01Introducción básica de la empresa y su estatus en la industria

Perfil

Fortescue Metals Group Ltd. (FMG) fue fundada en 2003 por el australiano Andrew Forrest mediante la adquisición y renombramiento de Allied Mining & Processing, cotizada en la ASX. FMG es líder global en la industria del mineral de hierro, destacando por su cultura corporativa única e innovación tecnológica. Ha desarrollado infraestructura y activos mineros de clase mundial en la región de Pilbara, en Australia Occidental, una de las principales zonas productoras de hierro. Es el tercer mayor productor de mineral de hierro de Australia y el cuarto a nivel mundial , después de Rio Tinto y BHP Billiton. A diferencia de los portafolios diversificados de Rio Tinto, BHP Billiton y Vale, FMG se enfoca exclusivamente en el mineral de hierro .

Negocios

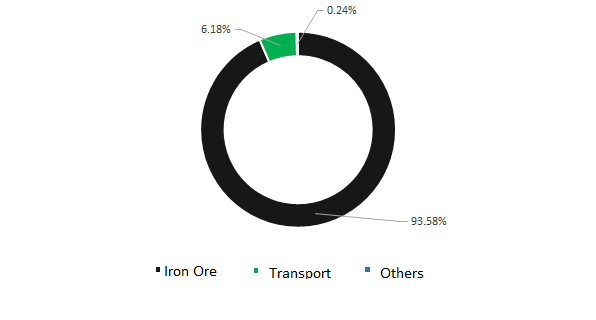

Según los informes financieros de Fortescue Metals Group, China representa el 89,7% de los ingresos totales de Fortescue. Más del 90% de su mineral de hierro se exporta a China. En sus primeros años, entre 2004 y 2006, Fortescue Metals Group firmó acuerdos de suministro a largo plazo con numerosas siderúrgicas chinas, incluyendo Hebei Wenfeng Steel Co. , Ltd., Jiangsu Fengli Group , y Jiangxi Pingxiang Steel Co., Ltd. Estos contratos de suministro le valieron la confianza del mercado de capitales, lo que impulsó el precio de sus acciones. Además, mediante financiación continua a través de diversos canales, Fortescue Metals Group acumuló fondos sustanciales para la exploración y desarrollo de mineral de hierro. El 15 de mayo de 2008, Fortescue Metals Group envió su primer cargamento comercial de mineral de hierro al puerto de Majishan de Shanghai Baosteel. La crisis financiera de 2008 sumió a Fortescue Metals Group, que había contraído una gran deuda, en una situación difícil, lo que llevó a la empresa a buscar capital de inversores. Fortescue Metals Group puso sus miras en Hunan Valin Steel Group Co., Ltd. (en adelante, "Grupo Valin") en China. En 2009, el Grupo Valin adquirió un total de 535 millones de acciones a un precio promedio de 2,38 AUD por acción mediante una colocación privada, obteniendo un 17,34% de participación y convirtiéndose en el segundo mayor accionista de Fortescue. El Grupo Valin invirtió en Fortescue durante lo más profundo de la crisis financiera. A medida que la economía mundial se estabilizó gradualmente, la producción y operaciones de Fortescue también aumentaron constantemente, y la crisis financiera se resolvió.

Principales componentes de ingresos del Grupo Fortescue (US$ mil millones)

Fuente de datos : Informe financiero de FMG SMM

02 Producción de mineral de hierro, envíos y principales productos

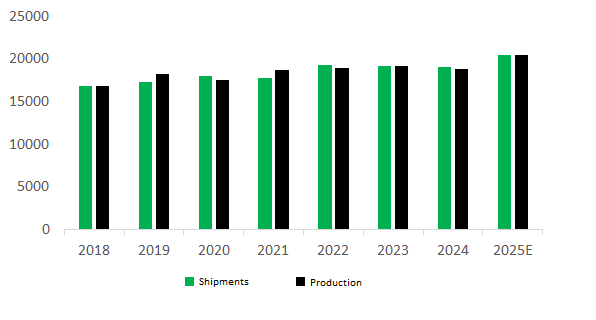

En 2004, Fortescue Metals Group (FMG) descubrió reservas de mineral de hierro en el área minera de Cloudbreak en la región de Pilbara, Australia Occidental. La empresa propuso posteriormente un plan de inversión de AUD 1,850 millones, proyectando una producción anual de 45 millones de toneladas de mineral de hierro. La construcción comenzó en Port Hedland en febrero de 2006, seguida del desarrollo a gran escala del puerto, ferrocarril y mina. En solo dos años, Fortescue Metals Group completó la infraestructura ferroviaria, inauguró el Puerto Fortescue Herb Elliott y comenzó la minería en su primera mina, Cloudbreak. El 15 de mayo de 2008, Fortescue Metals Group envió su primer cargamento de mineral de hierro al Puerto Maggie Hill de Shanghai Baosteel. La producción y los envíos han ido en aumento en los últimos años, con un objetivo de envío de 195-205 millones de toneladas para el año fiscal 2026.

