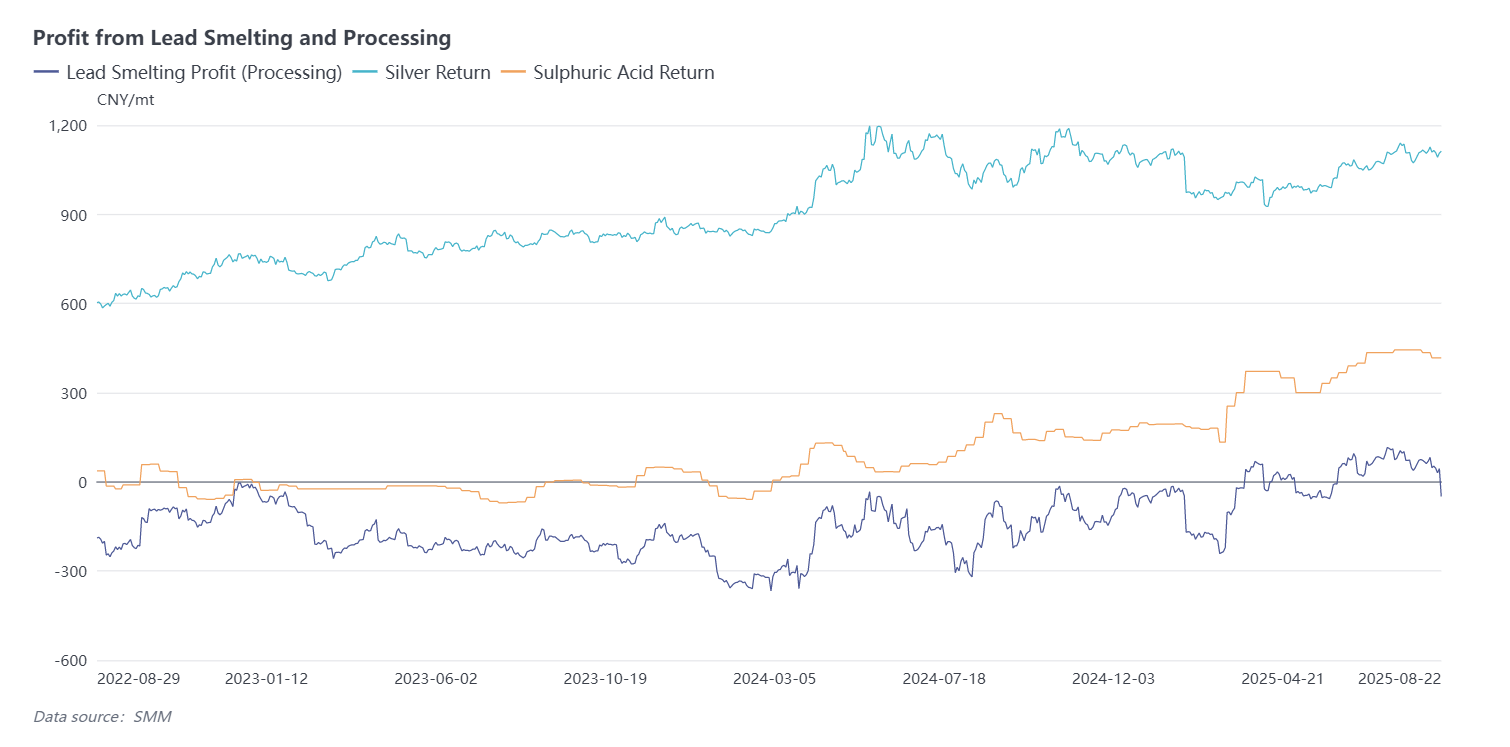

According to SMM, the significant rise in prices of by-products such as precious metals and sulphuric acid from lead smelting in H1 2025 greatly boosted the production enthusiasm of primary lead smelters. However, this has sown the seeds for a supply-demand imbalance of lead concentrates in H2. Although the mining and processing activities at domestic lead-zinc mine projects have increased, the actual output of lead concentrates did not rise substantially due to the low grade of associated lead in raw ore. Therefore, while the TCs for zinc concentrates arriving at smelters increased, lead concentrate TCs continued to face a situation where they are more likely to fall than rise.

