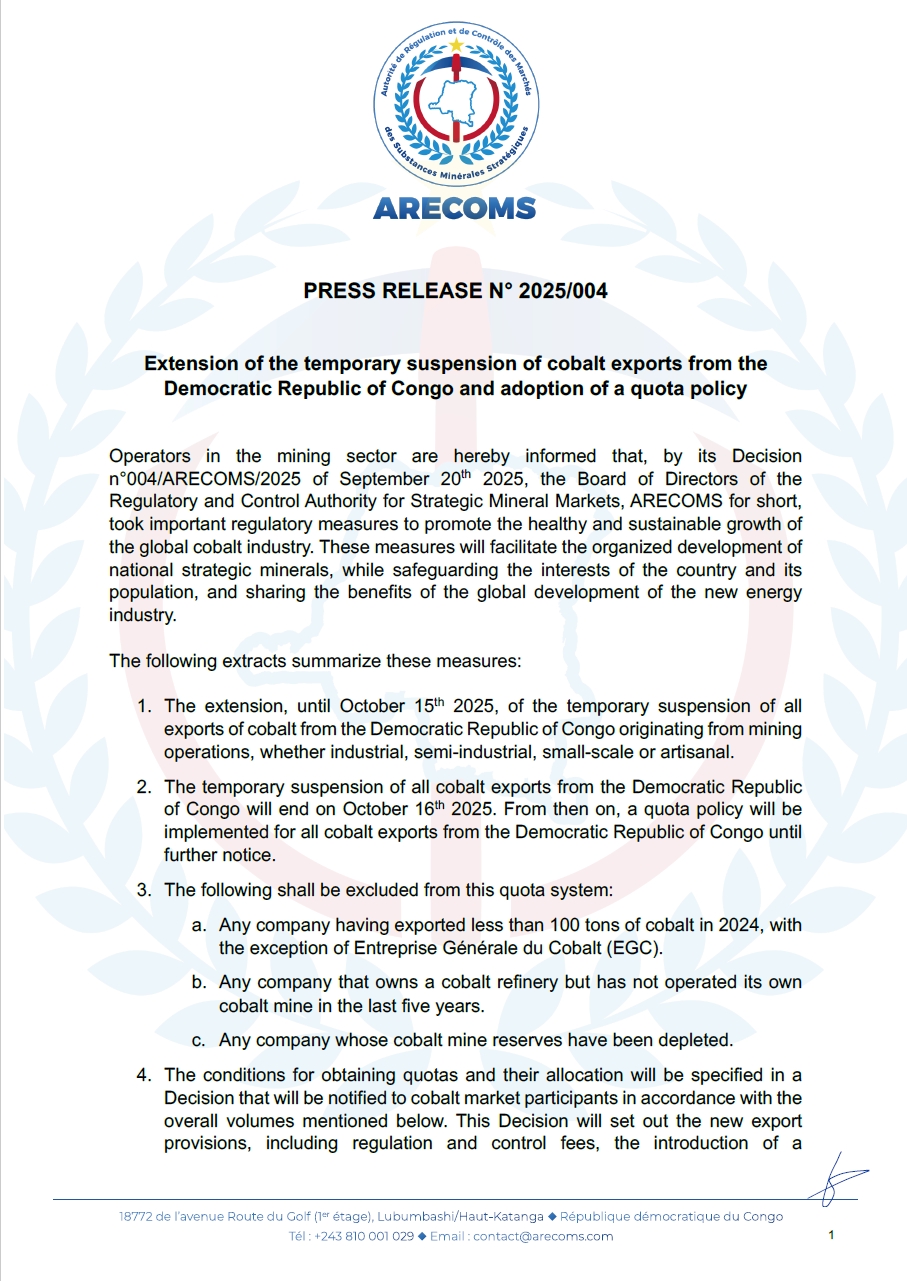

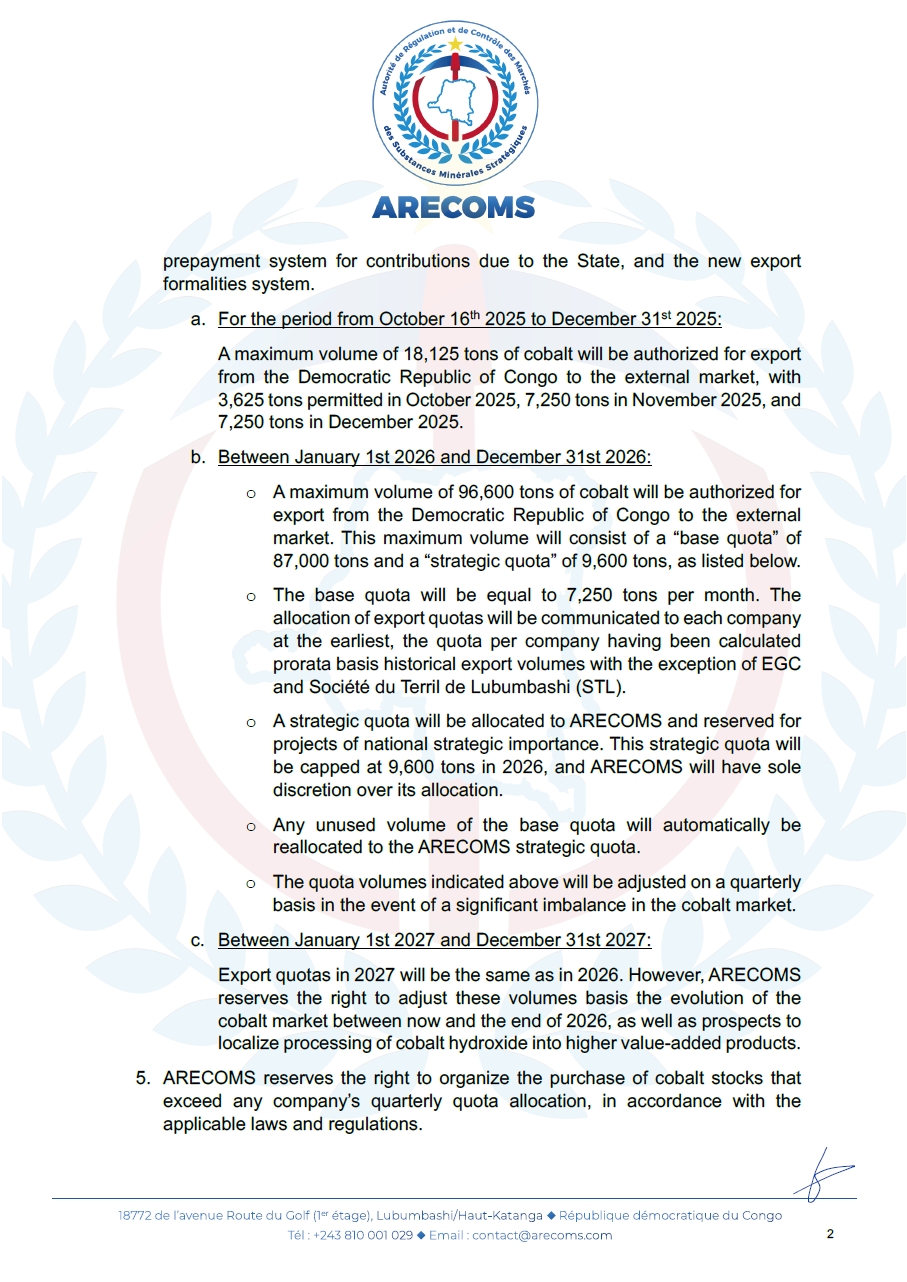

On the evening of September 21, 2025, the DRC announced the extension of the export ban, originally set to expire on September 21, until October 15, and declared that a quota policy would be implemented starting October 16. Below is the original document:

Market Conditions Prior to This Policy:

