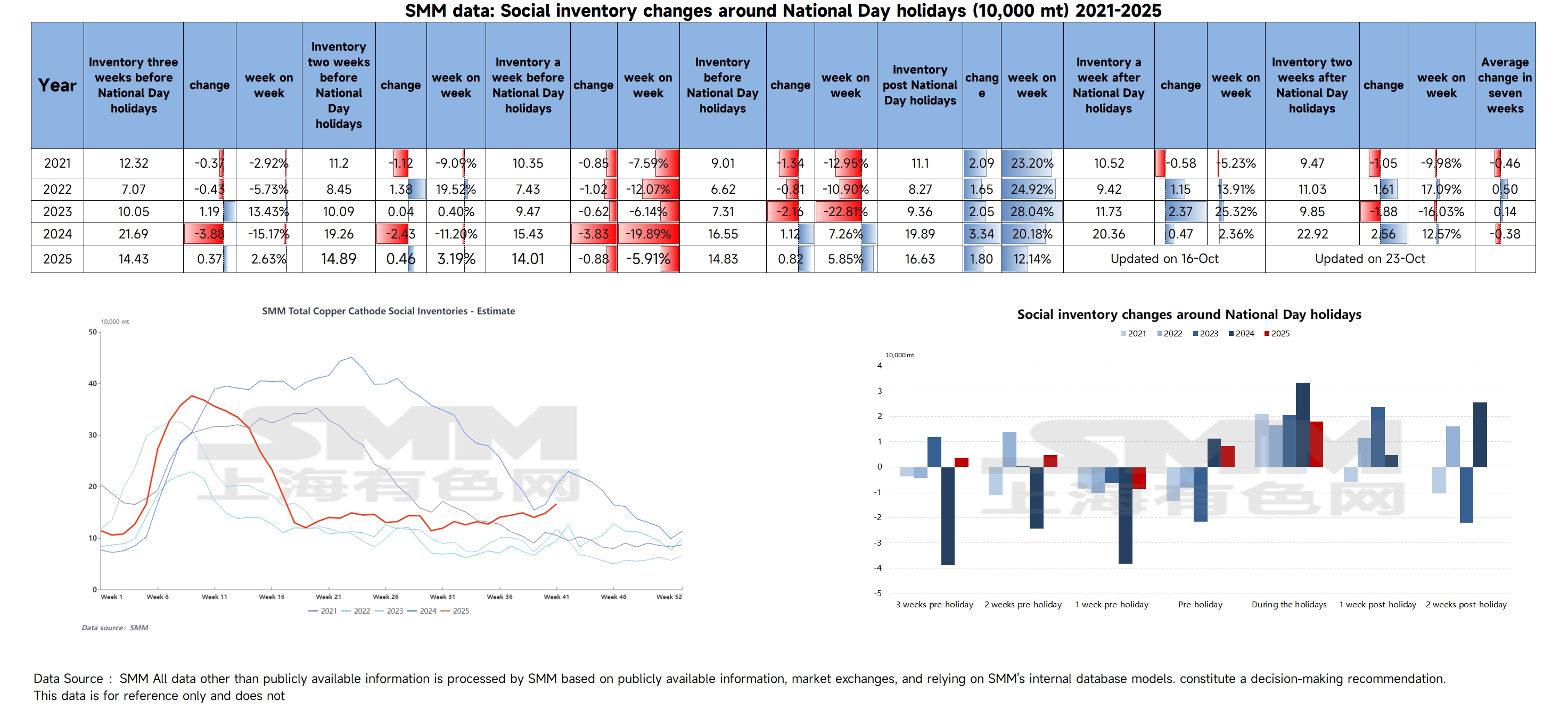

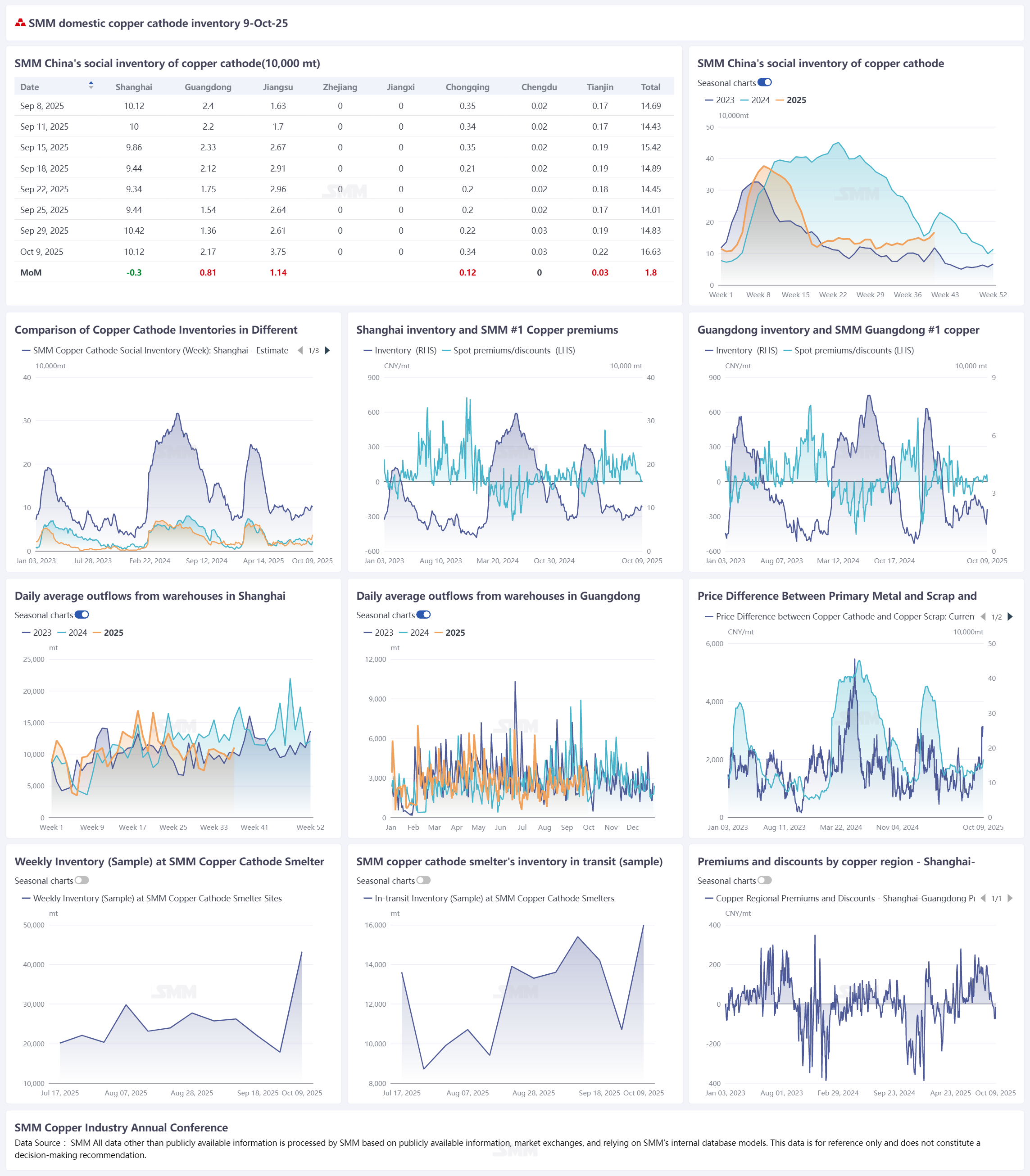

Following the holiday, as of October 9, SMM copper inventories in mainstream regions nationwide increased by 18,000 mt to 166,300 mt compared to September 29, and rose by 26,200 mt compared to September 25. Total inventories decreased by 37,300 mt YoY from 203,600 mt. Overall, the post-holiday inventory buildup was lower than market expectations and declined compared to the same period last year.

By region, inventory performance in major markets showed significant divergence:

Shanghai is the only major region with a decline in inventory:Copper cathode inventories decreased by 3,000 mt compared to September 29. During the holiday, overall cargo pick-up remained normal, and imported shipments did not arrive in concentrated volumes. Additionally, most of the supplies from smelters in and around east China were delivered to warehouses in Jiangsu. Coupled with smelters considering maintenance and export opportunities, fewer shipments were sent to Shanghai, ultimately driving destocking of copper cathodes in the region.

Supply-Demand Weakness in Guangdong Leads to Narrower Inventory Buildup:Inventory increased by 8,100 mt from September 29 to 21,700 mt. From both the supply and demand sides, demand performance was weak. During the holiday, downstream users in Guangdong were affected by both the off-season and high copper prices, leading most downstream factories to extend their National Day holiday, resulting in a significant YoY decline in pickup volume. On the supply side, some smelters implemented temporary production cuts due to equipment maintenance and raw material supply issues, while a small number of smelters diverted domestic supply for export, significantly reducing the volume of domestic copper cathode flowing into Guangdong's social inventory. Ultimately, this led to a lower inventory buildup compared to the same period last year.

