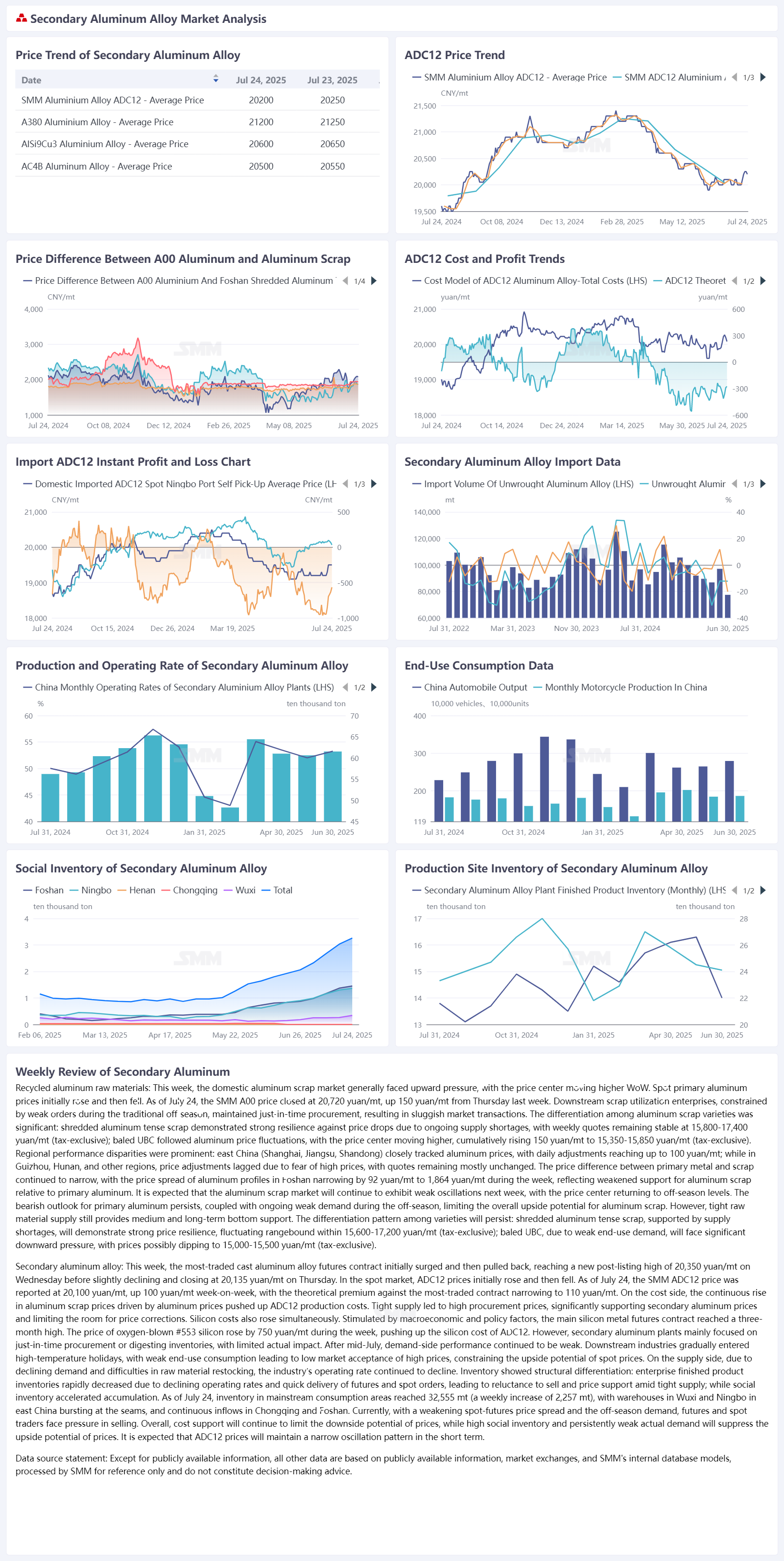

เศษอลูมิเนียม: สัปดาห์นี้ ตลาดเศษอลูมิเนียมภายในประเทศโดยทั่วไปต้องเผชิญกับแรงกดดันในการปรับตัวขึ้น ราคาเฉลี่ยมีการปรับตัวสูงขึ้นเมื่อเทียบกับสัปดาห์ก่อนหน้า ราคาอลูมิเนียมหลักในตลาดสปอตปรับตัวสูงขึ้นก่อนแล้วปรับตัวลงในภายหลัง ณ วันที่ 24 กรกฎาคม ราคา SMM A00 ปิดที่ 20,720 หยวน/ตัน เพิ่มขึ้น 150 หยวน/ตัน เมื่อเทียบกับวันพฤหัสบดีของสัปดาห์ก่อนหน้า ผู้ประกอบการใช้เศษอลูมิเนียมในภาคล่างของอุตสาหกรรม ซึ่งถูกจำกัดด้วยคำสั่งซื้อที่อ่อนแอในช่วงฤดูอ่อนแอตามปกติ ยังคงซื้อวัสดุตามความต้องการจริงเท่านั้น ส่งผลให้การซื้อขายในตลาดซบเซา มีความแตกต่างกันอย่างมากระหว่างประเภทของเศษอลูมิเนียม: เศษอลูมิเนียมที่บดแล้วมีความยืดหยุ่นสูงต่อการปรับตัวลงของราคาเนื่องจากการขาดแคลนในการจัดหาอย่างต่อเนื่อง โดยราคาประจำสัปดาห์ยังคงทรงตัวที่ 15,800-17,400 หยวน/ตัน (ไม่รวมภาษี) เศษอลูมิเนียมบดแล้วที่บรรจุเป็นก้อนติดตามการเปลี่ยนแปลงของราคาอลูมิเนียม ราคาเฉลี่ยมีการปรับตัวสูงขึ้น ปรับตัวสูงขึ้นรวม 150 หยวน/ตัน เป็น 15,350-15,850 หยวน/ตัน (ไม่รวมภาษี) ความแตกต่างในการดำเนินงานระหว่างภูมิภาคมีความเด่นชัด: ภาคตะวันออกของจีน (เซี่ยงไฮ้ เจียงซู ซานตง) ติดตามราคาอลูมิเนียมอย่างใกล้ชิด โดยมีการปรับราคาประจำวันสูงถึง 100 หยวน/ตัน ในขณะที่ในกุ้ยโจว หูหนาน และสถานที่อื่นๆ การปรับราคาล่าช้าเนื่องจากความกลัวราคาสูง โดยราคาส่วนใหญ่ยังคงทรงตัว ความแตกต่างในราคาระหว่างโลหะหลักและเศษอลูมิเนียมยังคงลดลงต่อเนื่อง โดยมีการปรับตัวลดลงของสเปรดราคาอลูมิเนียมโปรไฟล์ในเมืองฝอซาน 92 หยวน/ตัน เป็น 1,864 หยวน/ตัน ในช่วงสัปดาห์นี้ สะท้อนให้เห็นถึงการสนับสนุนที่อ่อนแอลงของเศษอลูมิเนียมเมื่อเทียบกับอลูมิเนียมหลัก