[SMM Hot Topic] Intensifying Overseas Trade Frictions: Is Steel Export Volume Starting to Pull Back?

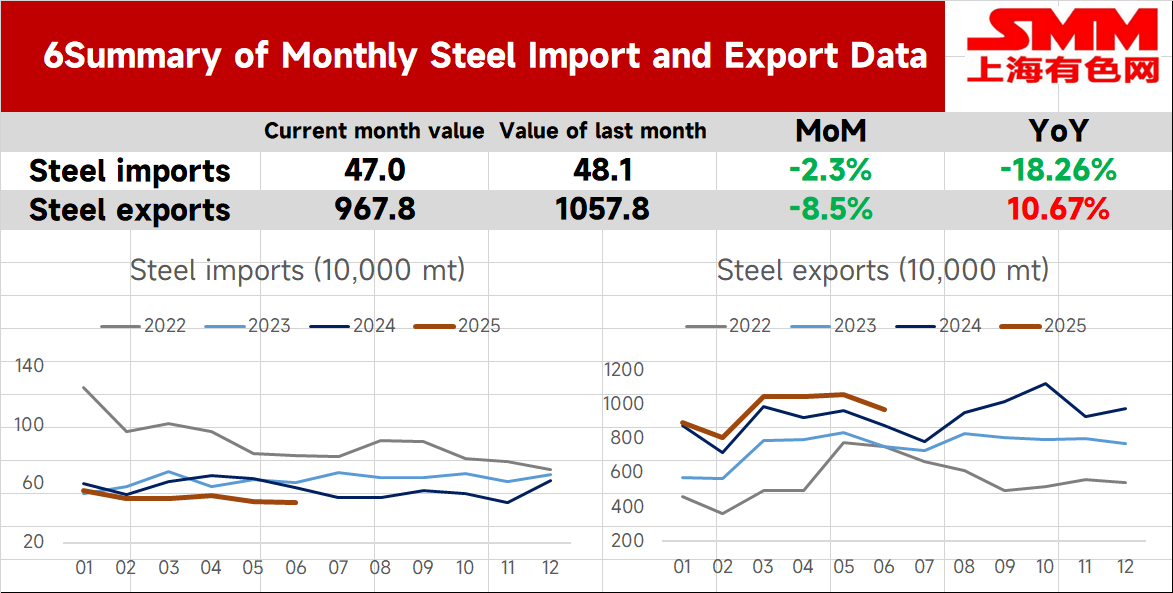

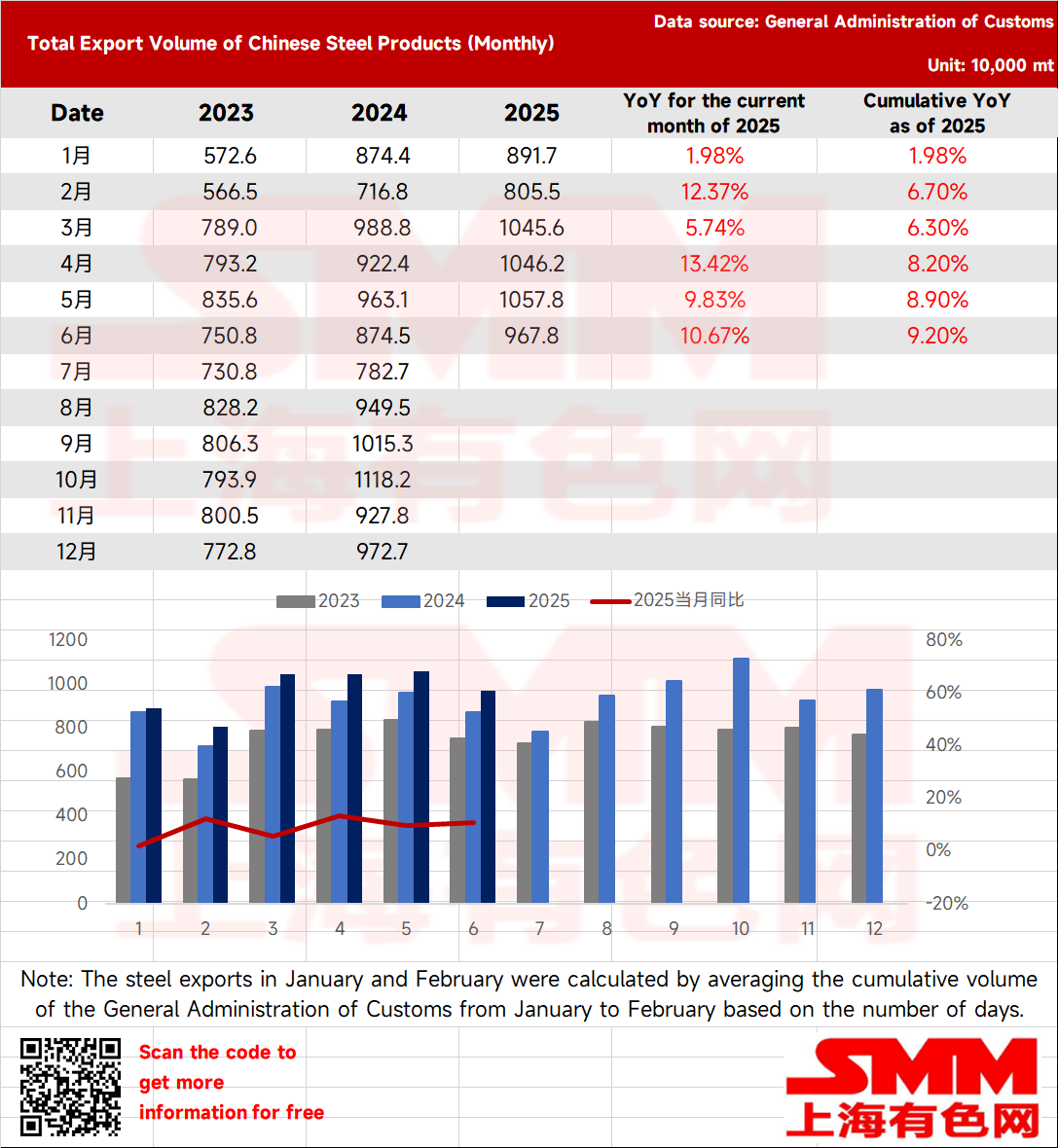

On July 14, data from the General Administration of Customs showed that China exported 9.678 million mt of steel in June 2025, a decrease of 900,000 mt MoM, down 8.5% MoM. From January to June, cumulative steel exports reached 58.147 million mt, up 9.2% YoY.

In June, China imported 470,000 mt of steel, a decrease of 11,000 mt MoM, down 2.3% MoM. From January to June, cumulative steel imports reached 3.023 million mt, down 16.4% YoY.

Overview of Steel Import and Export Data in June

- China's Steel Exports Fall Below 10 Million mt Level

In June, China's total steel exports fell 8.5% MoM. On June 3, Brazil initiated an anti-dumping investigation into HRC originating from China. Meanwhile, US President Trump announced an increase in tariffs on imported steel and aluminum and their derivative products from 25% to 50%, effective from June 4. With ongoing intensification of international trade frictions, although domestic traders are still engaging in volume discounts to secure transactions, as global seasonal demand weakens, overall order volumes are also pulling back.

- China's Steel Imports Decline Slightly MoM in June

In June, China imported 470,000 mt of steel, a decrease of 11,000 mt MoM, down 2.3% MoM. From January to June, cumulative steel imports reached 3.023 million mt, down 16.4% YoY. Net steel exports stood at 45.916 million mt.

- Short-Term Outlook for Steel Exports

According to data released by the China Federation of Logistics and Purchasing, the global manufacturing PMI in June 2025 was 49.5%, up 0.3 percentage points MoM, rising for two consecutive months MoM, but still below 50%. Global manufacturing remains in contraction territory, but the continuous slight increase in the index suggests a strengthening in the global manufacturing recovery. During the suspension period of the US tariff hike policy, countries around the world have a strong willingness to accelerate economic recovery. According to China's manufacturing PMI data, the new export orders index in June was 47.7%, up 0.2 percentage points MoM, rising for two consecutive months.

Monitoring data from the World Steel Association showed that in May 2025, global crude steel production from 70 countries included in the World Steel Association's statistics was 158.8 million mt, down 3.8% YoY. China's crude steel production was 86.55 million mt, down 6.9% YoY, while production in the rest of the world (excluding China) was 69.7 million mt, up 0.37% YoY.