The inventory in Jiangsu exhibited a "routine inventory buildup" trend:Inventories increased by 11,400 mt, bringing the total inventory level to 37,500 mt, in line with the seasonal pattern observed after the holiday. This was primarily driven by the continuous arrival of domestically produced copper and weakening downstream consumption, with the extent of inventory buildup comparable to the same period last year.

Social inventory still faces pressure from inventory buildup, and the supply-demand pattern continues to be dominated by high copper prices:Looking ahead, imported supplies are expected to continue arriving, but the COMEX-LME price spread shows signs of further widening, which may lead to an increase in shipments to the US. Close attention should be paid to the actual arrival of imported goods in the later period. Domestically, as year-end approaches, smelters are gradually entering maintenance cycles, and the volume of domestic supply arrivals is expected to decrease. However, with the delivery date of the 2510 contract nearing and against the backdrop of spot discounts, delivery-related inflows are anticipated to rise. On the demand side, high copper prices after the holiday have resulted in poor connectivity of new orders downstream, with just-in-time procurement being the dominant approach. Inventory is expected to continue accumulating.

![Early-Month Purchasing and Stockpiling Failed to Offset the Impact of Imports, SHFE Copper Spot Premiums Remained Under Pressure [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/OsOmo20251217171709.jpg)

![Market Activity Increased After the Contract Rollover, Spot Premiums Continued to Rise [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/fEiiq20251217171711.jpg)