Europe's Dependence on Chinese Rare Earth Magnetic Materials Continues to Highlight

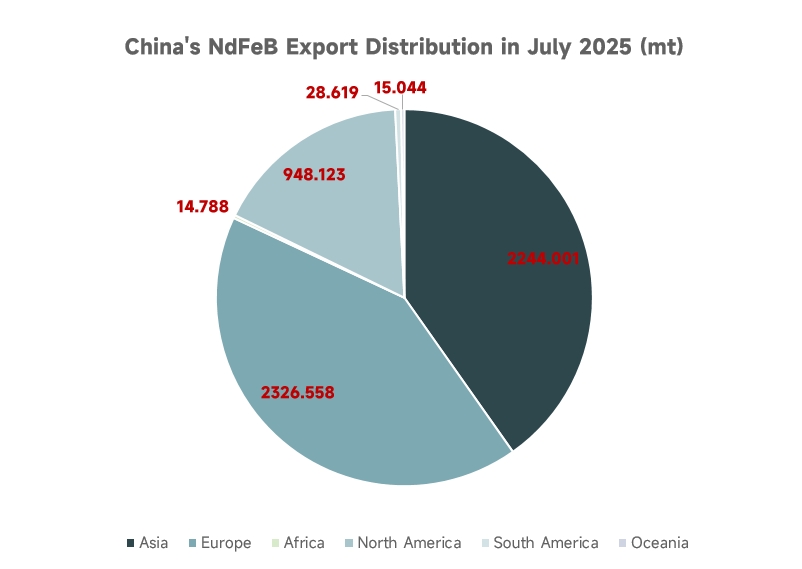

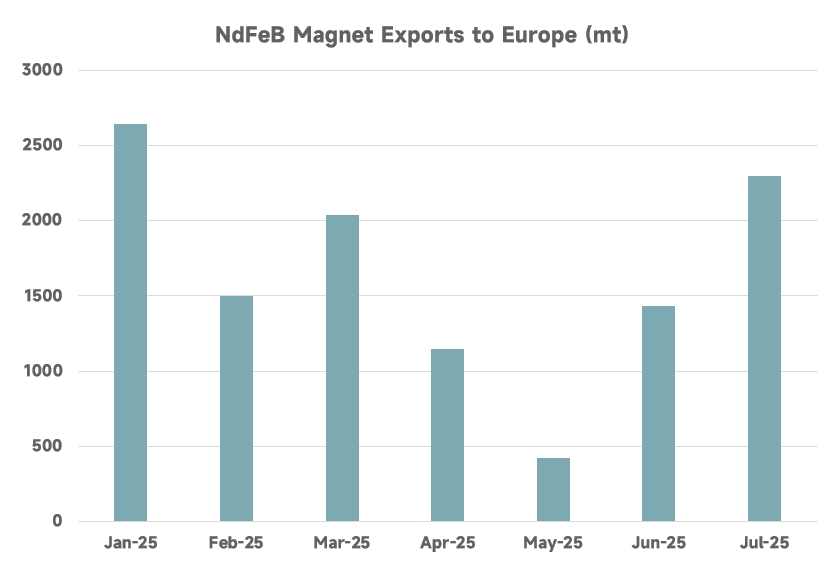

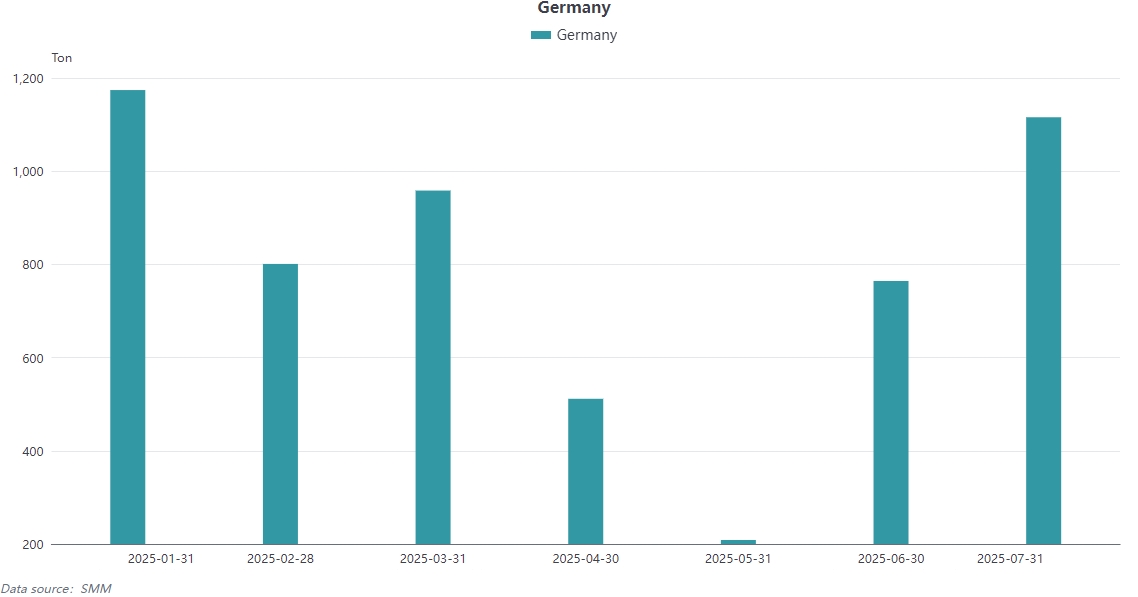

In July 2025, China's total exports of NdFeB permanent magnets reached 5,577.13 mt, up 77.95% MoM, with exports to Europe at 1,528.85 mt, accounting for 27% of the total monthly exports. Cumulative data from January-July 2025 shows that China exported 11,476.77 mt of rare earth permanent magnets to Europe, representing 41% of its global exports. Germany, as the largest demand country in Europe, imported 5,534 mt from January to June, making up 48% of the total European imports, reflecting a deep reliance of the European new energy industry on China's supply chain.

Europe Is Promoting Supply Chain Autonomy Through Local Projects and Technological Innovation

Solvay of France recently completed the expansion of its rare earth plant in La Rochelle (operational since 1948), and it is expected to meet 30% of Europe's magnetic rare earth demand by 2030. Currently, the plant is producing small batches of Pr-Nd oxide for permanent magnets and exploring separation technologies for heavy rare earths such as terbium and dysprosium. The Norwegian REEtec plant uses low-carbon solvent extraction technology, aiming to trial produce Pr-Nd by the end of 2025, with a 90% reduction in carbon emissions, setting a benchmark for environmental protection in refining in Europe. Canadian company Neo Performance Materials operates the only NdFeB sintering plant in Europe, located in Estonia, with a capacity of 2,000 mt/year. It plans to make commercial deliveries by 2026, marking a crucial step towards localization.

Circular Economy and International Cooperation Become Strategic Priorities in Europe

Solvay plans to meet 30% of its rare earth demand by 2030 through recycling retired motors (the current recycling rate is less than 1%) and will collaborate with Canada's Cyclic Materials to obtain recycled raw materials. The Japanese government has funded the construction of a refinery by France's Carester in Lac, aiming to produce heavy rare earth oxides by 2026, with 70% of the capacity already reserved by automakers such as Stellantis. The EU Critical Raw Materials Act explicitly requires 40% local processing and 25% recycling rates by 2030 and provides 1.7 billion euros in funding to advance magnet capacity projects.

European new energy and industrial giants form the core of magnetic material demand.

Automakers such as Volkswagen, BMW, and Mercedes-Benz rely on Chinese magnetic materials for their permanent magnet motors, with Zhong Ke San Huan supplying 35% of the magnetic materials for Tesla's European factory; Siemens' offshore wind turbines require high coercivity magnets, Bosch's industrial robots consume over 2,000 mt of magnets annually, and Airbus satellites use radiation-resistant magnets exclusively supplied by Tianhe Magnetics. The demand from these enterprises is driving Europe to accelerate localization, but in the short term, it remains difficult to break away from the rigid dependence on China's supply chain.

