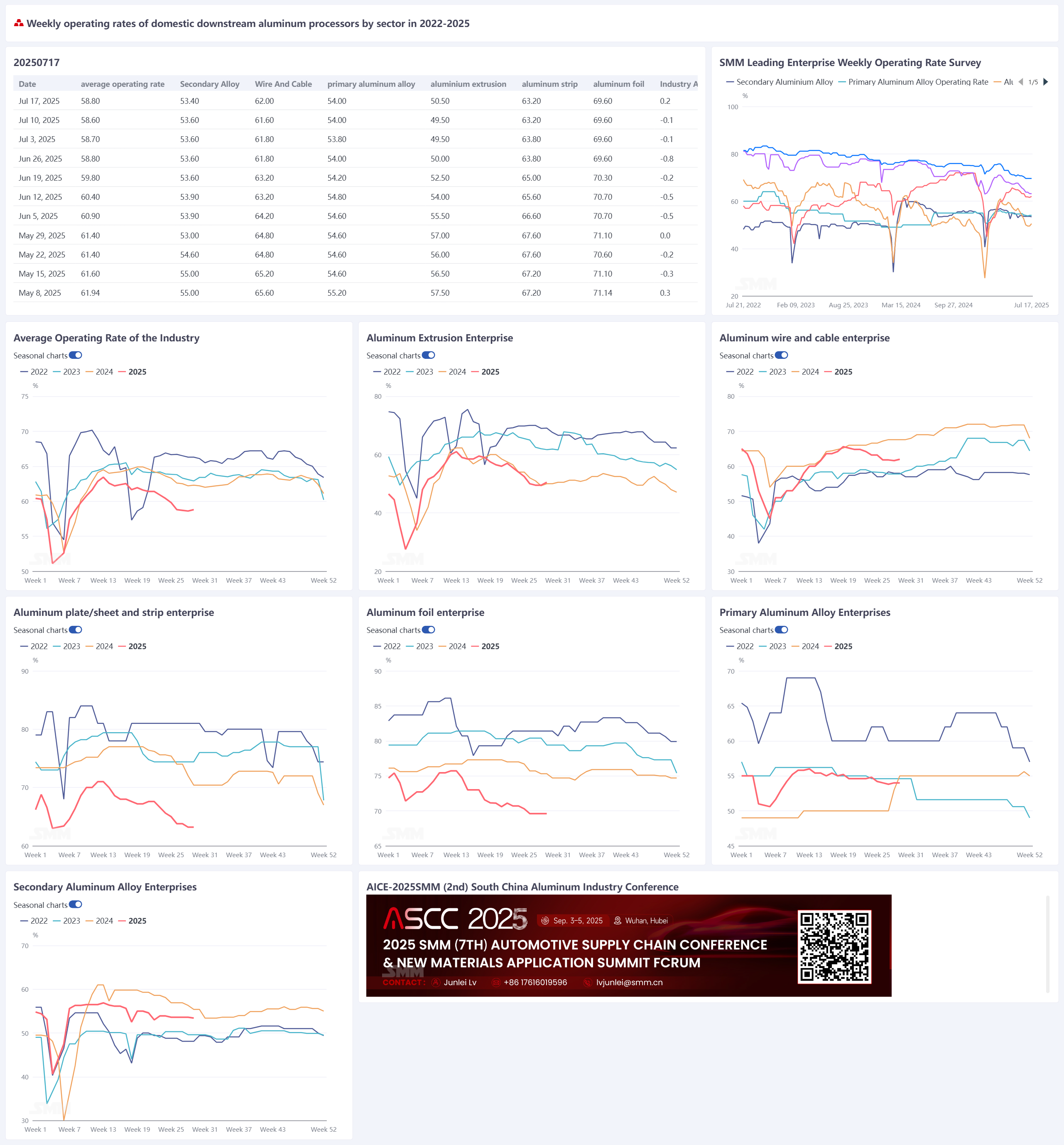

Currently, the downstream sector as a whole is under the shadow of the off-season atmosphere. The operating rate of the secondary alloy sector continues to decline. However, due to the pullback in the center of aluminum prices, there is differentiation among different sectors. The weekly operating rates of aluminum extrusion and aluminum wire and cable have slightly rebounded, driving marginal improvements in the industry's operating rate. The operating rate of the aluminum processing industry rose by 0.2 percentage points WoW to 58.8%. By sector:

