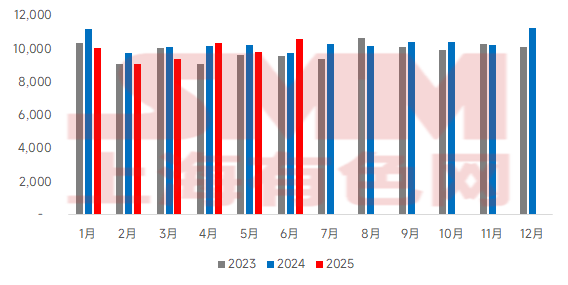

SMM, July 14, 2025: According to statistics from the General Administration of Customs of China, China imported 105.95 million mt of iron ore fines and concentrates in June, an increase of 7.817 million mt MoM, up 8% MoM, and up 8.54% YoY. The cumulative imports of iron ore fines and concentrates from January to June were 592.205 million mt, down 3% YoY.

The iron ore imports in June reached a new high for the year, mainly due to the following factors:

1) Seasonal rebound on the supply side. Major mines, such as BHP and Rio Tinto, had a need to push for shipment targets, and the average weekly shipment volume in June increased compared to May. Among non-mainstream mines, although shipments from non-mainstream mines in India, Peru, and Iran were constrained by policy and geopolitical factors, shipments from countries like Malaysia and Africa improved MoM, resulting in an overall increase.

2) Resilient demand support. Pig iron production remained stable at high levels: The daily average pig iron production of 242 steel mills in June consistently stayed above 2.4 million mt, with sustained rigid restocking demand.

Looking ahead to July, iron ore imports are expected to fall back from highs. Although the high shipment volume at the end of June will partially translate into arrivals in July, and domestic pig iron production remains high to support demand, coupled with one additional working day in July compared to June (31 days vs. 30 days), the overall imports in July are still expected to decline MoM from June due to the significant drop in shipments caused by concentrated maintenance at mines after the push for target at quarter-end. However, the absolute volume will still remain at a relatively high level.

Chart: China's Iron Ore Imports

Source: General Administration of Customs of China

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)