คาดว่าตลาดเศษอลูมิเนียมจะยังคงอยู่ในรูปแบบการแกว่งตัวที่อ่อนแอในสัปดาห์หน้า โดยราคาเฉลี่ยจะกลับไปอยู่ในระดับของฤดูอ่อนแอ ทัศนะในเชิงลบสำหรับอลูมิเนียมหลักยังไม่ได้หายไป รวมกับการถูกกดดันอย่างต่อเนื่องจากความต้องการในฤดูอ่อนแอที่อ่อนแอ จำกัดศักยภาพในการปรับตัวสูงขึ้นโดยรวมของเศษอลูมิเนียม อย่างไรก็ตาม การขาดแคลนในการจัดหาวัตถุดิบยังคงให้การสนับสนุนในระดับปานกลางและระยะยาว รูปแบบการแตกต่างระหว่างประเภทจะดำเนินต่อไป: เศษอลูมิเนียมที่บดแล้วมีความยืดหยุ่นสูงต่อราคาเนื่องจากการขาดแคลนในการจัดหา จะแสดงให้เห็นถึงความยืดหยุ่นในราคาที่แข็งแกร่ง โดยมีการแกว่งตัวอยู่ในช่วง 15,600-17,200 หยวน/ตัน (ไม่รวมภาษี) เศษอลูมิเนียมบดแล้วที่บรรจุเป็นก้อน เนื่องจากความต้องการในการใช้งานปลายทางที่อ่อนแอ จะเผชิญกับแรงกดดันในการปรับตัวลงอย่างมาก โดยราคาอาจลดลงถึง 15,000-15,500 หยวน/ตัน (ไม่รวมภาษี)

อลูมิเนียมอัลลอยด์รีไซเคิล: สัปดาห์นี้ สัญญาซื้อขายล่วงหน้าอลูมิเนียมอัลลอยด์หล่อที่ซื้อขายมากที่สุด มีการพุ่งขึ้นก่อนแล้วลดลงเล็กน้อย โดยทำสถิติสูงสุดหลังจากเปิดตลาดที่ 20,350 หยวน/ตัน ในวันพุธ ก่อนจะลดลงเล็กน้อย และปิดตลาดที่ 20,135 หยวน/ตัน ในวันพฤหัสบดี ในตลาดสปอต ราคา ADC12 เพิ่มขึ้นก่อนแล้วลดลง ณ วันที่ 24 กรกฎาคม ราคา SMM ADC12 รายงานที่ 20,100 หยวน/ตัน เพิ่มขึ้น 100 หยวน/ตัน เมื่อเทียบกับสัปดาห์ก่อน โดยมีเบี้ยปรับทางทฤษฎีเมื่อเทียบกับสัญญาซื้อขายล่วงหน้าที่ซื้อขายมากที่สุดลดลงเหลือ 110 หยวน/ตัน ในด้านต้นทุน การเพิ่มขึ้นอย่างต่อเนื่องของราคาอลูมิเนียมได้ผลักดันให้ต้นทุนการผลิตของ ADC12 เพิ่มขึ้น เนื่องจากราคาอลูมิเนียมรีไซเคิลเพิ่มขึ้น การจัดหาที่ตึงตัวทำให้ราคาซื้อสูง ซึ่งสนับสนุนราคาอลูมิเนียมรีไซเคิลอย่างมากและจำกัดพื้นที่ในการปรับราคาลง ราคาซิลิคอนก็เพิ่มขึ้นเช่นกัน ในเวลาเดียวกัน