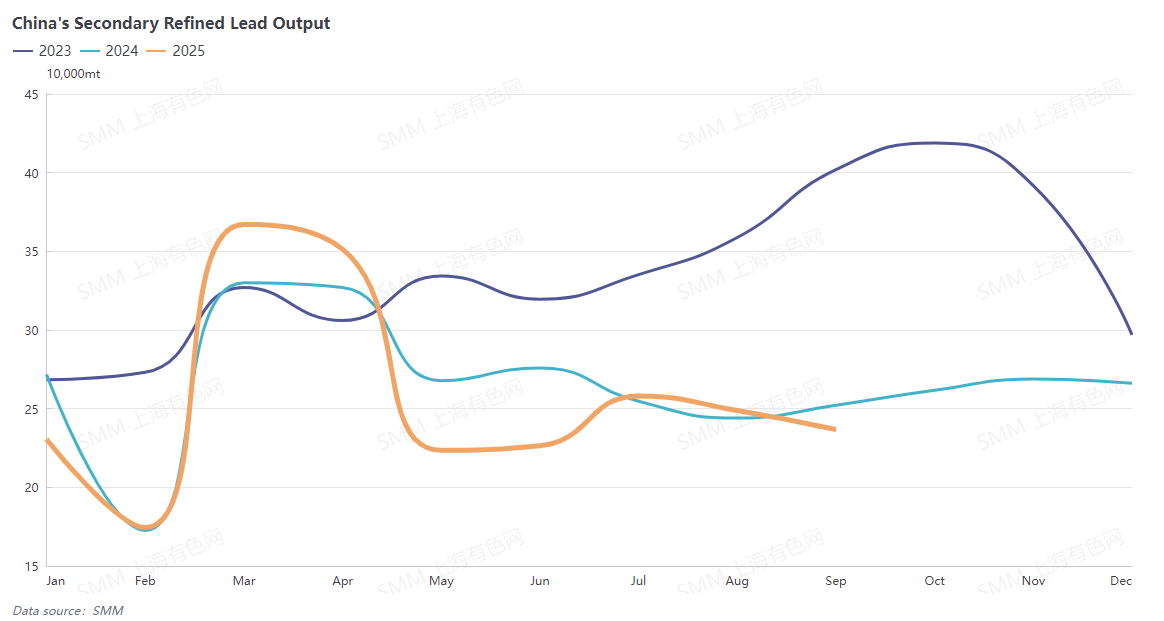

China's secondary lead production in September 2025 showed a declining trend, decreasing 0.99% MoM but increasing 5.52% YoY; secondary refined lead production fell 4.85% MoM and dropped 6.11% YoY.

At the beginning of September, the SCO summit combined with military parade activities led to a slowdown in operations for some recyclers in north China, causing regional tightening in scrap battery supply. At the same time, due to lack of confidence in end-use consumption and a bearish outlook on lead prices, smelters in Hebei cut production, while a large smelter in Inner Mongolia entered a shutdown for maintenance. In east China, individual smelters halted production from early September due to equipment maintenance needs. In south-west China, a large smelter completed equipment maintenance and resumed production in early September. In late September, consumption of lead-acid batteries for two-wheel bicycles improved, and lead prices fluctuated upward, prompting some secondary lead smelters in east China to raise output. Overall, the increased production from enterprises resuming or raising output offset the decline from those cutting or halting production, resulting in a smaller-than-expected drop in secondary refined lead production for September.

The National Day & Mid-Autumn Festival holidays fall in early October, with most secondary lead smelters scheduling production resumption plans for mid-October. Full production output is expected only by late October after oven drying is completed, contributing weakly to October's production. Additionally, as some enterprises remain cautious about improved consumption in downstream lead-acid batteries, the actual pace of production resumption is closely linked to lead price trends, scrap battery supply, and smelting profits.