- Primary alloy sector: Under the requirement for liquid aluminum alloying, surplus liquid aluminum is redirected to the production of primary aluminum alloy with relatively stable domestic demand, providing structural support for its operating rate. However, in the short term, the industry maintains a game of "liquid aluminum allocation dominance and aluminum price suppression of demand," with the operating rate in a doldrums.

- Aluminum plate/sheet and strip sector: During the week, the enthusiasm of downstream customers for cargo pick-up in the aluminum plate/sheet and strip sector slightly increased, alleviating the pressure on finished product inventories in the factory area. However, due to the continuous weakness of orders, the operating rate has still not improved.

- Aluminum wire and cable sector: During the week, enterprises released some just-in-time procurement of raw materials, and the operating rate slightly improved due to the influence of prices. However, in the short term, the off-season atmosphere remains strong, and order matching is still not in place.

- Aluminum extrusion sector: The off-season for aluminum extrusion remains obvious. Although some enterprises have received new orders for NEV extrusions, the construction materials sector continues to operate weakly. The operating rate of enterprises has slightly eased but is still not optimistic.

- Aluminum foil sector: During the traditional consumption off-season of July-August, there is no hope for a recovery in end-use demand. It is expected that the operating rate of the aluminum foil industry will continue to decline in the short term.

- Secondary aluminum alloy sector: Affected by the traditional off-season, the demand side remains sluggish. Downstream orders have decreased, and most enterprises maintain just-in-time procurement. Subject to the dual constraints of raw materials and orders, the industry's operating rate will still be under pressure in the short term. SMM expects that the weekly operating rate of downstream aluminum processing will decline by 0.1 percentage points next week to 58.7%.

Primary alloy: This week, the operating rate of the primary aluminum alloy industry was recorded at 54.0%, showing an improvement from the previous doldrums in mid-July. Despite being in the traditional off-season, under the requirement for liquid aluminum alloying, surplus liquid aluminum is redirected to the production of primary aluminum alloy with relatively stable domestic demand, providing structural support for its operating rate. In the short term, the industry maintains a game of "liquid aluminum allocation dominance and aluminum price suppression of demand," with the operating rate possibly remaining in a doldrums. In H2, under the triple pressures of weak demand in the traditional off-season, negative feedback from high aluminum prices, and tariff uncertainty, the doldrums in the primary aluminum alloy and aluminum wheel hub industries are difficult to break. The latter's exports may enter a period of deep adjustment, and a substantive recovery will require clearer policies and a reduction in cost pressure. Aluminum Plate/Sheet and Strip: This week, the operating rate of leading enterprises in the aluminum plate/sheet and strip sector stood at 63.2%. On Monday, aluminum prices cooled rapidly, with the price center moving downward, followed by a period of narrow fluctuations and adjustments throughout the week. Consequently, the enthusiasm of downstream customers for picking up goods from aluminum plate/sheet and strip manufacturers rebounded, alleviating some inventory pressure on finished products in the factory areas. However, due to the persistent weakness in orders, there was no significant improvement in operating rates. On the other hand, amid the ongoing high-temperature weather, although no actual feedback on power rationing due to high temperature and production cuts from aluminum plate/sheet and strip enterprises across various regions has been received yet, this is attributed to the fact that most aluminum plate/sheet and strip production lines are generally not operating at full capacity during the off-season, and industrial power consumption has not yet reached full load. As we enter the mid-to-late July, the probability of demand improving and subsequently driving up operating rates is extremely low. The industry's operating rate is expected to continue to be generally stable with a slight fall. In the subsequent transition period from the off-season to the peak season in August, assuming aluminum prices remain relatively stable, downstream customers' stockpiling actions for the peak season may bring about a wave of demand recovery.

