In June 2025, secondary lead production recovery fell short of expectations, with a 2.39% increase MoM and a 13.57% decrease YoY. Secondary refined lead production increased by 1.27% MoM and decreased by 17.97% YoY.

In May, high raw material costs coupled with weak downstream consumption led to a significant decline in secondary lead production. After entering June, the pressure on both procurement and sales ends did not improve significantly. The production enthusiasm of secondary lead smelters remained low, and the production resumption plans of some smelters that underwent maintenance in April-May were postponed, which became the main reason for the secondary lead production growth in June falling short of expectations. In addition, some manufacturers in east China were affected by environmental protection inspections, individual manufacturers in central China halted production due to sudden equipment failures, and new capacity in south-west China postponed commissioning due to problems discovered during equipment commissioning. These situations all limited the growth of secondary lead production in June.

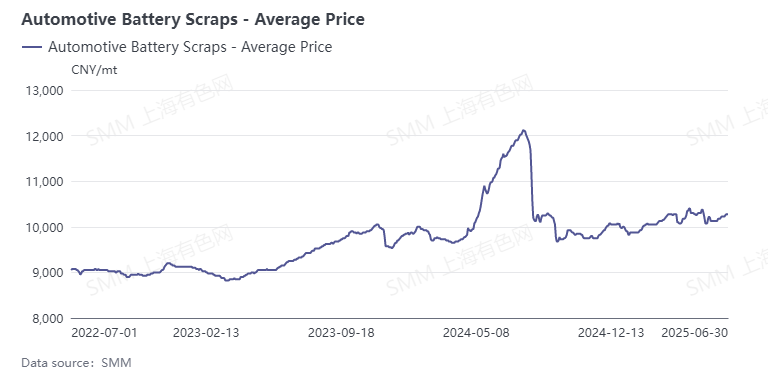

According to smelters, the current market supply of scrap batteries is scarce, and recyclers are hoarding them, resulting in daily arrivals being only sufficient to maintain low production. Under such market conditions, operating smelters generally lack confidence in increasing production in July, with most believing that production in July will be roughly the same as in June, and some manufacturers even still having expectations for production cuts. However, some large secondary lead smelters in east China, north China, and north-west China are expected to increase production in July compared to June due to the resumption of production after maintenance or the recovery of cross-month maintenance. Overall, secondary lead production in July is expected to maintain a growth trend.