China's Magnesium Product Exports in August 2025: Double Growth Month-on-Month and Year-on-Year, but High Market Prices Suppress Demand

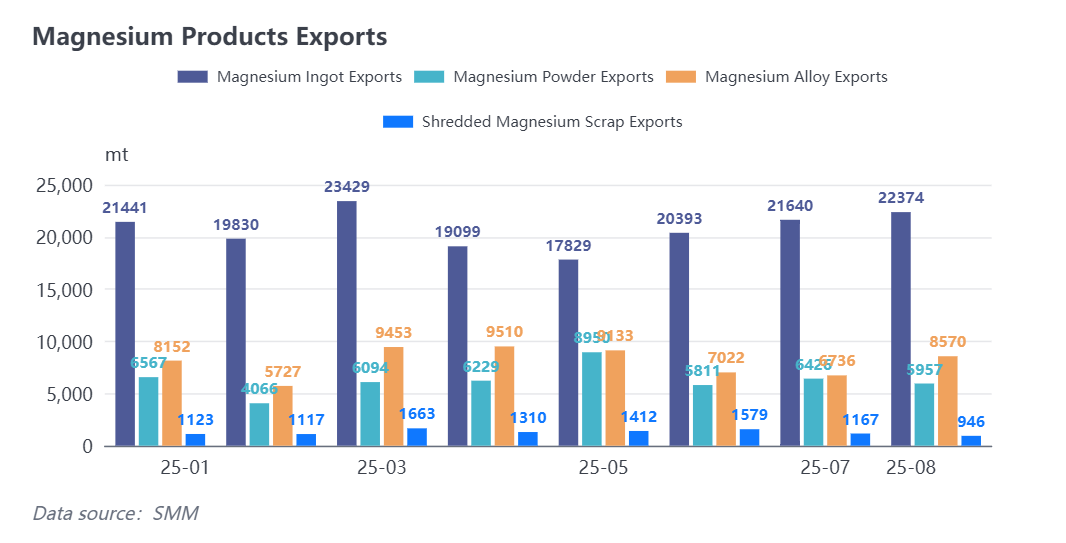

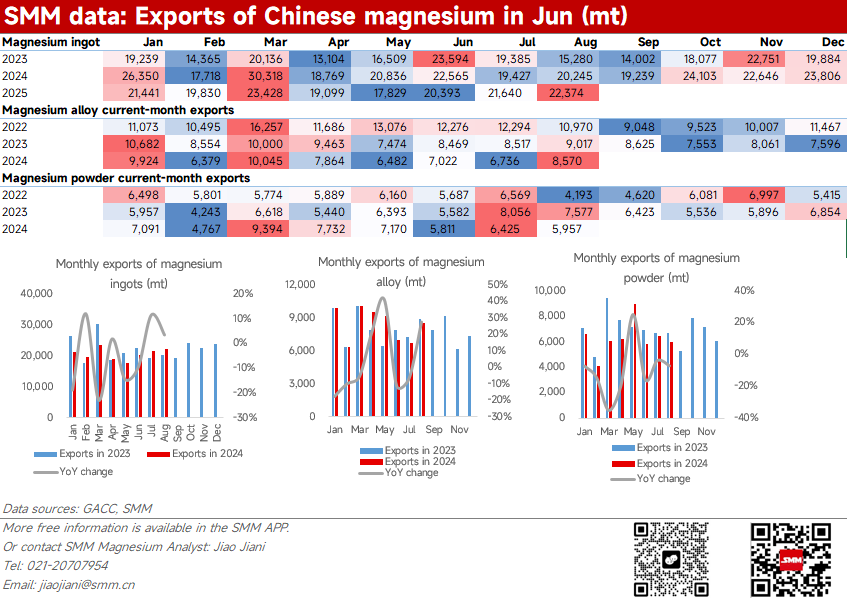

In August 2025, China's cumulative export volume of magnesium products reached 38,600 tons, an increase of 5.43% month-on-month and 4% year-on-year. The overall export performance for the month was bright, primarily driven by growth in exports of both magnesium ingots and magnesium alloys.

The main reasons for the strong export performance lie in the gradual execution of overseas orders received from late June to early July, reflecting that the scale of order releases in the first half of the year exceeded expectations. The situation of insufficient overseas demand at the beginning of the year was effectively compensated for later.

