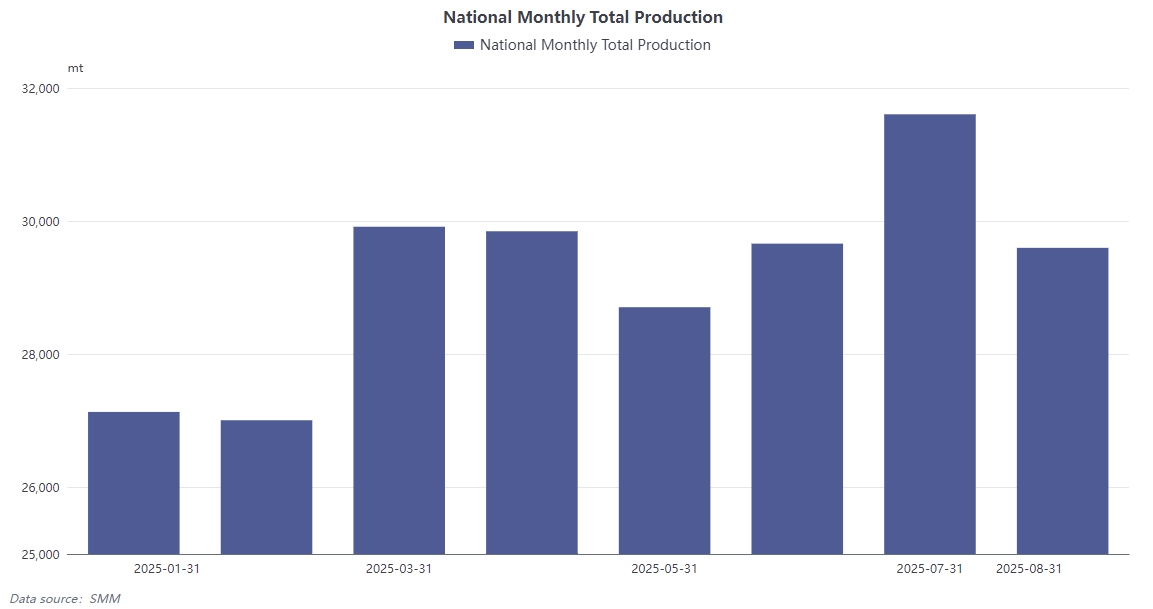

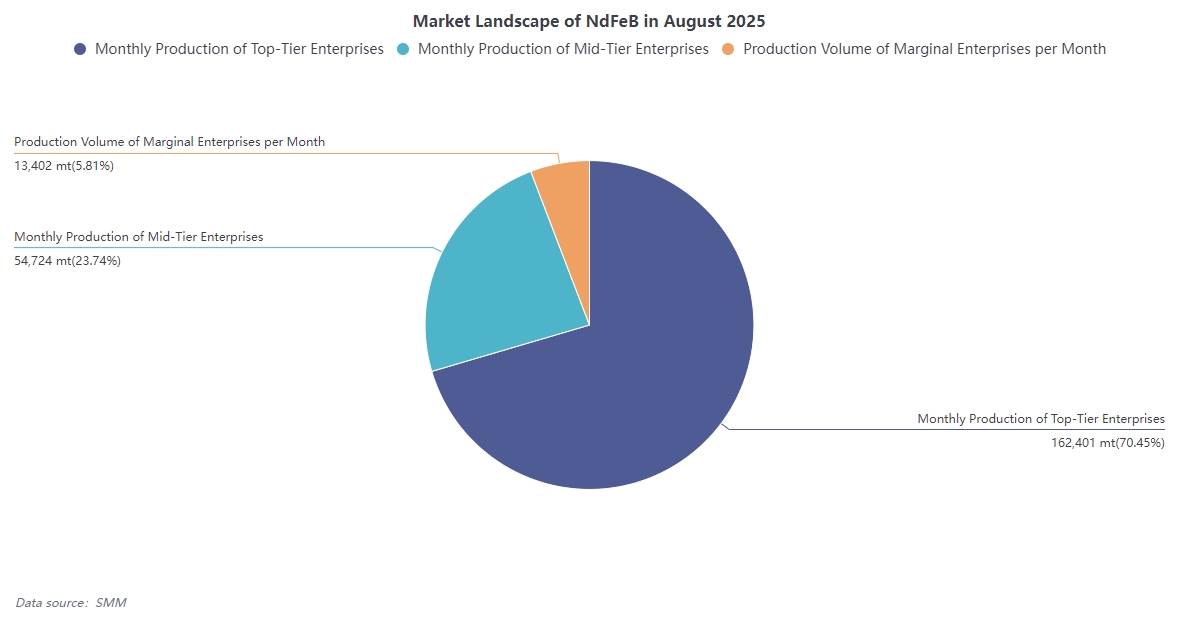

In August 2025, China's sintered NdFeB magnetic material industry showed a MoM decline in production but saw the consolidation of advantages among top-tier enterprises. According to SMM's frontline survey data, the national total production of sintered NdFeB reached 29,599 mt that month, down approximately 6.3% MoM. In terms of production structure, top-tier enterprises produced 20,904 mt, accounting for 70.45% of the total; mid-tier enterprises produced 6,997 mt, accounting for 23.74%; and small-tier enterprises accounted for only 5.81%. The industry exhibited a high degree of concentration, with top-tier enterprises dominating market share. Top-tier enterprises continue to hold a significant position in both production volume and technology, and a trend of orders increasingly shifting toward these enterprises is emerging, further reinforcing the industry's pattern of the strong growing stronger.

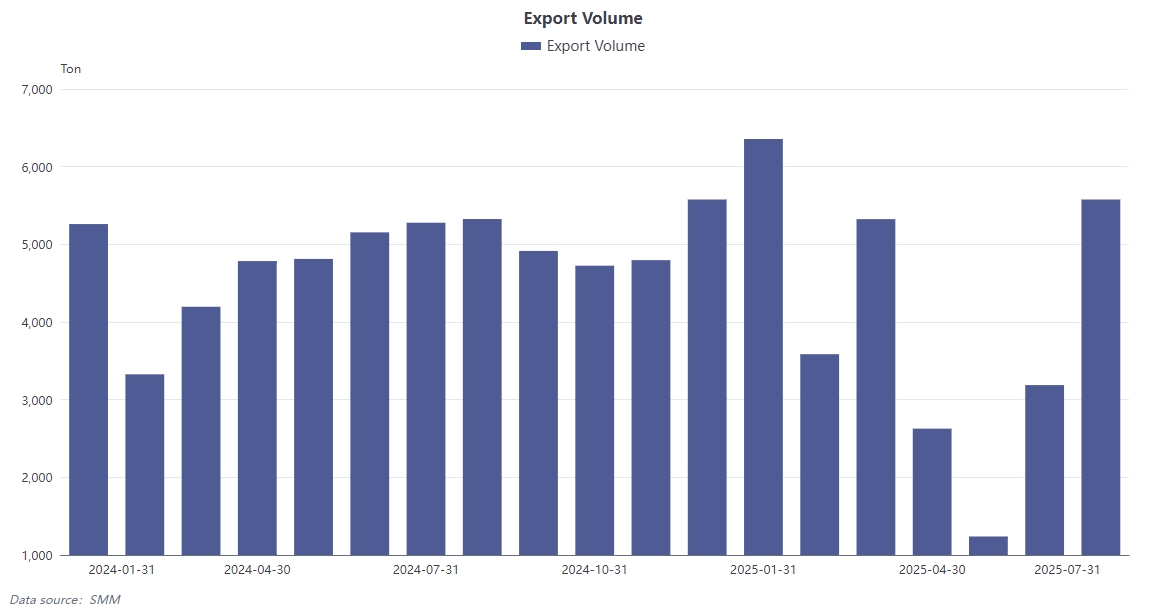

In terms of operating rate, the national average operating rate for sintered NdFeB plants in August 2025 was 69.24%, down 4.69% MoM. By enterprise size, the operating rate for top-tier enterprises was 67.34%, mid-tier enterprises 66.97%, and tail-end enterprises 62.13%, with overall operating rates trending downward, reflecting widespread short-term production pressure in the industry. On the export market, according to the General Administration of Customs, China exported 5,791.8 mt in August. Although magnetic material export data has not been officially released, based on past experience, magnetic material exports in August 2025 are expected to be at least 5,200 mt, flat MoM. From January to July 2025, total magnetic material exports were 27,890.6 mt, down 14% from 32,813.07 mt in the same period of 2024. This decline was mainly due to escalated China-US tensions after Trump took office in 2025, with the US imposing hefty tariffs and China implementing export controls, which suppressed export demand throughout H1.

