หลังจากช็อกภาษีและปรับโครงสร้างการค้าทั่วโลก ตลาดทองแดงยังคงตึงตัวในปี 2025 ข้อมูลแสดงว่า สต็อกทองแดงบริสุทธิ์ของสหรัฐเพิ่มขึ้นถึงระดับสูงสุดในรอบ 21 ปี หลังจากผู้ค้านำเข้าล่วงหน้าเพื่อหลีกเลี่ยงภาษีที่อาจเกิดขึ้นและการทำกำไรจากการซื้อขายระหว่างตลาด การนำเข้าชะลอลงในเดือนกรกฎาคมหลังจากช่วงการนำเข้าล่วงหน้า สุดท้ายผลของการตัดสินใจเรื่องภาษียกเว้นทองแดงแท่งแต่กำหนดภาษี 50% สำหรับผลิตภัณฑ์กึ่งสำเร็จรูป ทำให้การไหลเวียนของการค้าทั่วโลกบิดเบี้ยวมากขึ้น ดังนั้นตลาดทองแดงบริสุทธิ์ของสหรัฐกำลังเผชิญกับความไม่สอดคล้องระหว่างอุปสงค์และอุปทานระยะสั้นและระยะยาว และความรู้สึกของตลาดกลายเป็นความระมัดระวัง

ด้านความต้องการ คาดว่าการบริโภคทองแดงบริสุทธิ์ทั่วโลกจะเติบโตประมาณ 4.5% ในปี 2025 โดยได้รับแรงขับเคลื่อนหลักจากกิจกรรมทางอุตสาหกรรมและการกระตุ้นเศรษฐกิจของจีน มีการเติบโตอย่างมากในครึ่งแรกของปี อย่างไรก็ตาม การผลิตจากเหมืองคาดว่าจะเพิ่มขึ้นเพียง 0.5% ในขณะที่การผลิตทองแดงบริสุทธิ์คาดว่าจะเพิ่มขึ้น 1.9% เนื่องจากการผลิตของจีนเพิ่มขึ้นชดเชยการลดลงจากต่างประเทศ ความไม่สมดุลโครงสร้างนี้ยังคงอยู่ และคาดว่าขาดแคลนทองแดงบริสุทธิ์ทั่วโลกจะขยายตัวมากขึ้นในปี 2026 พร้อมกับการหมุนเวียนภายในของห่วงโซ่อุปทานในภูมิภาคที่เห็นได้ชัดเจนมากขึ้น