However, August exports did not reach the high point expected by the market. The main reasons include: firstly, the "anti-internal competition" policy introduced in late July pushed magnesium prices to remain high for a continuous month, increasing downstream purchasing wait-and-see sentiment; secondly, stricter supervision of export payments intensified the standoff between supply and demand, suppressing some actual demand, leading to more cautious new orders since July; thirdly, new orders from regions like Europe stalled after the summer holidays, resulting in an overall slowdown in demand.

Rise of North American Market and Recovery of European Demand Shape August Magnesium Exports; Significant Divergence in Product Trends

In August, magnesium ingot exports reached 22,400 tons, up 3.39% month-on-month, accounting for 58% of total magnesium product exports, making them the main driver for the month. However, their cumulative export volume for 2025 still decreased by 5.79% year-on-year, indicating that despite three consecutive months of month-on-month growth, the weak overseas demand trend this year has not yet been fully reversed. It is noteworthy that exports to the Netherlands saw a significant month-on-month increase of 33.71%, reaching 5,902 tons, showing positive signals of a gradual recovery in European market demand during the third quarter.

In August, magnesium powder exports were 8,850 tons, down 7.3% month-on-month, and the cumulative export volume for 2025 decreased by 11.19% year-on-year. Some magnesium plants reported that the export control policy effective from October 1st has already impacted orders for the fourth quarter. Coupled with persistently high magnesium prices in July and August, downstream purchasing sentiment remains cautious. Nevertheless, a certain number of overseas orders were still finalized in August, and their actual export impact is expected to be reflected in September's export data.

In August, magnesium alloy exports reached 8,570 tons, a significant increase of 27.23% month-on-month, but the cumulative export volume for 2025 still experienced a slight decrease of 0.72% year-on-year. Since the second half of the year, magnesium alloy exports have shown strong growth momentum, with overall order demand remaining high. Based on manufacturers' production schedules for September, which are largely fully booked, it further confirms a significant recovery in downstream demand. In terms of regional distribution, Canada became the largest destination for magnesium alloy exports this month, with a total of 2,248 tons, reflecting the gradual emergence of the North American market.

Inventory Accumulation and Slower Procurement in August Underpin Growth Expectations for September Exports

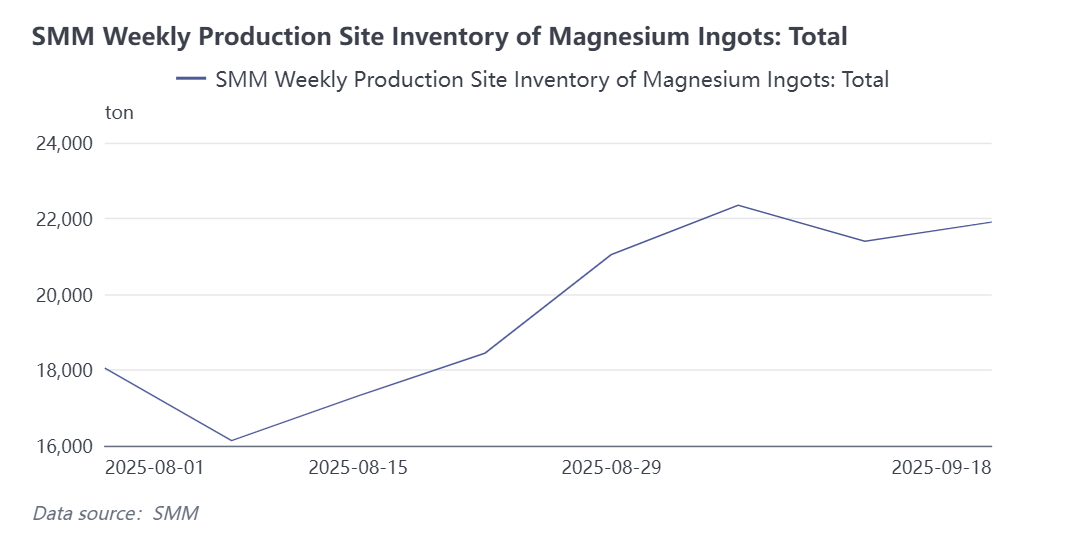

According to SMM survey data, magnesium ingot production in August was 80,511 tons, and magnesium plants began a phase of gradual inventory accumulation starting in August. This trend corresponds with the export performance in the same period, reflecting a weakening purchasing enthusiasm among traders in August. Part of the reason is that orders currently being shipped were already prepared for in early July. Looking at inventory levels in September, the market still shows a pattern of supply exceeding demand. However, with the gradual release of new orders in September and the push from the "rush to export" effect before the October export policy takes effect, it is expected that magnesium product export volume will achieve further growth in September.