[SMM Analysis] High volatility in the futures market drives improvement in spot transactions; Ningbo HRC inventory continues to decline

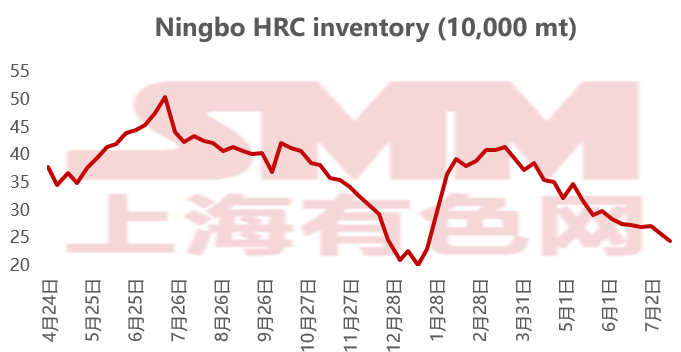

According to the SMM survey, the large-caliber inventory of SMM Ningbo HRC this week was 245,400 mt (as of July 16), a decrease of 11,100 mt WoW.

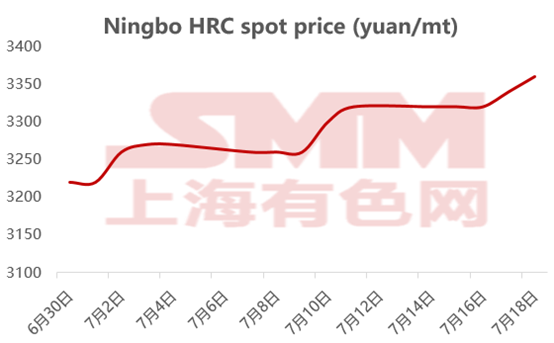

This week, HRC prices fluctuated upward, with spot prices rising by 40-60 yuan/mt on a weekly basis. The futures market surged too rapidly, with spot prices and the intensity of end-use demand release remaining at a moderate level, and overall transactions were relatively stable. As of the afternoon close on July 18, the most-traded HRC 2510 futures contract closed at 3,310 yuan/mt.

Meanwhile, according to the SMM survey, in the Ningbo spot trading market this week, in terms of prices, the transaction prices of mainstream HRC resources continued to rise. As of the afternoon of July 18, the spot quotes at the end of the trading day were 3,350-3,360 yuan/mt, up 40 yuan/mt from 3,320 yuan/mt last Friday. In terms of transactions, although the futures market surged significantly, the spot market's price increase was slower, and it was difficult to sell at high prices. However, most traders still held bullish expectations for the market, refusing to budge on prices, and overall transactions during the week were average. In terms of inventory, Ningbo HRC inventory continued to decline this week. According to the current SMM survey, the willingness of market terminals to purchase remains low, with the market dominated by speculative demand. The demand for low-alloy HRC remains at a relatively low level. However, considering that the recent momentum in the futures market remains strong and the supply of Ningbo HRC is at a relatively low level, if the DDH supply does not arrive next week, it is expected that there will still be a slight inventory destocking in Ningbo next week.

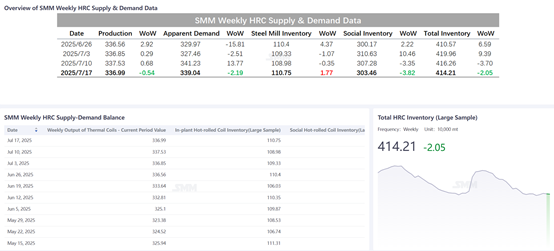

This week, SMM released the weekly balance data for HRC, showing a narrow decline in HRC production, continued inventory destocking, and a slight rebound in apparent demand. According to the current SMM statistics, the social inventory of HRC in 86 warehouses (large sample) nationwide was 3.0346 million mt, a decrease of 38,200 mt WoW, or -1.24% WoW, and -31.96% YoY. By region, except for slight inventory buildup in the north-east and north China regions, inventory in east, south, and central China regions was all destocking.

![[SMM Daily Chromium Review] Futures Rose While the Spot Market Remained Temporarily Stable, with Limited Adjustment in the Ferrochrome Market](https://imgqn.smm.cn/usercenter/rBCZR20251217171716.jpg)

![[SMM Iron & Steel] Hoa Phat Boosts Green Energy at Dung Quat Steel Complex](https://imgqn.smm.cn/usercenter/LSkpO20251217171720.jpg)