New Capacity Additions of Secondary Aluminum by Region and Product from January to June, 2025 (10,000 mt)

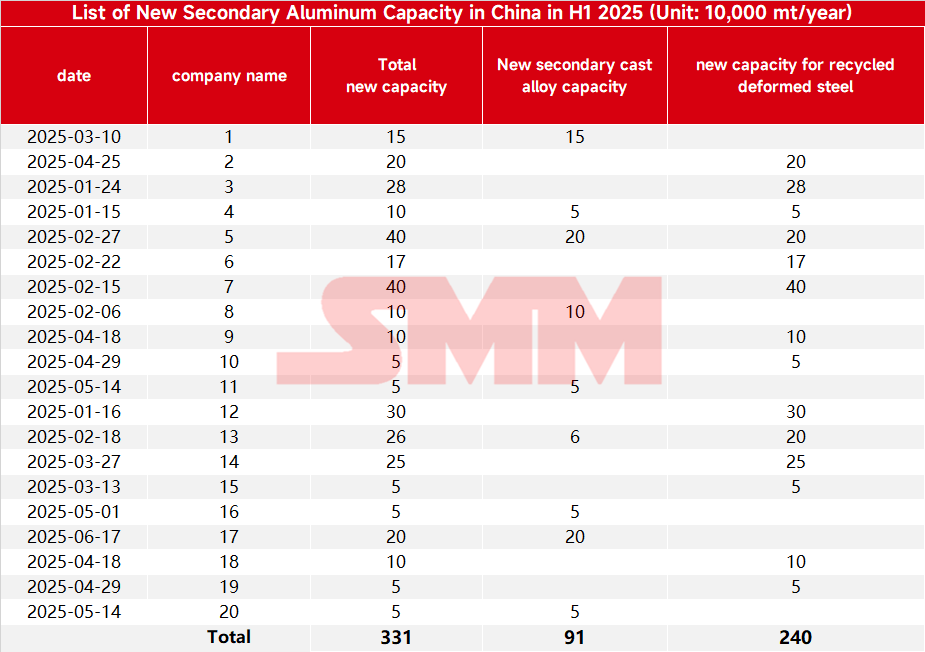

According to SMM statistics, from January to June 2025, there were 20 new secondary aluminum projects launched domestically, with a total new capacity of 3.31 million mt, showing a significant YoY increase. The layout was relatively concentrated in regions such as Guangxi, Chongqing, and Jiangsu. However, from the perspective of project status, most current projects are in the environmental assessment or new construction phase, with limited actual new capacity put into operation. It is expected that with the gradual completion and commissioning of projects, the subsequent supply in the secondary aluminum market will increase significantly, highlighting the pattern of active expansion and accelerated development of the domestic secondary aluminum industry.

From the perspective of product structure, in the first half of the year, the new capacity of secondary cast aluminum alloy was approximately 910,000 mt, and the new capacity of secondary wrought aluminum alloy was approximately 2.4 million mt. In recent years, due to the prominent overcapacity issue of secondary cast aluminum alloy, the industry's operating rate has hovered around 50% for a long time. Fierce competition has continued to compress corporate profits, leading to a slowdown in the pace of capacity expansion. In contrast, secondary wrought aluminum alloy has developed rapidly, mainly because enterprises are actively expanding the application scenarios of secondary aluminum to achieve carbon reduction and cost reduction goals. By leveraging its recycling advantages, they reduce raw material costs and carbon emissions, thereby driving the rapid expansion of the industry.