Depuis avril 2022, l'échantillon de l'enquête SMM sur la planification de la production de barres d'armature a été élargi pour inclure 56 entreprises.

Selon les données de l'enquête SMM menée auprès de 56 entreprises clés de production d'acier :

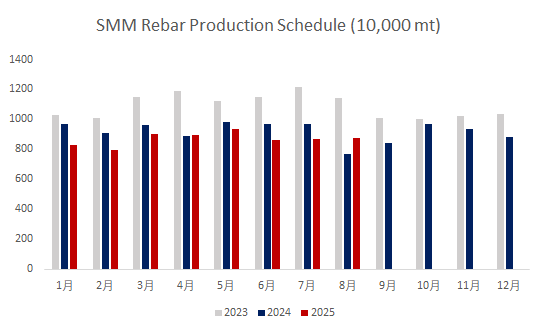

- La production planifiée de barres d'armature pour août était de 8,776 millions de tonnes, soit une augmentation de 114 700 tonnes par rapport à la production réelle de juillet, représentant un taux de croissance de 1,32 % ;

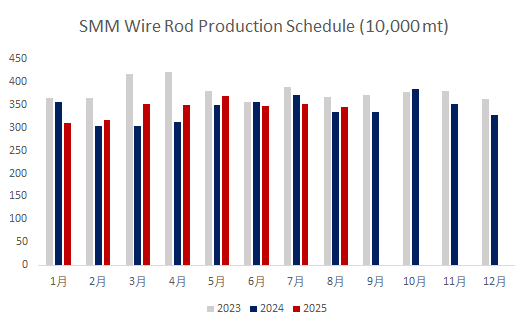

- La production planifiée de fil machine pour août était de 3,4541 millions de tonnes, soit une diminution de 65 700 tonnes par rapport à la production réelle de juillet, représentant un taux de baisse de 1,87 %.

Graphique 1-2 : Planification de la production de barres d'armature et de fil machine dans les aciéries (56 aciéries)

Source des données : SMM

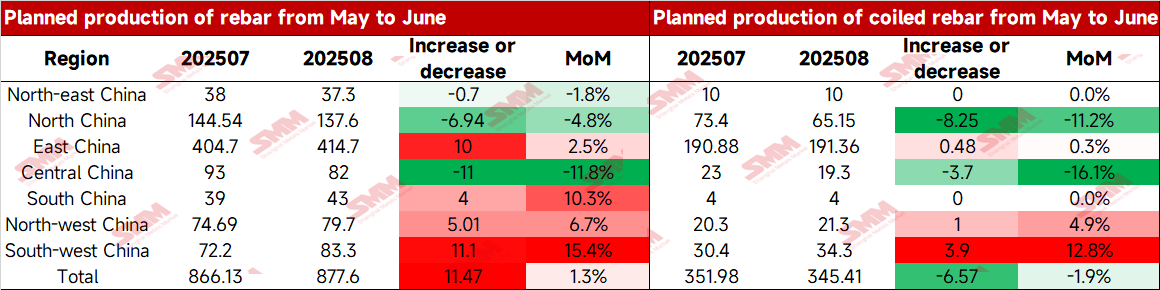

Tableau 1 : Planification de la production réelle de barres d'armature et de barres d'armature enroulées en mai et volume de production prévu en juin (10 000 tonnes)

Globalement :

En juillet, le prix de l'acier de construction à l'échelle nationale a fluctué à la hausse. Le marché avait de grandes attentes pour la réunion du Bureau politique du Comité central, et il y avait des nouvelles positives du côté des matières premières. De plus, l'investissement dans le projet de centrale hydroélectrique du fleuve Yarlung Zangbo dans l'industrie a stimulé l'enthousiasme pour l'acier fini, stimulant le renforcement continu des prix au comptant. Du côté des coûts, le prix de l'acier fini a augmenté en même temps que celui des matières premières, et les bénéfices de nombreuses aciéries se sont améliorés, avec des bénéfices globaux allant de (-100 à 300) yuan/tonne. En août, les aciéries prévoyaient d'augmenter la production de barres d'armature et de diminuer la production de fil machine, avec une légère augmentation de la production totale. Les aciéries de la région du Nord avaient un bénéfice brut de plus de 300 yuan/tonne pour la production de tôles et de bandes, et en août, le métal chaud serait priorisé pour assurer la pleine production des lignes de laminage de tôles et de bandes, de sorte qu'il était prévu d'arrêter les lignes de laminage de fil machine. En revanche, les aciéries de l'Est de la Chine prévoyaient de reprendre la production de hauts fourneaux d'ici la fin du mois, avec une augmentation de la production de barres d'armature. Les aciéries des autres régions ont pour la plupart maintenu une production normale.

En résumé, les aciéries sont axées sur les bénéfices et choisissent les variétés à marge élevée. Cependant, compte tenu de la « saison creuse plus forte que d'habitude » cette année, les aciéries n'ont actuellement aucun plan de réduction de production clair, et il y a toujours des attentes pour une augmentation de la production de matériaux de construction dans la période ultérieure.

![[SMM HRC Échanges quotidiens] Le volume des transactions au comptant a augmenté](https://imgqn.smm.cn/usercenter/VgxkU20251217171719.jpg)

![[Revue quotidienne SMM des tôles et plaques] Les tôles et plaques se consolident, focus à court terme sur le sentiment des coûts.](https://imgqn.smm.cn/usercenter/hyiDc20251217171715.jpg)