Producción y envíos de mineral de hierro a lo largo de los años

Fuente de datos : Informe financiero de FMG SMM

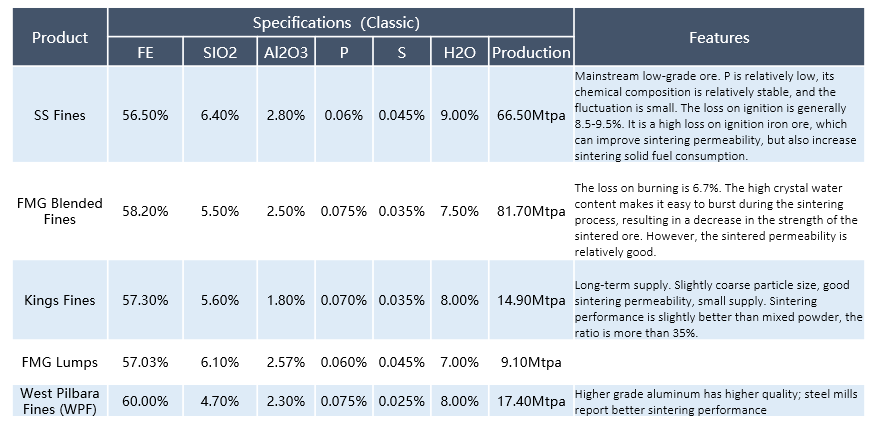

Productos

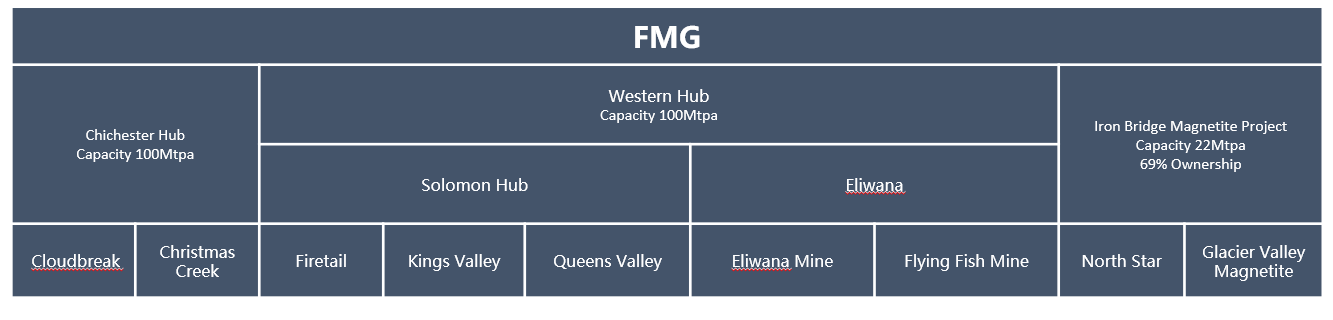

03 Situación de las minas del Grupo

1. Chichester Hub, incluyendo las minas Cloudbreak y Christmas Creek y tres instalaciones de procesamiento de mineral (OPFs), con una capacidad de producción anual de 100 millones de toneladas.

2. The Western Hub, compuesto por dos minas, Solomon y Eliwana, está ubicado cerca de las cordilleras Hamersley, 60 kilómetros al norte de Tom Price y 120 kilómetros al oeste del Chichester Hub. La mina Solomon comenzó operaciones en 2012, mientras que la mina Eliwana (140 kilómetros al oeste de la mina Solomon) inició producción en diciembre de 2020. Con su innovadora instalación de manejo de mineral de perfil bajo (OPF) y doble apiladora y recuperadora, la mina Eliwana tiene una capacidad de carga directa de hasta 9,000 toneladas por hora. The Western Hub tiene una capacidad de producción anual de 100 millones de toneladas.

