On the raw material side, dolomite prices show upward momentum influenced by reforms in the tender model, while demand-side magnesium smelting production rose 5.7% MoM to 85,000 mt, providing strong support. The ferrosilicon market remains supply-heavy with weak demand, balancing electricity price support against accumulating inventory. In energy costs, lump coal faces pressure from loose supply-demand dynamics, while semi-coke prices hold firm due to maintenance cycles. For hidden costs, normalized temperatures boosted smelting efficiency by 10%-15%, coupled with eliminated heat-prevention expenses and enhanced production stability, driving a notable pullback in overall costs.

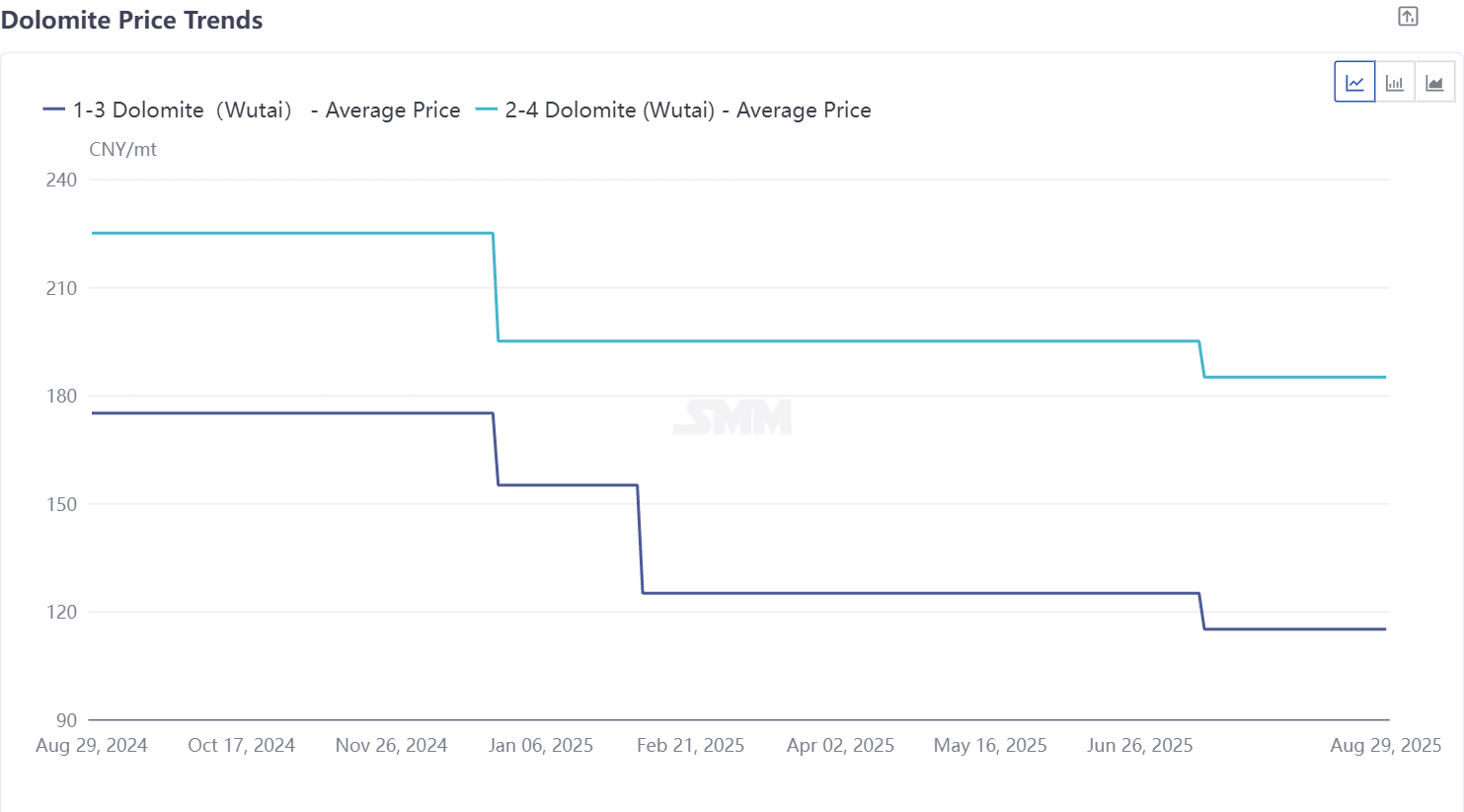

Dolomite: In September 2025, leading dolomite suppliers in Wutai will gradually adopt a tender-based sales model. Considering the impact of this transaction mode shift, dolomite prices may gain stronger upward momentum. Demand-side, magnesium smelters in major production hubs like Hubei and Inner Mongolia are increasing dolomite usage shares, limiting the reform’s influence. Additionally, primary magnesium smelter production is trending upward, with September output expected to rise 5.7% MoM to 85,000 mt. Given the projected demand uptick, dolomite’s price momentum is likely to strengthen.

Ferrosilicon: The ferrosilicon market exhibits a complex landscape. Recent production stays high, while post-restriction steel mill demand and seasonal peaks offer demand-side support. Cost-side, higher electricity prices provide a floor. Overall, the current supply-heavy, weak-demand pattern persists, with slight inventory buildup at production sites. Short-term drastic shifts are unlikely, and future price fluctuations hinge on market-moving news.

