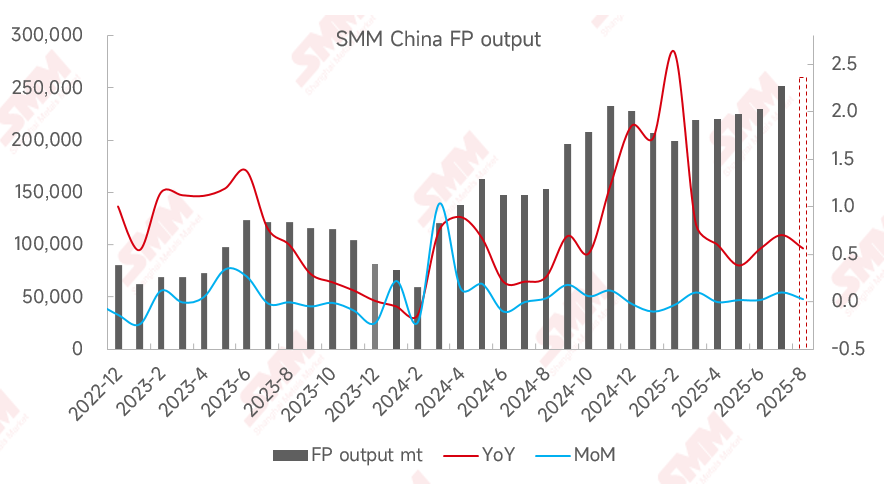

In July, domestic iron phosphate production increased by 10% MoM and surged by 70% YoY.

On the supply side, iron phosphate enterprises saw a notable increase in production in July: on the one hand, integrated enterprises experienced significant growth in their corresponding iron phosphate production; on the other hand, the expansion of production capacity by some enterprises drove up production. However, the concentrated release of new capacity also squeezed the shipments of existing iron phosphate enterprises, leading to some enterprises' shipments falling short of expectations.

On the demand side, downstream demand for LFP saw significant growth in July, with enterprises preferring to purchase high-value iron phosphate with lower prices and superior quality. The market's price expectations for iron phosphate weakened, but the requirements for product quality continued to rise.

On the cost side, industrial-grade MAP was in the off-season for consumption in July, with prices pulling back significantly compared to June; the price of ferrous sulphate, however, continued to rise, significantly increasing the cost pressure on iron phosphate enterprises for iron sources.

In August, with the continuous release of new capacity, iron phosphate production is expected to continue growing, with an anticipated increase of 3% MoM and 56% YoY.