After the tariff shock and global trade adjustments, the copper market remains tight in 2025. Data shows that US refined copper inventories have surged to a 21-year high, following front-loaded imports by traders seeking to avoid potential tariffs and capture inter-market arbitrage. Imports slowed in July after this pre-loading phase. The final tariff outcome exempted copper cathodes but imposed a 50% duty on semi-finished products, further distorting global trade flows. As a result, the US refined copper market is facing a clear mismatch between short- and long-term supply-demand, and market sentiment has turned cautious.

On the demand side, global refined copper consumption is expected to grow by nearly 4.5% in 2025, driven mainly by Chinese industrial activity and stimulus policies, with significant growth in the first half of the year. Mine supply, however, is forecast to rise just 0.5%, while refined output is expected to increase by only 1.9%—largely due to higher Chinese production offsetting overseas cutbacks. This structural imbalance remains, and the global refined copper deficit is projected to widen further in 2026, with regional supply chain “internal circulation” becoming more evident.

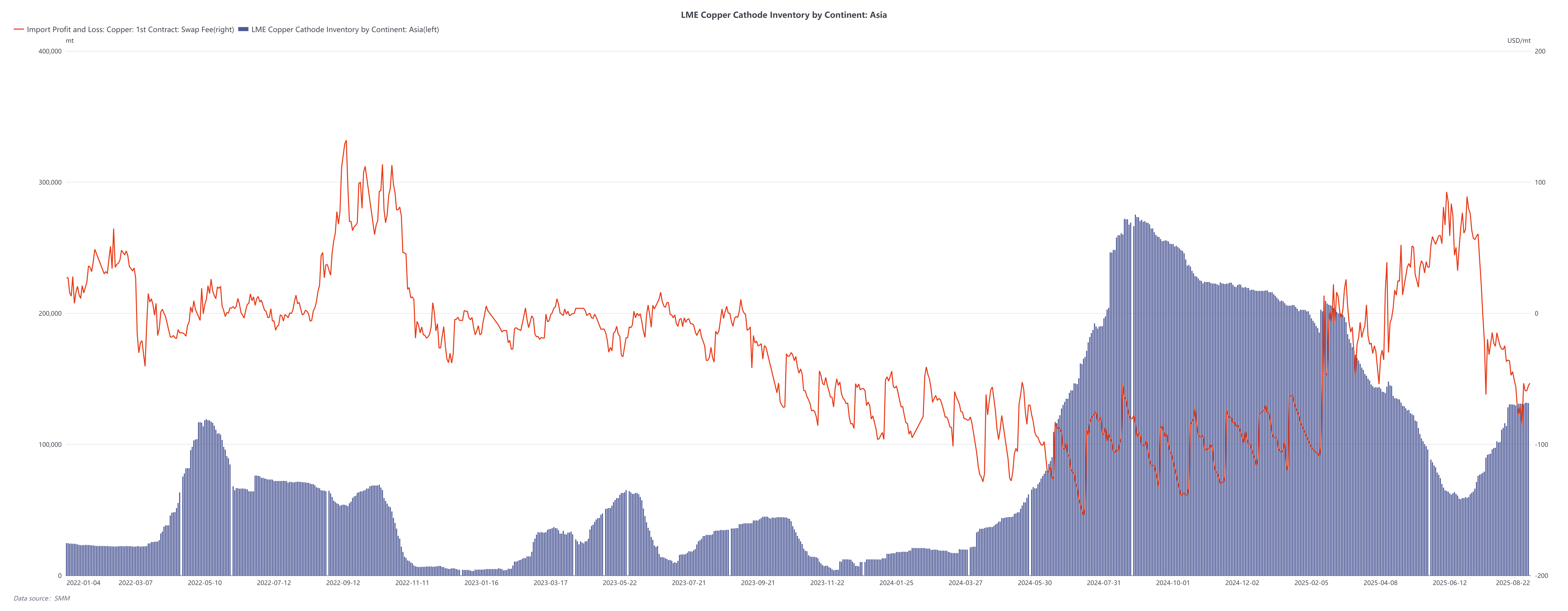

Meanwhile, LME Asian inventories have continued to build since the second half of 2024, reflecting a redistribution of global trade flows. However, despite the stock build, LME nearby spreads have weakened since June 2025, pointing to softer Asian physical demand. Earlier this year (February–April), tight nearby spreads highlighted prompt shortages, but the recent decline indicates short-term pressure has eased. Looking ahead, inventory builds are more likely to concentrate in the US, while the current LME-COMEX arbitrage suggests little inclination for US cathode outflows.

Outlook:

Although fundamentals remain tight, the combination of “rising inventories + weakening spreads” underscores demand-side uncertainty. Market participants expect that as China’s import window gradually reopens in late August, bonded zone destocking will accelerate, brand premiums will narrow, and spot trading will revert to SHFE/LME arbitrage-driven logic. Overall, copper price volatility is likely to stay elevated, with trade policy and uneven global growth continuing to reshape international copper flows.