- SMM Cold-rolled Production Schedule: Cold-rolled production schedule of steel mills in August reversed the decline and turned to an increase

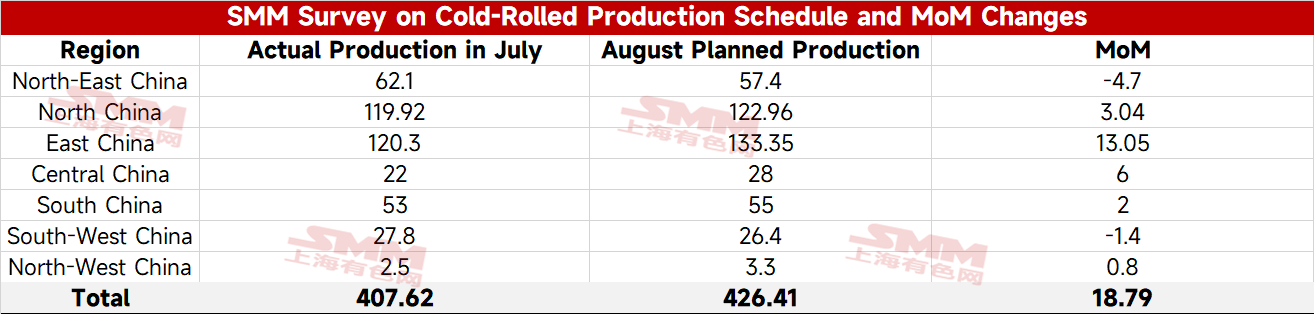

According to the latest tracking by SMM, the planned production volume of cold-rolled commercial materials for August from 31 mainstream steel mills producing cold-rolled sheets and coils totaled 4.2641 million mt, an increase of 187,900 mt compared to the actual production volume of cold-rolled commercial materials MoM, representing a growth rate of 4.61%.

- SMM HRC Production Schedule: The HRC production schedule for August increased by only 0.5% MoM

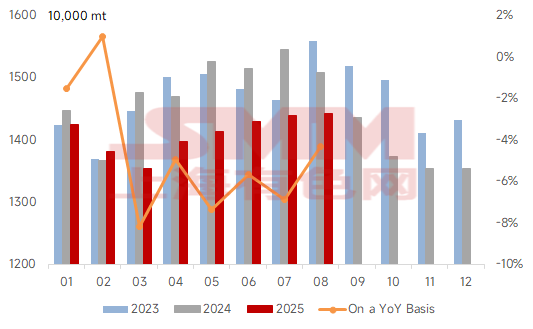

According to the latest tracking by SMM, the planned production volume of HRC commodity materials for August from 39 mainstream steel mills producing HRC totaled 14.4211 million mt, up 70,500 mt from the actual production volume of HRC commodity materials in the previous month, representing a 0.5% increase. On a daily average basis, the planned production volume of HRC commodity materials for August was 465,200 mt/day.

In August, some steel mills in north-east China, north China, south-west China, and south China initiated a new round of maintenance cycles, which, to a certain extent, affected the production release of HRC. Additionally, some steel mills in east China and central China reported that recent orders for cold-rolled products were slightly better than those for hot-rolled products, leading to a shift in production from hot-rolled to cold-rolled products. Under these combined influences, despite high profits, the total production schedule for hot-rolled coils at steel mills in August only increased slightly MoM from the previous month.

In terms of maintenance, the impact from hot-rolled maintenance in August is temporarily 780,600 mt, an increase of 509,800 mt MoM from the previous month. The announced maintenance is mainly concentrated in steel mills in north-east China, north China, southwest China, and south China. SMM will continue to monitor the subsequent situation.

Summary: In August, the planned daily average production of hot-rolled coil (HRC) by domestic steel mills increased slightly MoM compared to the actual production in the previous month, but the increase was lower than previously expected. This was mainly due to some regional steel mills starting a new round of maintenance cycles, as well as some steel mills reducing HRC production and increasing cold-rolled production schedules.

Looking ahead, in terms of supply, the production schedule for HRC by steel mills in August will remain basically stable MoM. On the demand side, amid the off-season and frequent high-temperature and rainy weather, the overall demand for steel is under pressure. However, the demand from downstream manufacturing industries for HRC is expected to maintain strong resilience. SMM expects that the accumulation of HRC inventory in August will be limited, and the fundamental contradictions will have a relatively small drag on prices.

In addition, in terms of news, in the mid-to-late August, the intensity and frequency of disruptions caused by the news of "production restrictions for the military parade" will both increase. Given the low fundamental contradictions and the "strong expectations" of supply reductions brought about by production restrictions, the HRC price in August will form a fluctuating trend at highs, with a more likely to rise than fall situation. Attention should be paid to the substantive policies on production restrictions for the military parade in the mid-to-late August. If the policies fall short of expectations, there will be a risk of a high-level price correction.

![[SMM Daily Chromium Review] Futures Rose While the Spot Market Remained Temporarily Stable, with Limited Adjustment in the Ferrochrome Market](https://imgqn.smm.cn/usercenter/rBCZR20251217171716.jpg)