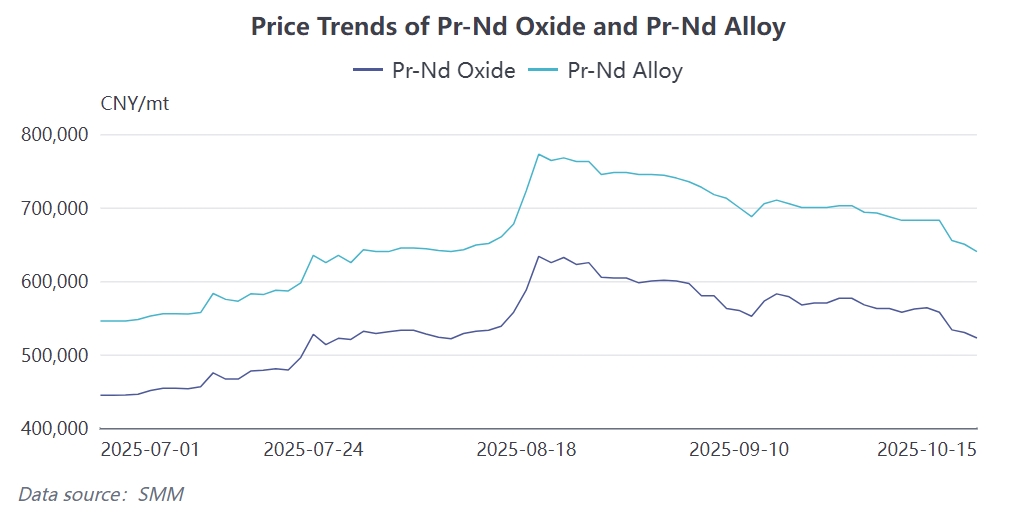

Berdasarkan survei SMM terbaru, produksi bahan magnet NdFeB Cina pada September 2025 sebesar 29,106 ton, turun 1.66% secara bulanan, dengan tingkat operasi industri keseluruhan pada 68.1%, turun 4.14 poin persentase secara bulanan. Yang lebih kritis, produksi Oktober diperkirakan turun lebih lanjut menjadi 27,648 ton, turun sekitar 5% secara bulanan, yang mencerminkan beberapa tekanan yang sedang dihadapi oleh industri bahan magnet. Berdasarkan hal ini, harga pasar NdFeB pada Oktober diperkirakan turun sekitar 3.4% secara bulanan dibandingkan dengan September, dengan harga rata-rata grade utama 52UH diperkirakan sekitar 445 yuan/kg, sedangkan 48SH berada di sekitar 300 yuan/kg. Dari sudut pandang biaya-plus, harga transaksi nyata saat ini berkorespondensi dengan harga aloy Pr-Nd sekitar 650,000 yuan/ton, sedangkan kuotasi pesanan yang baru saja ditandatangani pada minggu ini berkorespondensi dengan tingkat 630,000 yuan/ton.

Yang penting untuk dicatat, konsentrasi industri semakin mencepat. Bagian produksi perusahaan kelas atas naik 2.76% secara bulanan menjadi 73.5%, sedangkan bagian perusahaan kelas menengah turun 1.8% menjadi 21.8%, dan bagian perusahaan kelas bawah turun 1.1% menjadi 4.6%. Perubahan struktural ini menunjukkan bahwa, dalam latar belakang permintaan pasar yang lemah, perusahaan kelas atas dengan keuntungan skala dan hambatan teknologi menunjukkan ketahanan risiko yang lebih kuat.

II. Analisis Mendalam Sisi Permintaan: Divergensi Struktural Yang Signifikan

2.1 Kendaraan Listrik: Pertumbuhan Melambat Tetap Tahan

Analisis kinerja permintaan: Produksi KL mencapai 1.617 juta unit pada September, naik 16.33% secara bulanan, tetapi laju pertumbuhan diperkirakan melambat secara signifikan pada Oktober, dengan total produksi diperkirakan sekitar 1.665 juta unit. Meskipun KL mungkin mengalami penimbunan stok secara bertahap pada November dan Desember akibat dampak kebijakan penurunan subsidi yang dimulai pada 2026, efek nyatanya masih belum pasti meninggat lemahnya pasar konsumen akhir.