ได้รับการกระตุ้นจากปัจจัยทางเศรษฐกิจและนโยบาย สัญญาหลักของซิลิคอนเมทัลฟิวเจอร์สทำสถิติสูงสุดในรอบสามเดือน ราคาซิลิคอนออกซิเจน #553 เพิ่มขึ้น 750 หยวน/ตัน เมื่อเทียบกับสัปดาห์ก่อน ผลักดันให้ต้นทุนซิลิคอนของ ADC12 เพิ่มขึ้น อย่างไรก็ตาม โรงงานอลูมิเนียมรีไซเคิลส่วนใหญ่เน้นการจัดซื้อแบบจัสต์อินไทม์หรือการย่อยสลายสินค้าคงคลัง ทำให้ผลกระทบจริงมีจำกัด หลังจากกลางเดือนกรกฎาคม ผลการดำเนินงานของฝ่ายความต้องการยังคงอ่อนแอ ภาคอุตสาหกรรมต่อเนื่องได้เข้าสู่ช่วงวันหยุดฤดูร้อนที่มีอุณหภูมิสูง และการบริโภคในปลายทางที่อ่อนแอทำให้ตลาดยอมรับราคาสูงได้ต่ำ จำกัดศักยภาพในการปรับราคาขึ้นของราคาสปอต ในด้านการจัดหา เนื่องจากความต้องการลดลงและความยากลำบากในการจัดหาวัตถุดิบ อัตราการดำเนินงานของอุตสาหกรรมยังคงลดลง สินค้าคงคลังแสดงให้เห็นถึงความแตกต่างเชิงโครงสร้าง: สินค้าคงคลังผลิตภัณฑ์สำเร็จรูปขององค์กรลดลงอย่างรวดเร็วเนื่องจากอัตราการดำเนินงานลดลงและการส่งมอบคำสั่งซื้อฟิวเจอร์สและสปอตอย่างรวดเร็ว ทำให้ไม่เต็มใจที่จะปรับราคาลงในช่วงที่การจัดหาตึงตัว ในขณะที่สินค้าคงคลังทางสังคมเร่งการสะสมขึ้น ทำให้ถึง 32,555 ตัน (เพิ่มขึ้น 2,257 ตันในสัปดาห์) ในพื้นที่บริโภคหลักเมื่อวันที่ 24 กรกฎาคม คลังสินค้าในเมืองอู่ซีและหนิงโปทางตะวันออกของจีนเต็มไปด้วยสินค้า และมีการไหลเข้าอย่างต่อเนื่องในเมืองฉงชิ่งและเฟิ่งหั่น การอ่อนแอลงของสเปรดราคาสปอต-ฟิวเจอร์สในปัจจุบัน ร่วมกับความต้องการในช่วงนอกฤดู ทำให้ผู้ซื้อขายฟิวเจอร์สและสปอตมีแรงกดดันในการขาย โดยรวมแล้ว การสนับสนุนต้นทุนจะยังคงจำกัดศักยภาพในการปรับราคาลง ในขณะที่สินค้าคงคลังทางสังคมที่สูงและความต้องการจริงที่อ่อนแออย่างต่อเนื่องจะยับยั้งศักยภาพในการปรับราคาขึ้นของราคาคาดว่าราคา ADC12 จะคงรูปแบบการแกว่งตัวในช่วงเวลาสั้น ๆ