[SMM Analysis] Global Steel Market Weekly Review, Issue 4

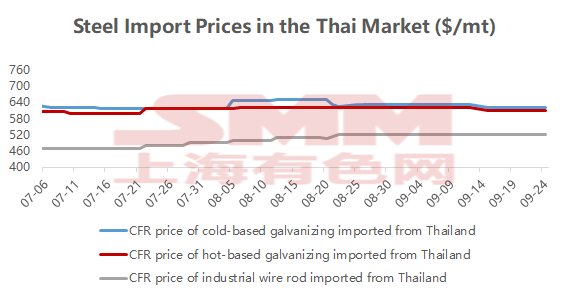

Last week, China's steel export prices fluctuated rangebound by $1-3/mt. By sheet & plate variety, HRC prices edged down $1-2/mt, while medium-thickness plates, cold-rolled products, and silicon steel remained in the doldrums. In the Thai market, mainstream product prices held steady mid-week, with galvanizing CFR Thailand traded at $610-620/mt and wire rod CFR at $520-525/mt. According to local traders, supply of some galvanizing resources is somewhat tight, overall shipment sentiment is average, and mills refuse to budge on prices.

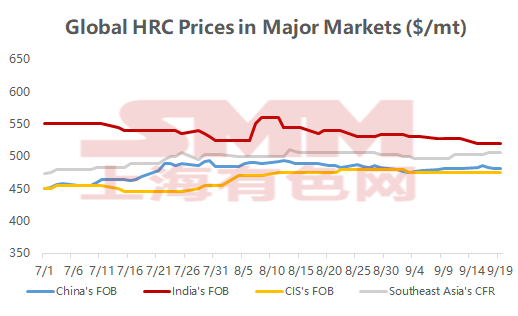

Globally, last week saw most steel market prices in the doldrums, with significant fluctuations observed in India and the EU. Affected by weak global demand and concerns over emerging policies, market sentiment for HRC exports in India weakened, putting prices under pressure, and transaction prices subsequently declined. In the EU, end-user purchasing demand remained sluggish. Although traders recently pushed for price increases due to CBAM and tariffs, these were not fully realized, leading to a correction in HRC prices, while some specialty steel prices saw increases. Looking ahead, with the National Day holiday approaching, uncertainties regarding the implementation of customs policies in October are increasing. Chinese export offers are expected to remain in the doldrums. The EU market still holds potential for price increases, with significant fluctuations anticipated around mid-October. In India, due to increased risks in exports to Europe, the focus has shifted to markets like the Middle East and Southeast Asia, potentially leading to further price cuts to capture market share.

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)