The main reasons for the decline in magnetic material production in August can be attributed to the combined impact of multiple factors: significant pressure on the cost side, with prices of NdFeB raw materials such as Pr-Nd oxide and Pr-Nd alloy remaining high throughout July and August. Taking Pr-Nd alloy as an example, its monthly average price remained at 638,636 yuan, with consecutive sharp increases in between. This high cost led to a noticeable wait-and-see sentiment among end-users, with some non-urgent orders being temporarily postponed, and enterprises shifting to primarily consuming inventory. End-use demand entered the traditional off-season, with domestic new energy vehicle production and sales continuing to decline in August. The home appliance sector, represented by air conditioners, gradually reduced production as the summer period ended. The 3C electronics sector, lacking stimulus from new models, saw saturated production and relatively small increments. Meanwhile, industrial sectors such as wind power and industrial robots were affected by hot summer weather, which reduced factory operating rates and weakened support for NdFeB permanent magnet orders. Policy barriers in the export market intensified internal divisions. Although there was order demand from regions like Europe and the US, and exports were expected to remain at a relatively high level, the current policy requiring declaration for NdFeB magnetic materials has resulted in export licenses being concentrated in the hands of leading large enterprises. Small and medium-sized enterprises struggled to obtain licenses, leaving them uncompetitive in exports and ultimately leading to insufficient operating rates, exacerbating the overall decline in production.

High raw material costs were the primary factor suppressing production. As a key raw material for NdFeB magnetic materials, price fluctuations of Pr-Nd alloy directly affect the production costs and profit margins of magnetic material enterprises. The average high price of 638,636 yuan/mt throughout July-August far exceeded historical levels for the same period, and coupled with consecutive price surges during this time, it imposed significant cost pressure on downstream magnetic material enterprises. Faced with such high raw material prices, end-use application enterprises showed significantly reduced purchase willingness. Apart from essential orders, many customers chose to postpone procurement plans, prioritize digesting their own inventory, and wait for price adjustments. This wait-and-see sentiment propagated upstream along the industry chain, directly reducing the orders of magnetic material enterprises, thereby forcing them to adjust production plans and lower operating rates.

Seasonal demand weakness combined with sluggish performance across multiple application sectors collectively led to an overall pullback in domestic demand in August. As a key growth driver for high-performance NdFeB magnetic materials, the NEV sector saw continued declines in both production and sales, reducing direct consumption of magnetic materials. In the home appliance sector, particularly air conditioner manufacturing, production schedules were gradually adjusted downward as the peak summer consumption season ended, lowering demand for related magnetic components. The 3C electronics market, lacking stimulation from revolutionary new models, reached saturation in overall production, making it difficult to provide significant incremental demand. Although long-term demand remains positive in industrial sectors such as wind power and industrial robots, August was similarly constrained by high summer temperatures. Factories in many regions adjusted operating hours or reduced production loads to cope with extreme heat and electricity peak periods, indirectly reducing short-term order demand for NdFeB permanent magnets.

The intensification of export policy barriers has exacerbated structural differentiation within the industry, becoming a key institutional factor affecting overall production. Although there is demand in the European and US markets, and exports are expected to remain at a relatively high level, the current export declaration and licensing system for NdFeB magnetic materials, in practice, channels export license resources more toward larger-scale, compliance-robust top-tier enterprises. Mid-tier and tail-end enterprises struggle to obtain export licenses smoothly under such policy conditions, leading to a loss of competitiveness in the international market and an inability to effectively secure overseas orders. As a result, their operating rates have further declined, exerting a noticeable drag on the national total magnetic material production in August. The trend of export orders concentrating in top-tier enterprises, while consolidating their dominant position, objectively constrains the overall capacity utilization, as the pace of capacity expansion among top-tier enterprises is unable to fully compensate for the market void left by the exit of small and medium-sized enterprises in the short term.

Looking ahead, the rare earth permanent magnet industry is undergoing an adjustment period triggered by the structural contradiction of "low-end surplus and high-end shortage." This involution is expected to gradually ease between 2026 and 2028, driven by policy-driven capacity exits, the emergence of new demand, and technological breakthroughs. In the short term, although rare earth raw material prices have pulled back slightly from their highs, supply remains tight due to constraints such as mining quotas, reduced imports of ore, and environmental protection policies. Downstream demand is expected to strengthen MoM as it enters the traditional peak consumption season, which will support magnetic material prices. In the long run, the rapid development of industries such as NEVs, wind power, and robotics will continue to drive growth in rare earth demand. The global NdFeB supply-demand gap may persist and widen over time, giving top-tier enterprises with resources, technological expertise, and customer barriers a competitive advantage.

![Overseas Pr-Nd offers surged rapidly, countries accelerated rare earth mine development [SMM Rare Earth Overseas Weekly Review]](https://imgqn.smm.cn/usercenter/wHkop20251217171744.jpeg)