Malaysia, August 2025 — Malaysia’s stainless-steel scrap market has long been shaped by exports. With limited domestic capacity to absorb material, selling abroad has become the default. India now stands as the largest buyer, while China, despite offering firmer prices, remains a difficult destination thanks to its exacting import rules.

Price comparison: narrowing margins between Malaysia and China

SMM Research shows that domestic prices for 304 stainless-steel scrap in Malaysia range at RM4.6-6.2/kg (around 1.09–1.47 US$/kg). The spread reflects sharp differences in quality: clean industrial off-cuts command higher prices, while dismantled or impurity-laden scrap trades at the lower end.

According to SMM data, quotations in Foshan—the heart of China’s stainless trade—stand at RM5.6–5.82/kg (around 1.32–1.38 US$/kg). That is only a shade higher than Malaysia’s average. The gap, at about RM1/kg (0.23 US$/kg), leaves scant room for profitable arbitrage.

Two routes: big traders export, small ones stay at home

For now, the flows of Malaysia’s stainless-steel scrap are clearly divided:

-

Large traders focus on exports, particularly to India, where the abundance of buyers and flexible collection terms foster long-term stability.

-

Smaller traders sell mainly into the domestic market, though limited smelting capacity constrains demand.

This split—“big traders ship abroad, small traders sell at home”—has left Malaysia unable to form a credible domestic benchmark, with prices instead dictated by external markets.

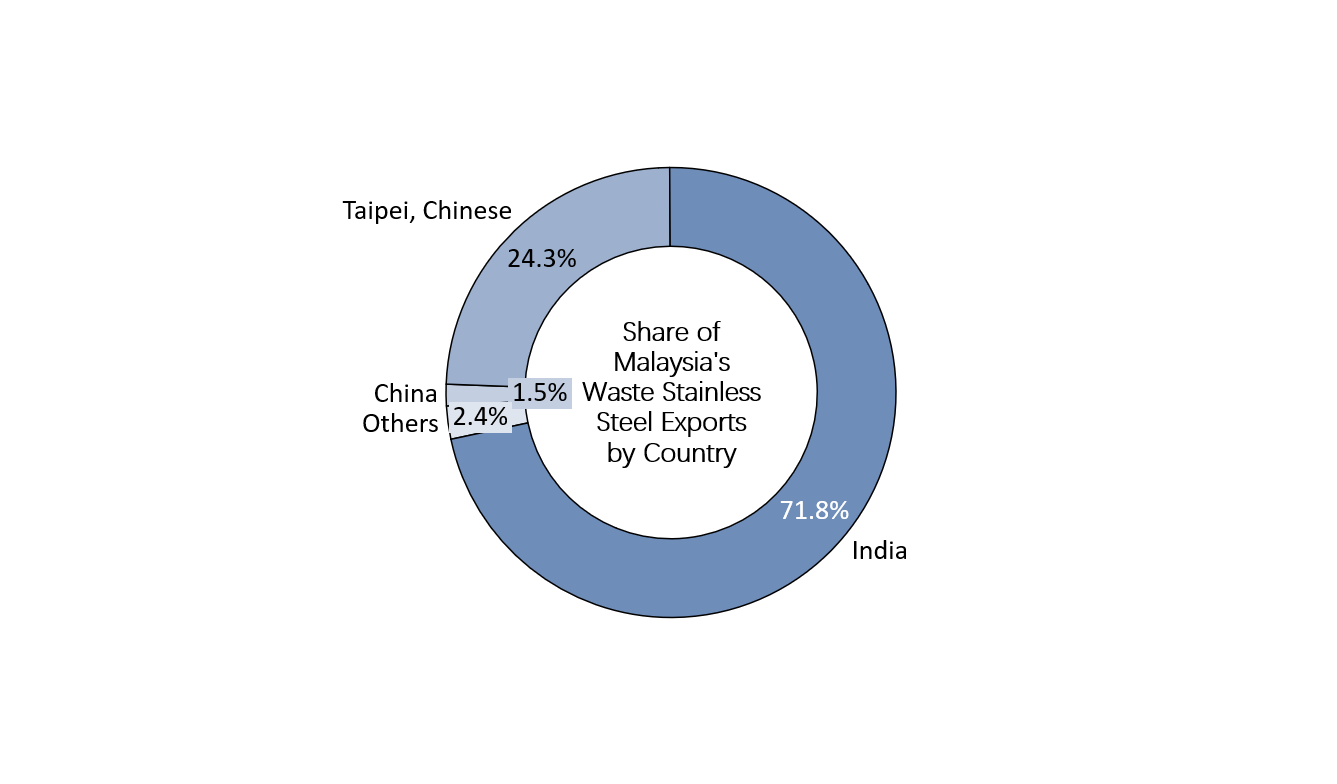

India takes more than 70%

Data from Trademap.org illustrate the imbalance. In 2024, Malaysia’s stainless-steel scrap exports went chiefly to:

-

India: 5,153 (71.8%)

-

Taiwan (Chinese Taipei): 1,746 (24.3%)

-

Belgium: 113 (1.6%)

-

China: 111 (1.5%)

-

Singapore: 25 (0.3%)

-

UAE: 25 (0.3%)

India remains Malaysia’s natural outlet, thanks to simple import rules and a well-established buyer network.

Sources: Trademap.org, SMM

Policy and regulation: Malaysia free, India easy, China strict

Policy helps explain the divergence. In 2021 Malaysia introduced a Ferrous Scrap Export Duty, but stainless scrap was excluded. Exports thus remain free of charge and unrestricted.

China is another matter. Since 2020 it has enforced GB/T 39733-2020 “Recycled Steel Raw Materials”, a national standard demanding strict controls on composition, radiation, and paperwork. For most Malaysian yards, compliance is prohibitively complex.

India, by contrast, imposes few constraints. Import procedures are simple and fast, reasons why it has become Malaysia’s natural export destination.

Industry voices

“Most of the material still goes to India,” admits one recycler. “China’s demand is large, but the procedures are too complicated.”

Another trader was blunter: “We don’t even know how China’s procedures actually work. We just hear they are very complex. Without clear channels, we dare not even try.”

Outlook

Malaysia’s stainless-scrap trade is marked by uneven quality and divided flows. In the short term, India will remain the primary outlet. But if Malaysia can raise its game in sorting, testing, and certification, it may yet crack the higher-value Chinese market. Until then, the lion’s share of its scrap will keep sailing west.

![[SMM Stainless Steel Flash] Indonesian Major Mill Hikes 316L Export Price by $100/t](https://imgqn.smm.cn/usercenter/NHXhQ20251217171733.jpg)