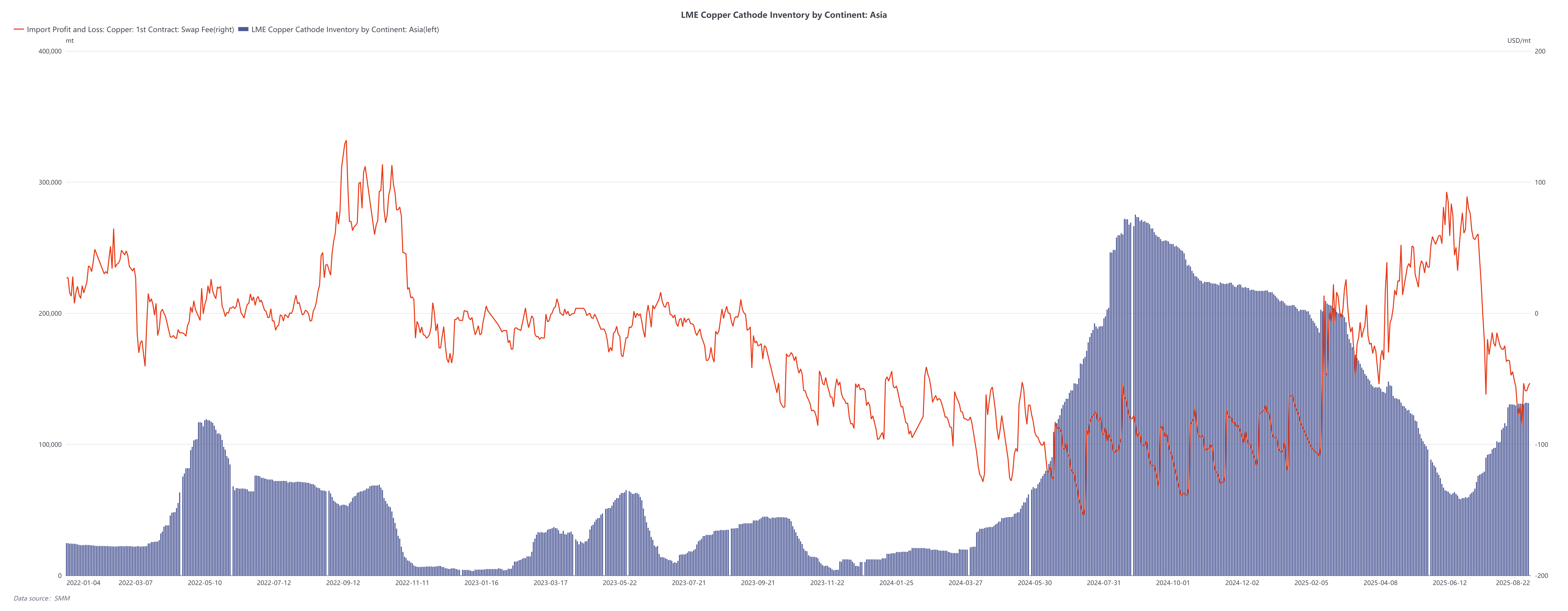

ในขณะเดียวกัน สต็อก LME ในเอเชียเพิ่มขึ้นต่อเนื่องตั้งแต่ครึ่งหลังของปี 2024 สะท้อนถึงการกระจายใหม่ของการไหลเวียนการค้าทั่วโลก อย่างไรก็ตามแม้ว่าสต็อกจะเพิ่มขึ้น แต่สเปรดใกล้เคียงของ LME อ่อนแอลงตั้งแต่เดือนมิถุนายน 2025 ชี้ให้เห็นว่าความต้องการทางกายภาพในเอเชียอ่อนแอลง ในช่วงต้นปีนี้ (กุมภาพันธ์-เมษายน) สเปรดใกล้เคียงที่ตึงตัวแสดงถึงภาวะขาดแคลนที่เร่งด่วน แต่การลดลงล่าสุดบ่งบอกว่าแรงกดดันระยะสั้นได้คลายลง มองไปข้างหน้า การสะสมสต็อกมีแนวโน้มที่จะรวมศูนย์ในสหรัฐ ในขณะที่การเก็งกำไร LME-COMEX ปัจจุบันชี้ให้เห็นว่าไม่มีแนวโน้มที่จะมีการส่งออกทองแดงแท่งออกจากสหรัฐ

แนวโน้ม:

แม้ว่าพื้นฐานยังคงตึงตัว แต่การผสมผสานของ "สต็อกเพิ่มขึ้น + สเปรดอ่อนแอ" ชี้ให้เห็นถึงความไม่แน่นอนทางด้านความต้องการ ผู้เข้าร่วมตลาดคาดว่าเมื่อหน้าต่างการนำเข้าของจีนค่อยๆ เปิดขึ้นในปลายเดือนสิงหาคม การลดสต็อกในเขตปลอดอากรจะเร่งขึ้น พรีเมียมแบรนด์จะแคบลง และการซื้อขายสปอตจะกลับมาขับเคลื่อนโดยตรรกะการเก็งกำไร SHFE/LMEโดยรวมแล้ว ความผันผวนของราคาทองแดงน่าจะยังคงอยู่ในระดับสูง เนื่องจากนโยบายการค้าและการเติบโตทางเศรษฐกิจที่ไม่สม่ำเสมอทั่วโลกยังคงเปลี่ยนแปลงการไหลเวียนของทองแดงระหว่างประเทศ