- In January-August 2025, China's exports of sheets & plates decreased by 1% YoY.

On September 8, data from the General Administration of Customs showed that China exported 9.51 million mt of steel in August 2025, down 326,000 mt MoM, a decrease of 3.3% MoM. Cumulative steel exports from January to August totaled 77.49 million mt, up 10.0% YoY.

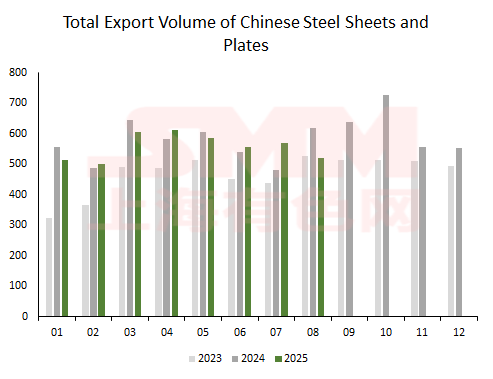

Among these, China exported 5.2037 million mt of steel sheets & plates in August 2025, down 501,000 mt MoM, a decrease of 8.8% MoM. Cumulative exports of sheets & plates from January to August reached 44.6326 million mt, down 1.2% YoY.

In terms of proportion, China's exports of steel sheets & plates accounted for approximately 52% of total steel exports (including steel billet) from January to August 2025, a decrease of about 10 percentage points compared to the same period in 2024. Meanwhile, exports of rebar, coiled rebar, and steel billet accounted for approximately 14% of total steel exports (including steel billet) in the first eight months of this year, an increase of about 11 percentage points compared to the same period in 2024.

It is not difficult to notice that the product mix of steel exports shifted in 2025, with both the export volume and share of long products and steel billet increasing. The total exports of steel billet in the first eight months of 2025 reached 9.2426 million mt, an increase of 6.8813 million mt compared with the same period in 2024, up 291%. The total exports of rebar in the first eight months of 2025 reached 6.064 million mt, an increase of 1.9857 million mt compared with the same period in 2024, up 49%. The total exports of coiled rebar in the first eight months of 2025 reached 6.0248 million mt, an increase of 2.17 million mt compared with the same period in 2024, up 56%.

In contrast, the total export volume and share of products such as HRC and cold-rolled products pulled back. The total exports of HRC in the first eight months of 2025 reached 16.4016 million mt, a decrease of 3.0882 million mt compared with the same period in 2024, down 16%. The total exports of cold-rolled products in the first eight months of 2025 reached 3.3604 million mt, a decrease of 285,000 mt compared with the same period in 2024, down 8%. The main reason behind this is primarily related to the continued intensification of overseas anti-dumping measures against China's cold-rolled and HRC in 2025.

- From the perspective of sheet & plate export structure, coated & plated products are actively filling the gap left by hot-rolled exports.

Due to the ongoing rise in impact from overseas anti-dumping measures, China's hot-rolled exports decreased significantly this year. Meanwhile, the export volume and proportion of coated & plated products increased markedly, making them the top category in China's steel exports. From January to August 2025, the total export volume of coated & plated sheets & strips reached 20.0904 million mt, an increase of 2.8938 million mt compared to the same period in 2024, representing a 17% growth. In terms of flow direction, from January to August this year, exports to the top 20 destination countries accounted for 63% of the total coated & plated exports, with the top-ranked countries primarily located in Southeast Asia, South America, the Middle East, East Asia, and Europe.

Reportedly, the primary reasons for this stem from the price competitiveness and product technological advantages of China's coated & plated sheets & strips. However, the substantial increase in coated & plated exports also sows the seeds for potential "anti-dumping" risks in more overseas markets targeting these products from China...

![[SMM Daily Chromium Review] Futures Rose While the Spot Market Remained Temporarily Stable, with Limited Adjustment in the Ferrochrome Market](https://imgqn.smm.cn/usercenter/rBCZR20251217171716.jpg)

![[SMM Iron & Steel] Hoa Phat Boosts Green Energy at Dung Quat Steel Complex](https://imgqn.smm.cn/usercenter/LSkpO20251217171720.jpg)