As of July 14, 2025, export offers (FOB) for HRC from India, Turkey, and the CIS were $550/mt, $535/mt, and $455/mt respectively, while China's HRC export offer (FOB) was $464/mt. Currently, the price spreads between China's HRC export offers and those of other countries are $86/mt, $71/mt, and -$9/mt. After recent domestic price hikes driven by multiple positive news, domestic and international trade prices have risen significantly. However, as the overseas off-season deepens, downstream consumption remains weak, and some traders report difficulties in moving goods at higher prices. Therefore, prices are fluctuating rangebound, and the price spreads between China's HRC export offers and those of other countries have narrowed.

According to the latest SMM survey on steel mills' export order schedules, under the export task of maintaining volume, the planned HRC export volume for July is expected to increase slightly MoM compared to the actual export volume in June. However, with the contraction of domestic and international price spreads, China's steel export price advantage has weakened. Coupled with the weakening of global demand, domestic order-taking pressure has increased. Therefore, SMM expects that the total steel export volume in July will continue to decline compared to June, but will still remain at a relatively high level YoY.

As July progresses, with the ongoing deepening of global trade frictions, the risks faced by China's steel exports continue to increase. On July 4, 2025, Vietnam's anti-dumping investigation into HRC from China also entered the final ruling stage from the preliminary ruling. Meanwhile, the Malaysian government has made a preliminary ruling to impose temporary anti-dumping duties on galvanized steel coils/sheets originating from or exported from China, South Korea, and Vietnam, with tariff rates ranging from 3.86% to 57.90%. Considering the escalation of the US's imposition of reciprocal tariffs globally, this will continue to exacerbate the crisis in domestic steel re-export trade.

According to SMM shipping data, as of June 31, the total port departures from Chinese ports in June were 11.5429 million mt, down 0.55% MoM from May, with a smaller decline compared to customs data, possibly mainly due to the still high volume of steel billet exports in June. Meanwhile, according to SMM surveys, recent export orders for HRC, steel billets, etc. have all pulled back. Although domestic prices have risen with the futures market, it is not easy to secure orders at higher export prices. The situation of export MD (missing delivery) remains rampant. Under the influence of malicious competition, it is difficult for traders to close deals. In summary, SMM expects that steel export volume in July will still maintain a relatively high growth level YoY, but will continue to decline MoM compared to June. On the basis of maintaining export volume, the decline is not expected to be overly pessimistic for the time being.

![[SMM Daily Chromium Review] Futures Rose While the Spot Market Remained Temporarily Stable, with Limited Adjustment in the Ferrochrome Market](https://imgqn.smm.cn/usercenter/rBCZR20251217171716.jpg)

![[SMM Iron & Steel] Hoa Phat Boosts Green Energy at Dung Quat Steel Complex](https://imgqn.smm.cn/usercenter/LSkpO20251217171720.jpg)