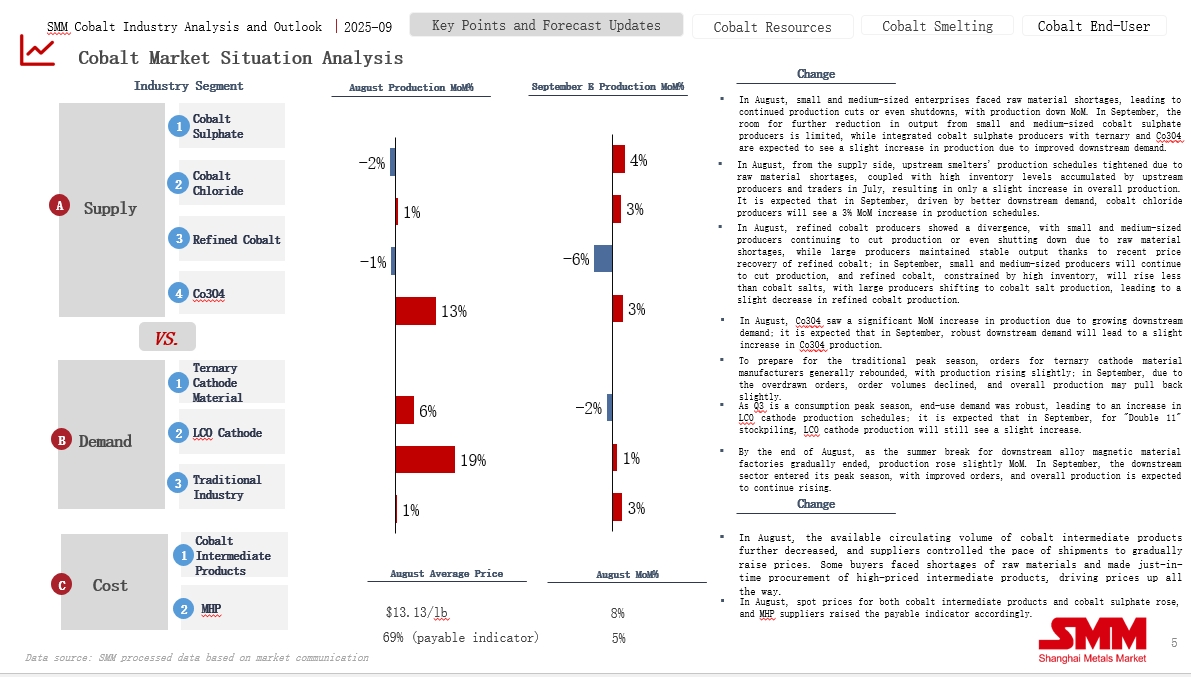

The chart below illustrates the cobalt market situation prior to the announcement of this round of policies. Overall, on the supply side, raw material imports continued to decrease, and smelters maintained tight production schedules amid constrained raw material inventory. Meanwhile, on the demand side, the market was in its peak season with increased demand, leading to a destocking trend across the entire cobalt market.

Market Expectations and Price Conditions Prior to This Round of Policy:

Before the official announcement of this policy, the market generally expected the DRC to extend the export ban, and all cobalt products were in a continuous rising state.

Last week, overseas cobalt intermediate product quotations continued to be raised, with transactions in the domestic market around $14.4/lb, and some enterprises reported possible transactions around $14.7/lb.

Cobalt sulphate spot prices continued to rise, with most smelters suspending quotations and raising their intended selling prices to above 60,000 yuan/t. However, downstream players remained relatively cautious, mainly consuming their own inventory, and market transactions were sluggish.

The cobalt chloride market performed strongly, with enterprise quotations maintained at 70,000-75,000 yuan/t, supported by strong cost-side factors, but downstream enterprises generally adopted a wait-and-see attitude. Co3O4 prices continued to rise, with the quotation range for high-voltage and high-doping Co3O4 at 225,000-230,000 yuan/t. Influenced by rising raw material cobalt chloride prices, cost-driven upward momentum significantly strengthened, and some downstream enterprises increased inventory reserves.

Ternary cathode precursor prices continued their upward trend, with nickel sulphate, cobalt sulphate, and manganese sulphate prices rising continuously, further driving up precursor costs, and producer quotations increased rapidly. Ternary cathode material prices continued to rise, lithium carbonate shifted to a slight increase, while cobalt sulphate and nickel sulphate maintained a sharp upward trend, significantly boosting ternary cathode material prices; cathode plant orders performed well but still faced considerable cost pressure.