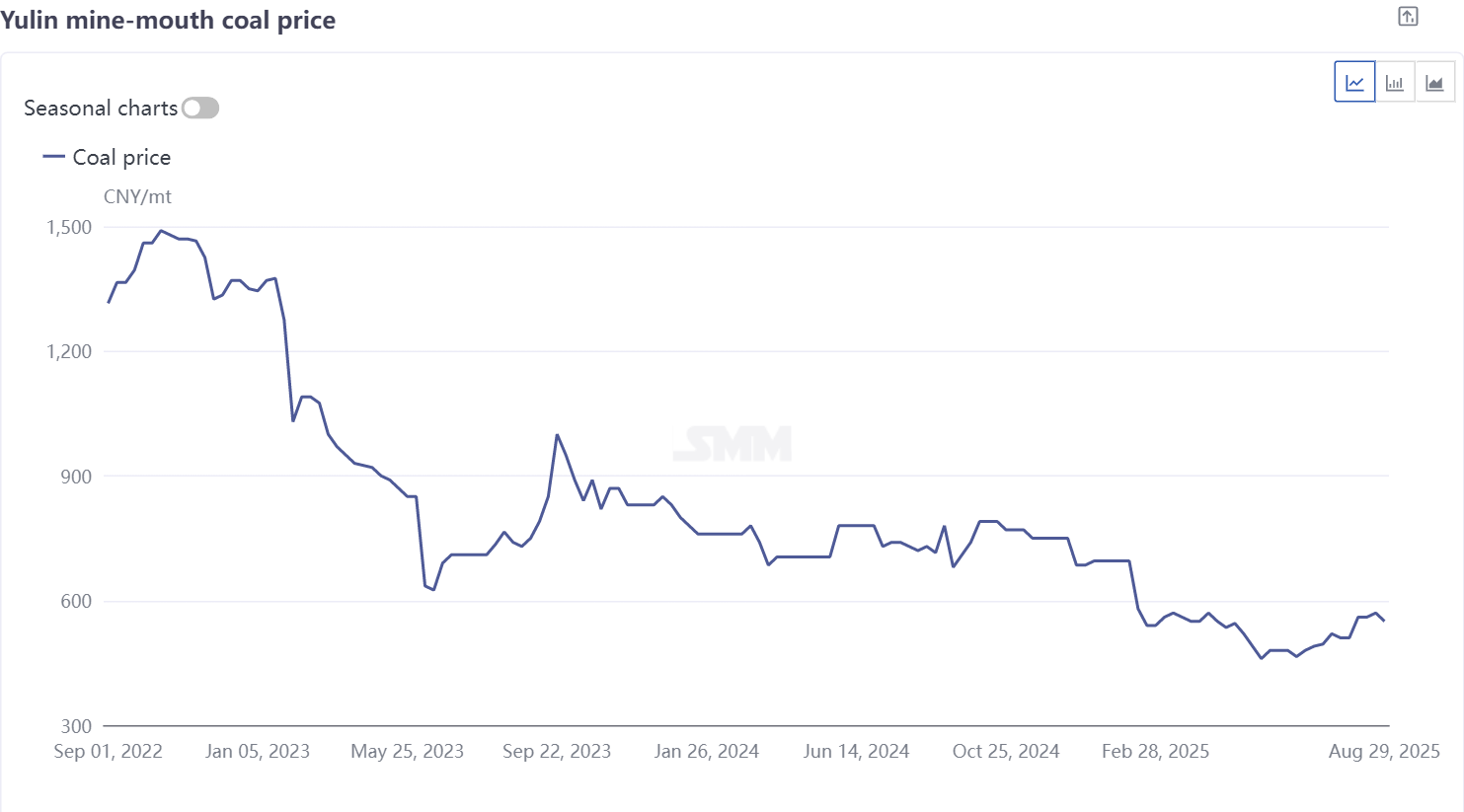

Energy Costs: Recently, steel mills in North China entered a maintenance wave, and as high temperatures eased, coal demand from energy-intensive industries softened. Multiple factors dampened downstream demand, reducing pithead transport vehicles and leaving lump coal prices in the doldrums. September coal demand may weaken further. Meanwhile, enhanced safety inspections around Beijing prompted some mines to halt post-monthly quota fulfillment, tightening lump coal supply. September supply is expected to rise. Combined, lump coal fundamentals may tilt toward supply-heavy, weak-demand dynamics, pressuring prices. Some semi-coke plants plan maintenance in early September, resuming gradually mid-to-late month, likely keeping semi-coke prices firm.

Hidden Costs: In September, temperatures returned to the suitable range, fundamentally improving the high-temperature environment in magnesium plant production workshops. Employee leave frequency significantly decreased, and production team stability was restored, effectively avoiding the productivity decline caused by labor shortages in July. Meanwhile, the suitable temperature conditions stabilized smelting equipment operation, shortening the smelting cycle by 10%-15% compared to July, thereby reducing additional time costs and energy consumption losses due to prolonged production processes. Additionally, with the end of the high-temperature season, extra expenses such as heatstroke prevention measures and equipment overload protection, previously invested to cope with extreme weather, were correspondingly eliminated, further driving a pullback in hidden costs.

![Magnesium Ingot Transactions Increased, Rigid Demand Support Became More Evident, and a One-Sided Market Trend Was Unlikely in the Short Term [SMM Spot Magnesium Ingot Flash Report]](https://imgqn.smm.cn/usercenter/hSSxt20251217171722.jpeg)

![High Costs Drove a Second TiO2 Price Increase Within the Month, While Diverging Domestic and External Demand Tested the Sustainability of the Price Rise [SMM Titanium Spot Flash Report]](https://imgqn.smm.cn/usercenter/pAOxy20251217171725.jpg)