Resource development focuses on low-risk and sustainable mining areas.

The EU's REEsilience project screened 149 rare earth deposits globally, identifying the Fen mine in Norway, the Kiruna mine in Sweden, and Greenland as high-quality resources with low environmental and social risks (ESG). The Fen mine in Norway has reserves of 8.8 million mt, with a high proportion of light rare earths, and is expected to start production in 2030; the Kiruna mine in Sweden, due to the environmental assessment process, will be delayed until 2035, highlighting the challenges in development timelines. Leveraging its nuclear power advantages and political support, France leads nine EU critical raw material projects, attracting companies such as UK's Less Common Metals to set up refining capacity.

Resource endowment and environmental protection policy form a dual shackle.

European rare earth deposits are concentrated in the northern cold regions and Greenland, where mining requires overcoming technological bottlenecks related to permafrost and deep-sea operations. Moreover, due to radioactive waste management disputes, the environmental assessment process for Norway's Fen Mine (with reserves of 8.8 million mt) and Sweden's Kiruna Mine has been extended to 10-15 years, with costs surging by 30%-50%. This has forced the EU to lower its 2030 domestic mining target to 10%. Stringent environmental standards further constrain smelting capacity — although France's Solvay plant possesses full-range separation technology, it cannot increase production due to wastewater discharge restrictions, and the controversy over uranium by-product processing in Greenland has directly led to the project being shelved.

Geopolitical divisions tear apart supply chain collaboration.

After Brexit, the UK turned to the US-led "Minerals Security Partnership" (MSP), but the US's own shortage in rare earth refining capacity could not provide an immediate alternative; German automakers, to secure their production lines, expedited the procurement of Chinese magnetic materials through a "green channel," with imports from January-June 2025 accounting for 48% of the total European volume, indirectly weakening the EU's unified negotiating position; the "European Rare Earth Alliance" promoted by France failed to make significant progress due to frequent changes in government.

Technological autonomy is trapped in a raw material shortage dilemma.

Europe's only domestic magnetic material plant (with a capacity of 2,000 mt/year owned by Canada's Neo in Estonia) has delayed its commercial delivery from 2026 to 2028 due to a lack of heavy rare earth separation capability and reliance on Chinese dysprosium and terbium raw materials. Swedish LKAB's recycling technology for extracting rare earths from iron ore scrap has been boycotted by customers such as BMW and Siemens because the purification cost is four times higher than that of primary ore in China. Although the EU holds 12% of rare earth patents, China has blocked 37 core processes, including grain boundary diffusion technology (which reduces dysprosium usage to 0.8%), causing European magnets to lag one generation behind in performance.

Recycling strategies encounter practical efficiency bottlenecks.

Solvay plans to meet 30% of demand through recycling by 2030, but the current e-waste recycling rate is less than 1%, and the energy consumption for dismantling waste motor magnets is 200% higher than in China. The France-Japan cooperative recycling pilot plant has a capacity of only 800 mt/year, which is less than 2% of Europe's demand. Platinum alloy alternative materials, with a BHmax only 60% that of NdFeB and double the cost, have been deemed "uncommercializable within a decade" by Volkswagen and Bosch.

Strategic Reserves Expose Supply Chain Vulnerability

The EU secretly implemented a "rare earth reserve plan," but the inventory only supported three months of demand, far below the nine-month safety line for natural gas reserves. In June 2025, German automakers faced depleted inventories due to approval delays and were forced to accept supervision by China's tracking system, requiring each batch of magnets to be accompanied by a commitment letter stating they would not be used for military purposes, highlighting a passive situation marked by sovereignty concessions.

Finally, we cannot deny that Europe indeed has a very broad market for rare earths. However, whether the rare earth industry chain will continue to rely on China or can effectively rise and build its own industry chain remains to be observed. SMM will also continue to monitor the dynamics of the European market in the future.

![Rare Earth Prices Hold Up Well, and Market Inquiry Activity Increases [SMM Rare Earth Weekly Review]](https://imgqn.smm.cn/usercenter/AJTtH20251217171744.jpg)