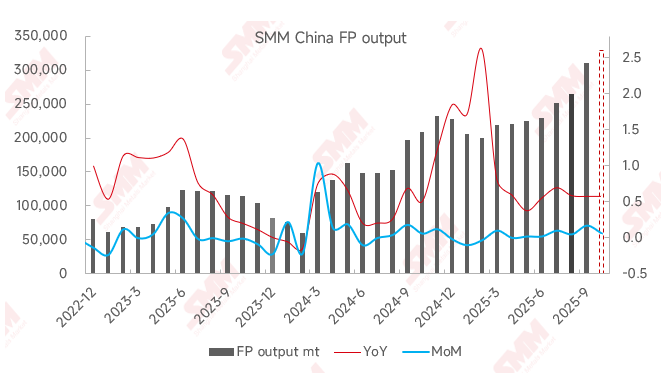

In September, the domestic iron phosphate market exhibited an active trend of "increases in both volume and price," with particularly outstanding production data. According to statistics, iron phosphate production rose significantly by 17% MoM and was up 58% YoY, successfully surpassing the 300,000 mt monthly production threshold, achieving a notable supply-side increase compared to August.

Regarding growth drivers, the core logic revolves around the strong transmission of downstream demand. On one hand, a surge in orders for integrated leading LFP enterprises directly boosted demand for their self-produced iron phosphate. On the other hand, as the lithium battery market entered its traditional peak season in September, downstream demand was transmitted upward through the layers, not only driving synchronous growth in orders and production schedules for iron phosphate enterprises but also significantly increasing activity in the externally purchased iron phosphate market. Against this backdrop, the iron phosphate market achieved breakthroughs in both "self-production and external sales" in September. Some enterprises, responding to order growth, even activated previously idle production lines, leading to a significant increase in the overall industry operating rate and a further rise in the number of enterprises operating at full capacity.

Cost side, a divergent pattern of "one stable, one rising" emerged. In September, industrial-grade MAP prices remained low, providing relatively stable cost support for iron phosphate production. However, affected by tight supply, ferrous sulphate prices continued to rise, resulting in substantial cost pressure for iron phosphate enterprises in sourcing iron.

Looking ahead to October, with further increases in market activity and continuous improvement in the supply-demand relationship, iron phosphate prices are expected to see a slight increase, and industry enterprises are generally optimistic about the October market. Production-wise, iron phosphate output in October is projected to increase by 6% MoM, while the YoY growth rate is expected to remain high at 58%, suggesting a continuation of strong industry prosperity.