LCO market prices rose slightly, with mainstream transaction prices for 4.45V/4.48V products above 235,000 yuan/t, and transaction prices for 4.50V and above models exceeding 240,000 yuan/t, mainly driven by the continuous rise in Co3O4 prices.

Impact of This Round of Policies:

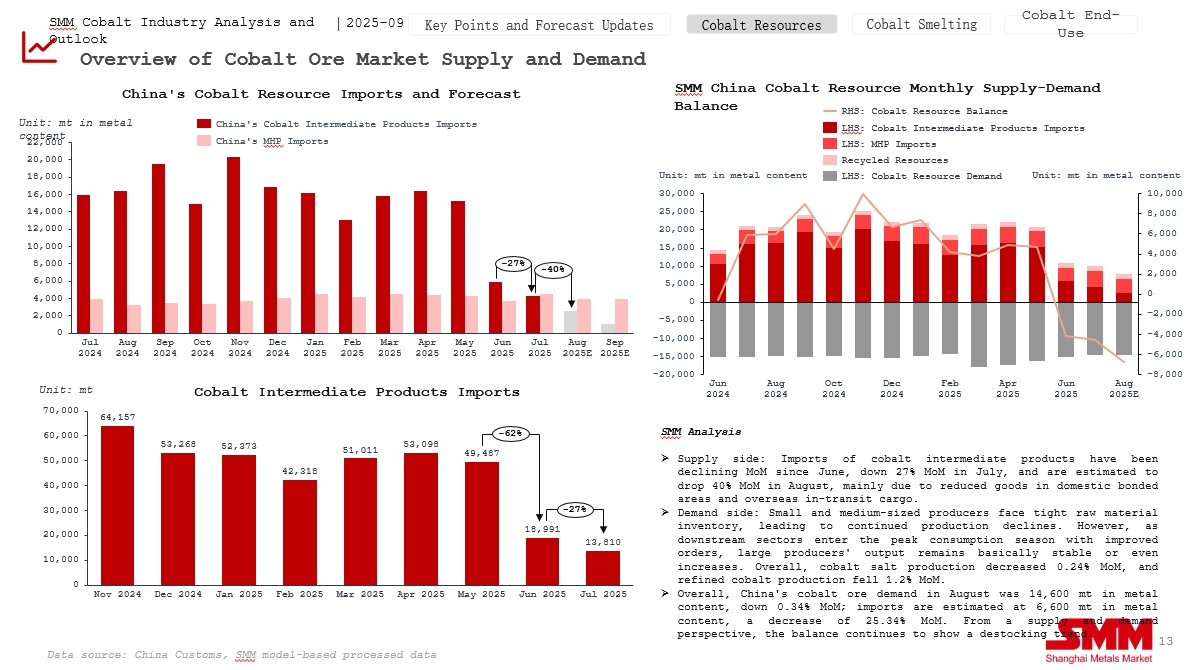

According to SMM model calculations, under the current policy, China's cobalt market will continue to be in a destocking state from 2025 to 2027. China's cobalt resource demand in 2025 is estimated to be around 170,000 to 180,000 mt . As of July, China imported approximately 87,000 mt of intermediate products. Considering the 2 to 3-month shipping period from the DRC to China, if the export ban is not lifted until October 16, the only intermediate products that can enter China this year will be the inventory in domestic bonded zones and overseas ports. The total import volume of intermediate products for the year is projected to be about 90,000 to 100,000 mt. Domestically, recycled cobalt production in 2025 is expected to be around 15,000 mt, and MHP imports are estimated at 50,000 mt. It is anticipated that China's cobalt resources will undergo destocking of 10,000 to 20,000 mt this year.

In 2026 and 2027, even assuming that downstream cobalt demand is suppressed due to high cobalt prices and remains at around 180,000 to 190,000 mt, and further assuming that MHP and recycled cobalt production increase due to high economic viability, with MHP imports reaching 70,000 to 80,000 mt and domestic recycled production at 20,000 mt, there will still be a demand for nearly 100,000 mt of cobalt intermediate products domestically. Considering that the DRC utilizes its entire strategic quota and slightly exceeds it to 100,000 mt, with 80% of this volume exported to China, China's cobalt resources will still face a gap of approximately 10,000 to 20,000 mt.