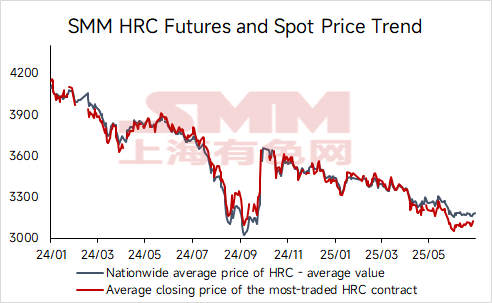

- In June, the nationwide average price of HRC fell by 2% MoM.

In June, the spot and futures prices of HRC were in the doldrums on a MoM basis. The monthly average nationwide price of HRC from SMM was 3,173.1 yuan/mt, down 2.3% MoM; the monthly average price of the most-traded HRC futures contract in June was 3,099 yuan/mt, down 2.7% MoM, and the spot-futures price spread strengthened slightly MoM.

• In the last week of June, HRC inventory began the inventory buildup cycle.

In June, HRC production maintained an upward trend, mainly driven by the resumption of production at steel mills that had undergone maintenance earlier and an increase in production schedules. In terms of inventory, as of June 26, the social inventory of HRC in 86 warehouses (large sample) nationwide, as compiled by SMM, stood at 3.0017 million mt, up 22,200 mt MoM, or a 0.75% increase MoM, and down 27.00% YoY. In the fourth week of June, the social inventory of HRC nationwide began to accumulate. Except for east China, inventories in central, south, north, and north-east China all increased, and the total inventory of HRC also began the inventory buildup cycle. In terms of apparent demand, the weekly average apparent demand for HRC compiled by SMM in June was 3.3232 million mt, down 1.69% MoM from May and down 4.18% YoY. Entering the off-season, downstream demand for HRC was impacted to a certain extent.

• HRC price center expected to decrease slightly in July

Entering July, considering the reduction in maintenance and the relatively favorable profit levels of steel mills, it is expected that HRC production by steel mills in July will increase slightly compared to June. On the demand side, although HRC is less affected by seasonality compared to rebar and other products, downstream demand remains resilient. However, frequent high temperatures and rainfall in July will still impact market transactions and logistics to a certain extent, thereby suppressing demand release. It is expected that total inventory will accumulate slightly on a MoM basis in July, and fundamental contradictions will be greater than those in June.

Macro side, July is still in a vacuum period for macroeconomic policies, and the policy's ability to boost prices is limited.

Overall, HRC prices in July will face a dual challenge from the macroeconomic vacuum and the increase in fundamental contradictions. It is expected that the HRC price center will decrease slightly in July.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)