Penilaian trend jangka panjang: Industri KL telah masuk tahap perkembangan besar-besaran yang cepat dan besar. Laju pertumbuhan tahunan KL diproyeksikan sebesar 20%-25% pada 2025, sedikit lebih rendah daripada 34.75% pada 2024, tetapi masih mempertahankan tingkat yang cukup tinggi.Permintaan baja magnet untuk kendaraan listrik baru berkisar antara 2,7 hingga 7,0 kg per kendaraan。 Konsumsi kumulatif magnet permanen NdFeB dari Januari hingga Agustus 2025 mencapai 40,800 ton, memperkuat posisi kendaraan listrik baru sebagai area aplikasi terbesar untuk bahan magnet。

Karakteristik struktural: Permintaan menunjukkan divergensi struktural yang signifikan。 Area aplikasi tradisional, seperti peralatan rumah tangga termasuk AC, telah memasuki musim sepi produksi setelah musim panas。 Sektor elektronik 3C menghadapi permintaan jenuh karena kurangnya stimulasi dari model baru, menyebabkan pengurangan pesanan untuk bahan magnet kelas rendah dan menengah。 Sebaliknya, permintaan di area aplikasi baru tetap kuat。 Didorong oleh program domestik untuk pemutakhiran peralatan skala besar dan perdagangan barang konsumen, permintaan untuk NdFeB kinerja tinggi di sektor kendaraan listrik baru terus tumbuh stabil。

2。2 Sektor Tenaga Angin: Dampak Signifikan dari Faktor Musiman

Penurunan instalasi: Setelah reformasi pasar listrik pada Mei 2025, lonjakan instalasi sebagian besar telah menyelesaikan instalasi tahun ini。 Pada Oktober, saat wilayah instalasi tenaga angin utama secara bertahap memasuki musim dingin, operasi luar ruang menjadi lebih menantang, menyebabkan penurunan volume instalasi yang nyata。 Selain itu, dibatasi oleh fluktuasi signifikan harga logam tanah jarang, tingkat penetrasi turbin direct-drive telah menurun, memberikan dukungan lebih sedikit untuk produksi magnet permanen NdFeB。

2。3 Sektor Aplikasi Tradisional: Menghadapi Tekanan Umum

Sektor AC: Memasuki musim sepi tradisional di Q4, produksi terus melemah。 Data ChinaIOL menunjukkan bahwa pada September 2025, jadwal produksi penjualan domestik untuk AC rumah tangga adalah 5,72 juta unit, turun 6,3% YoY; pada Oktober, 4,815 juta unit, turun 23,4% YoY; dan pada November, 5,55 juta unit, turun 17,6% YoY。

Sektor Elevator: Terpengaruh oleh penurunan berkelanjutan di real estat, properti komersial terus menurun, dengan aplikasi terbatas di Q4。 Meskipun kebijakan yang memungkinkan penarikan dana prov perumahan untuk menambah elevator ke gedung residensial yang ada telah diperkenalkan di tempat-tempat seperti Tianjin, dorongan permintaan secara keseluruhan terbatas。

Pasar Ponsel: Pasar domestik mendekati saturasi, kurangnya momentum pertumbuhan。Meskipun seri Xiaomi 17 mencetak rekor penjualan, pasar secara keseluruhan kekurangan model baru yang revolusioner untuk merangsang produksi, yang cenderung menuju kejenuhan.

Robot Industri: Pada kuartal keempat, sektor ini tetap stabil pada dasarnya, dengan indeks industri rata-rata dan potensi pertumbuhan terbatas.Namun, lonjakan permintaan bahan magnetik BH tinggi di sektor seperti robot industri dan robot humanoid sebagian mengimbangi penurunan di area tradisional.

2.4 Pasar Ekspor: Kendala Signifikan dari Regulasi Kebijakan

Dampak Pengendalian Ekspor: Karena penguatan pengendalian ekspor oleh Kementerian Perdagangan, perusahaan bahan magnetik utama menjadi lebih hati-hati terhadap ekspor pada Oktober.Tanpa panduan jelas lebih lanjut, mereka mempertahankan sikap menunggu dan melihat, mengakibatkan pengurangan produksi bagi perusahaan dengan proporsi ekspor tinggi pada Oktober.

Perubahan Struktur Ekspor: Kebijakan saat ini yang mewajibkan deklarasi untuk magnet NdFeB telah memusatkan lisensi ekspor di tangan perusahaan tingkat atas, menyulitkan perusahaan menengah dan kecil untuk mendapatkan lisensi, mengintensifkan polarisasi industri.Kebijakan pengendalian ekspor menyoroti keunggulan perusahaan besar, karena mereka langsung berhadapan dengan perusahaan top Eropa, menikmati persetujuan ekspor yang lebih mudah dan sistem keterlacakan bahan magnetik yang lebih lengkap.

