[SMM Analysis] Weekly Review of the Global Steel Market, Issue 5

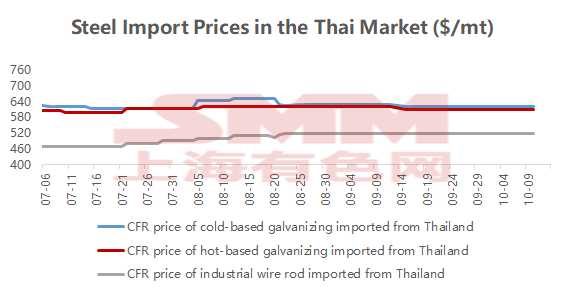

On a WoW basis from the Friday before the holiday to the Friday after the holiday, Chinese steel export prices fell by $4-5/mt, primarily due to significant declines in HRC prices, while medium-thickness plates, cold-rolled products, and silicon steel remained largely stable. In the Thai market, prices for mainstream resource varieties also remained stable, with CFR Thailand transaction prices for galvanizing at $610-620/mt and wire rod at $510-520/mt. This was mainly because during the double holiday, Chinese traders generally showed low enthusiasm for market transactions of export resources. Meanwhile, according to a recent SMM survey, some steel mills have raised their galvanizing prices for October, with export quotes increasing by $5-10, while wire rod prices are expected to decline. However, considering the recent continuous decline in Chinese prices and the uncertain trading environment, most downstream enterprises in Thailand remain on the sidelines, making it difficult for steel mills to raise prices for sales. Therefore, prices are expected to remain weak and stable, with actual transaction prices still expected to decline.

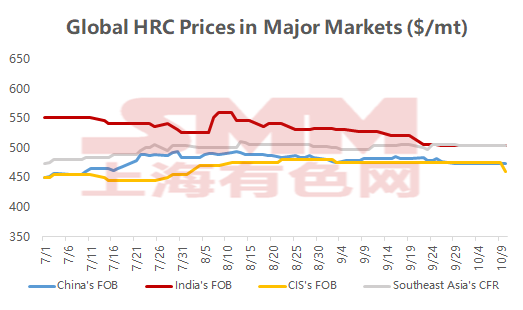

In major global markets, steel prices fell by 2-15 yuan/mt on a WoW basis from the Friday before the holiday to the Friday after the holiday. Chinese export prices were primarily affected by tariff barriers, leading to a decline in market sentiment and subsequently weaker steel prices. The most significant declines were seen in export prices from the Commonwealth of Independent States (CIS), with the Russian market being particularly representative. The main reason for the price drop was a decline in demand from traditional sales markets, such as China and Turkey, especially in the Chinese market where most transactions were suspended due to the holiday. As a result, Russian suppliers were forced to lower prices to fulfill November orders while actively exploring other regions, such as India. However, the acceptance of quotes in the Indian market was generally low, resulting in overall lower prices. In the European market, the implementation of the Carbon Border Adjustment Mechanism (CBAM) and the upcoming reduction in import quotas are expected to reshape the trade landscape between buyers and domestic and overseas suppliers. However, due to the lack of clarity regarding new market rules, uncertainty continues to affect market sentiment, coupled with weak downstream demand, leading to a continued weakening of transaction prices. Looking ahead, as post-holiday trade activities in China return to normal, CIS export prices are expected to improve. However, due to increased overseas uncertainties, Chinese prices are likely to remain in the doldrums. Most downstream customers in Southeast Asia currently exhibit a wait-and-see sentiment, resulting in prices holding steady in the doldrums, with a risk of slight declines in the near term.

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![[SMM Daily Chromium Review] Futures Rose While the Spot Market Remained Temporarily Stable, with Limited Adjustment in the Ferrochrome Market](https://imgqn.smm.cn/usercenter/rBCZR20251217171716.jpg)

![[SMM Iron & Steel] Hoa Phat Boosts Green Energy at Dung Quat Steel Complex](https://imgqn.smm.cn/usercenter/LSkpO20251217171720.jpg)