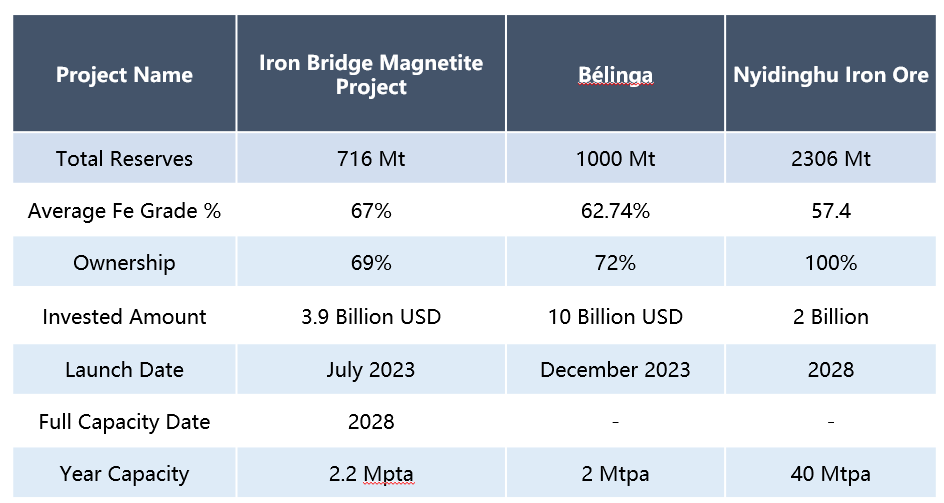

3. Proyecto de Magnetita Iron Bridge: El Proyecto Iron Bridge, ubicado 145 kilómetros al sur de Port Hedland, integra los yacimientos de magnetita de clase mundial North Star y Glacier Valley. Es una empresa conjunta no incorporada entre FMG Magnetite Pty Ltd (69%) y Formosa Steel IB Pty Ltd (31%). Cada parte es responsable de su participación accionaria en el gasto de capital total. El proyecto fue aprobado en septiembre de 2020, con una evaluación comercial completada en mayo de 2021. El primer envío de aproximadamente 200,000 toneladas será en septiembre de 2023, con una producción esperada de 13 millones de toneladas/año en 2024 y 22 millones de toneladas/año en 2028.

04Proyecto de Expansión Futura

el nuevo proyecto busca lograr una mayor expansión sobre la base de una producción estable

Los planes recientes de aumento de producción de FMG incluyen el Proyecto de Magnetita Iron Bridge, el Proyecto de Mineral de Hierro Galen Belinga y el Proyecto Nitinghu.

Actualmente, el proyecto Tieqiao ha entrado en producción desde mayo de 2023. El primer lote de envíos será de aproximadamente 200,000 toneladas en septiembre de 2023. El volumen de producción en 2024 será de 13 millones de toneladas y el volumen de envío será de 12 millones de toneladas. Se espera alcanzar una capacidad de producción de 22 millones de toneladas/año en 2028.

El Proyecto de Mineral de Hierro Belinga, ubicado en Gabón , es el primer proyecto de mineral de hierro de Fortescue Metals Group fuera de Australia, adquirido a través de su subsidiaria conjunta. Su objetivo es lograr una producción estable mientras busca una mayor expansión. El 4 de diciembre de 2023, el primer envío de mineral de hierro del Proyecto Belinga se cargó y envió con éxito. Actualmente, la mina Belinga aún se encuentra en las primeras etapas de operaciones de prueba y no ha comenzado oficialmente la producción a gran escala. Fortescue Metals Group está realizando extensas actividades de perforación para desbloquear gradualmente el potencial de producción del proyecto Belinga.

Nyidinghu , en desarrollo por Chichester Metals, una subsidiaria de Fortescue Metals, cubre aproximadamente 92,301 hectáreas y está valorado en aproximadamente US$2,000 millones (A$3,100 millones). La mina está planificada para producir aproximadamente 40 millones de toneladas de mineral de hierro anuales durante 26 años, con el primer mineral esperado en 2028.

05 Plan de Transformación Verde

Fortescue Metals Group planea invertir $6,200 millones para 2030 para lograr la transformación verde y la neutralidad de carbono en todas sus operaciones de mineral de hierro

Los proyectos clave de inversión y construcción incluyen:

1. El Proyecto de Metales Verdes , ubicado en la mina Christmas Creek, es una colaboración con el grupo China Baowu Steel para avanzar en la tecnología de hierro reducido directo (DRI) basada en hidrógeno. Con una inversión total de 50 millones de dólares, la planta tendrá una capacidad de producción anual de más de 1,500 toneladas de metal verde , con la primera producción prevista para el cuarto trimestre de 2025.

2. Tren Eléctrico de Mineral de Hierro (Infinity Train) : En asociación con Williams Advanced Engineering (WAE), la empresa está desarrollando el primer tren eléctrico de mineral de hierro con cero emisiones del mundo, llamado Infinity Train, que utiliza la recuperación de energía gravitacional en descensos para recargar sus baterías. Se espera que el tren esté operativo para 2026. Este tren es autosuficiente en su ciclo eléctrico, sin necesidad de cargador externo.

3. El proyecto Pilbara Energy Connect integra las necesidades fijas de energía de la región de Pilbara en una red eficiente. El proyecto incluye la construcción de granjas solares de 100 MW y 190 MW en North Star y Cloudbreak, respectivamente, junto con 500 km de líneas de transmisión y subestaciones asociadas. Se espera que la granja solar North Star se complete en 2024, mientras que la granja solar Cloudbreak se completará en la segunda mitad de 2026.

![[Comentario diario del acero inoxidable de SMM] El lado de financiación y la resonancia del níquel de la SHFE impulsan los futuros de SS, la demanda al contado de acero inoxidable se mantiene débil.](https://imgqn.smm.cn/usercenter/ocJKj20251217171717.jpg)