Prospek Ekspor Kuartal Keempat: Mempertimbangkan dinamika industri dan orientasi kebijakan, ekspor magnet tanah jarang pada kuartal keempat 2025 diperkirakan menunjukkan "volume total stabil namun diferensiasi struktural." Di satu sisi, pasar Eropa akan mengalami perlambatan pesanan baru karena liburan Natal dan penyelesaian kebutuhan penimbunan; di sisi lain, pasar Asia dan Amerika Utara mungkin mengambil alih sebagian permintaan yang bergeser, tetapi peningkatan keseluruhan akan terbatas.Berdasarkan ekspor kumulatif 34,000 ton dari Januari-Agustus dan perkiraan tahunan 49,000 ton, 15,000 ton perlu diekspor pada kuartal keempat, rata-rata sekitar 3,500 ton per bulan, penurunan signifikan dari puncak Agustus.

III. Analisis Singkat Sisi Pasokan: Regulasi Kebijakan Mengoptimalkan Lanskap Pasokan

Sisi pasokan, meskipun harga bahan baku tanah jarang sedikit menarik diri dari tertinggi, pasokan tetap ketat karena faktor seperti kuota penambangan, impor bijih yang berkurang, dan kebijakan perlindungan lingkungan.Sejak 2025, pengelolaan negara atas industri tanah jarang telah memasuki fase baru, dengan implementasi langkah-langkah regulasi terkait menandai optimisasi lebih lanjut dari lanskap pasokan sumber daya strategis ini.

Tren konsentrasi kapasitas di antara perusahaan-perusahaan tingkat atas telah membatasi fluktuasi drastis dalam produksi keseluruhan, dan industri sedang bertransisi dari lanskap kompetitif yang terfragmentasi ke struktur oligopoli. Tiongkok telah membentuk beberapa kluster industri material magnet utama di Zhejiang, Guangdong, Jiangxi, dan Tiongkok Utara. Di antara mereka, wilayah Zhejiang adalah pusat global untuk NdFeB, menjadi tuan rumah bagi banyak perusahaan tingkat atas.

IV. Prospek dan Prakiraan Permintaan Q4

4.1 Penilaian Tren Permintaan Jangka Pendek

Berdasarkan kondisi pasar saat ini, permintaan material magnet NdFeB pada Q4 diperkirakan menunjukkan karakteristik berikut:

Kendaraan Listrik: Pertumbuhan produksi pada Oktober diproyeksikan melambat menjadi sekitar 1.665 juta unit. Pemulihan ringan mungkin terjadi pada November-Desember karena dorongan untuk target tahunan di akhir tahun, tetapi pertumbuhan permintaan aktual akan terbatas karena kelemahan di pasar konsumen akhir.

Sektor Tradisional: Permintaan di area aplikasi tradisional seperti AC dan lift diperkirakan tetap di bawah tekanan. Q4 adalah musim sepi tradisional untuk sektor-sektor ini, dengan pengurangan pesanan yang nyata.

Pasar Ekspor: Dipengaruhi oleh liburan Natal, potensi pertumbuhan di Q4 terbatas. Ekspor keseluruhan tidak diharapkan signifikan, rata-rata sekitar 3,500 ton per bulan.

Sektor Emerging: Permintaan di area emerging seperti robot industri dan robot humanoid relatif stabil. Namun, potensi pertumbuhan dibatasi oleh lingkungan ekonomi keseluruhan.

4.2 Tren Pengembangan Permintaan Jangka Menengah dan Panjang

Dari perspektif global, industri material magnet tanah jarang Tiongkok telah membentuk sistem rantai industri yang lengkap. Tiongkok tidak hanya mempertahankan posisi terdepan dalam cadangan tanah jarang tetapi juga mengendalikan mayoritas produksi tambang tanah jarang global dan kapasitas material magnet NdFeB.

Dalam jangka panjang, perkembangan pesat industri seperti kendaraan listrik, tenaga angin, dan robotika akan terus mendorong pertumbuhan permintaan tanah jarang.Kesenjangan pasokan-permintaan NdFeB global kemungkinan akan bertahan dan berpotensi melebar dalam jangka panjang. Perusahaan-perusahaan tingkat atas yang memiliki sumber daya, teknologi, dan hambatan pelanggan akan memegang keunggulan kompetitif, dan tren menuju peningkatan konsentrasi industri tidak dapat dihindarkan.

![[Pengumuman SMM] Pengumuman tentang Revisi Metode Kuotasi Harga Bijih Itrium-Sedang, Kaya Europium SMM](https://imgqn.smm.cn/usercenter/rqOXm20251217171744.jpeg)