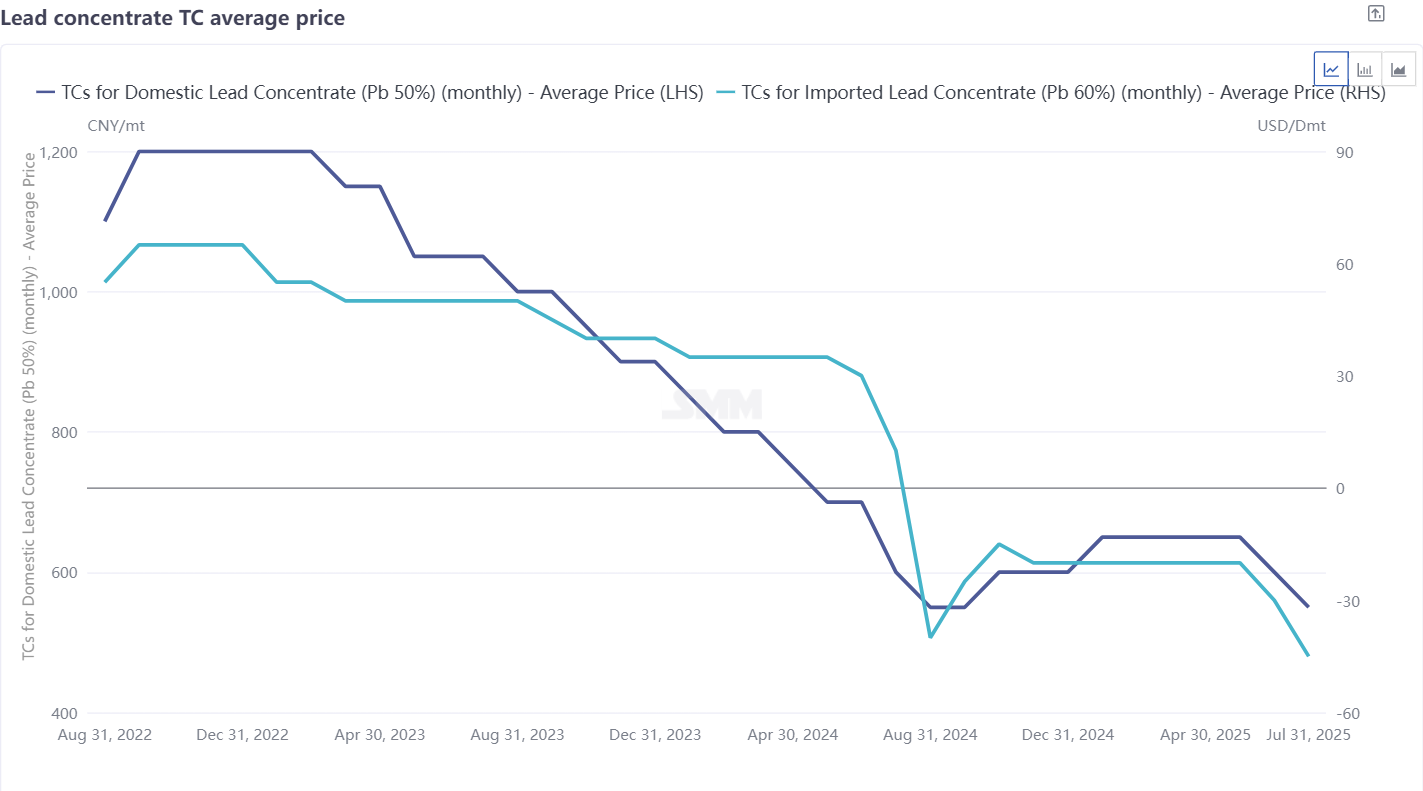

In terms of market quotations, compared with imported lead concentrates, the changes in TCs for domestically produced lead concentrates were more moderate. On one hand, under the long-term fixed cooperation model between major domestic lead-zinc mines and smelters or traders, the decline in mainstream lead concentrate TCs was much smaller than the prices determined through tender and bid methods. On the other hand, some smelters, in addition to using lead concentrates, can also obtain supplements from other lead-containing materials, allowing them to quote relatively higher TCs for lead concentrates due to their lower dependence on lead concentrates.

In mid-to-late August, the circulation of goods in the domestic lead ore trading market became tight again, with most offers being in the form of forward sales. Multiple lead-zinc mines in Inner Mongolia and Guangxi stated that current demand orders for lead ores have been scheduled for the next 2-3 months, and some projects have even completed the pre-sale tenders for their entire 2025 annual lead concentrate production. In contrast, zinc concentrates still settled on a monthly basis without similar queuing for forward sales. At the same time, there were few quotes for imported lead concentrates, leading to a "hard-to-find" situation in the market, especially for those lead concentrates containing multiple metal elements, whose TCs were raised, or the payable indicators for silver content were adjusted upward. Some small smelters reported a decrease in days of raw material inventories and expressed concerns about the stability of lead concentrate supply in Q4. Even though primary lead smelters will enter regular maintenance periods in September, and some companies tried to increase prices in summer to gain more room for winter negotiations, this did not change the pessimistic expectations regarding the supply-demand relationship of lead concentrates.

In September, the SMMpb50TC price was reduced by 50 yuan/mt in metal content to 450 yuan/mt in metal content (price range: 350-550), and the SMMpb60TC price was lowered by $30/dmt to -$90/dmt (price range: -110~-70). Although more primary lead smelters were expected to undergo maintenance in the autumn, market participants remained cautious about the future of lead concentrate TCs due to limited growth in lead concentrate supply. The arrival of imported lead concentrates in Q3 did not effectively alleviate the tight supply, and a rebound in lead concentrate TCs is unlikely in the short term.