For a long time, China has established absolute authority in the rare earth sector by leveraging its reserve advantages and monopoly in smelting and separation technologies. However, as the US-China rivalry intensifies, the US has accelerated the reconfiguration of the rare earth supply chain in collaboration with its allies through the Critical Minerals Act, promoting a process of "de-Sinicization." For example, Lynas Corporation of Australia achieved commercial separation of dysprosium oxide in Malaysia in 2025, becoming the first producer of heavy rare earths outside of China. The US, on the other hand, has supported domestic projects such as the Round Top mine (which is expected to separate dysprosium oxide in January 2025 and commence production in 2026) and has injected equity capital into and imposed price caps on MP Materials, the mineral developer of Mountain Pass in the US, in an attempt to reduce its reliance on China's medium-heavy rare earths (previously, 70% of the US's rare earth imports originated from China). Against this backdrop, China's close monitoring of overseas rare earth developments is a crucial measure to safeguard the security of the industry chain and strategic initiative.

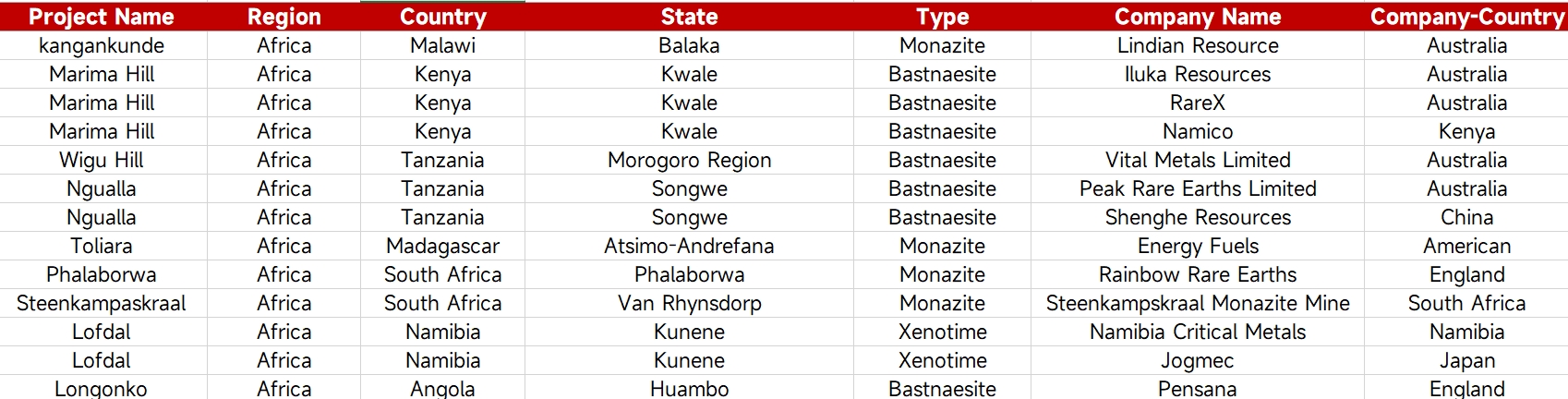

From the perspective of overseas mine deployment, among the 30 projects in non-Asian regions, South America (9 projects) and Africa (10 projects) are rich in resources but lack local enterprise leadership due to economic weaknesses inherited from colonial history and the high barriers to rare earth mining (radioactive treatment, investments exceeding $1 billion per single project, and a 5-8 year payback period). Mining development has long relied on Western capital. In contrast, the US and Australia have been more proactive: the US is building domestic capacity through the Mountain Pass mine (operated by MP Materials) and the Round Top mine, while Lynas' Malaysian plant in Australia, though capable of separating heavy rare earths, still has expansion plans pending implementation. At the capital level, MP Materials has entered the top 50 global mining companies, thanks to a $400 million equity investment and a guaranteed purchase agreement from the US Department of Defense, ranking alongside China Northern Rare Earth in market performance, reflecting the Western consensus on the strategic value of rare earths.

The essence of the rare earth game has transcended resource competition, becoming the core arena for major powers to vie for technological and industrial security. The "Australian ore - Malaysian processing - US and Japanese application" chain led by the US, though intended to divert China's influence, still awaits practical validation: While the EU has promoted the Critical Raw Materials Act to limit dependence on China (setting a 65% import cap), it has had to accept China's targeted exports to countries like Germany and Vietnam due to a lack of smelting technology. For China, the core strategic significance of focusing on overseas rare earths lies in three dimensions: First, **technological early warning** - monitoring innovations such as Lynas' separation process and Apple's recycling technology to guard against disruptive alternatives like rare earth-free motors; Second, **intervention in the pricing mechanism** - closely monitoring overseas price trends and guiding adjustments in domestic prices through various means; Third, **building supply chain resilience** - constructing a buffer system of "domestic reserves + overseas bases" by acquiring overseas resources such as the Ngualla mine in Tanzania (with reserves of 887,000 mt and a 15% proportion of dysprosium and terbium) to ensure stable supply for domestic customers (such as robotics and wind power industries) during emergencies.

China's scrutiny of overseas rare earths is, in fact, a defensive layout to optimize its own industry chain from a global perspective - avoiding over-stimulating the West to accelerate technological breakthroughs while consolidating its irreplaceability through resource control and technological positioning, ultimately shifting the focus of the game from "resource possession" to the ultimate battlefield of "technological sovereignty."