Aluminum Wire and Cable: This week, the operating rate of leading enterprises in the aluminum wire and cable sector stood at 62%, increasing by 0.4 percentage points WoW, indicating signs of the industry's operating rate hitting bottom and recovering. From a short-term perspective, enterprises' current orders are still mainly centered around power grid and new energy orders. Despite enterprises having a backlog of power grid orders, order matching for July has not yet been completed. Coupled with the impact of high-temperature weather, production scheduling is not fully utilized. However, the significant downward shift in the aluminum price center during the week has slightly stimulated enterprises' willingness to operate, and some rigid demand for raw material inventories has also been released. Regarding power grid orders, the first batch of tender results for main network line materials of China Southern Power Grid was announced in the past week, with approximately 2 billion yuan in orders secured, providing order support for enterprise operations in H2 and the next year. Simultaneously, sporadic distribution network orders have also been secured, and orders on hand for top-tier enterprises continue to increase. Therefore, from a long-term perspective, in the final year of the "14th Five-Year Plan," supervision over power grid construction remains urgent. Coupled with the relatively abundant backlog of orders for enterprises, it is expected that there will still be a concentrated delivery window period in H2, driving up the operation of aluminum wire and cable and aluminum consumption. In the short term, there has still been no significant turning point in order matching, and the operating rate of aluminum wire and cable in July is expected to remain mainly within a certain range. It is anticipated that the turning point in operating rates may appear in August.

Aluminum Extrusion: This week, the operating rate of China's aluminum extrusion industry increased by 1 percentage point MoM to 50.5%. The slight increase in the comprehensive operating rate of sampled enterprises this week was mainly due to new automotive extrusion orders received by some enterprises. In terms of sub-sectors, for industrial extrusion, the weekly sample operating rate increased slightly compared to the previous week. According to SMM surveys, some industrial extrusion enterprises reported receiving new automotive material orders, driving up their operating levels. For PV extrusion, sampled enterprises reported a downward trend in order volumes, coupled with a further decline in processing fees, compressing enterprises' profitability and leading to a slight fall in operating rates. Relevant enterprises are actively seeking transformation. Additionally, some PV extrusion enterprises stated that the "volume discount" model is not a long-term solution. They still remain optimistic about the healthy and long-term development of the PV extrusion industry and anticipate that the industry can return to a track of benign competition. For building material extrusion, the overall operating rate of sampled enterprises declined slightly compared to the previous week, and currently, they can only maintain the production rhythm of orders on hand. Despite the narrowing decline in real estate completions in June, enterprises generally reported that the transmission effect of this positive signal was not significant, and the operating situation of building material extrusion remained weak. SMM will continue to monitor the actual progress of order implementation in various fields.

Aluminum Foil: This week, the operating rate of leading enterprises in the aluminum foil sector stood at 69.6%. The overall demand in the aluminum foil market remained weak during the week, with the industry's operating rate running at a low level. In terms of product categories, the demand for double zero foils such as household foil, container foil, and pouch foil in July contracted by 5-10% YoY, with the downtrend persisting. Processing fees temporarily halted their decline, with the price of conventional double zero 6 foils operating around 5,800-6,200 yuan/mt, with no short-term possibility of an increase, but also operating close to the cost line. The "volume discount" strategy has gradually lost its effectiveness. During the traditional consumption off-season in July-August, there is no hope for a recovery in end-use demand. It is expected that the operating rate of the aluminum foil industry will continue to decline in the short term.

Secondary Aluminum Alloy: This week, the operating rate of leading enterprises in the secondary aluminum alloy sector decreased slightly by 0.2% WoW to 53.4%, mainly constrained by raw material shortages and demand reductions. Market feedback this week indicated that the difficulty in purchasing aluminum scrap remained high. Although prices decreased slightly during the week, they still remained at a high level. The industry's theoretical losses persisted, and insufficient restocking by enterprises led to a decrease in raw material inventories, also dragging down the operating rates of some enterprises. With half of July passed, the demand side remained sluggish due to the traditional off-season, with downstream orders decreasing and mostly maintaining just-in-time procurement. Constrained by both raw materials and orders, it is expected that the industry's operating rate will continue to be under pressure in the short term.