》Check SMM aluminum product quotes, data, and market analysis

》Subscribe to view historical prices of SMM metal spot cargo

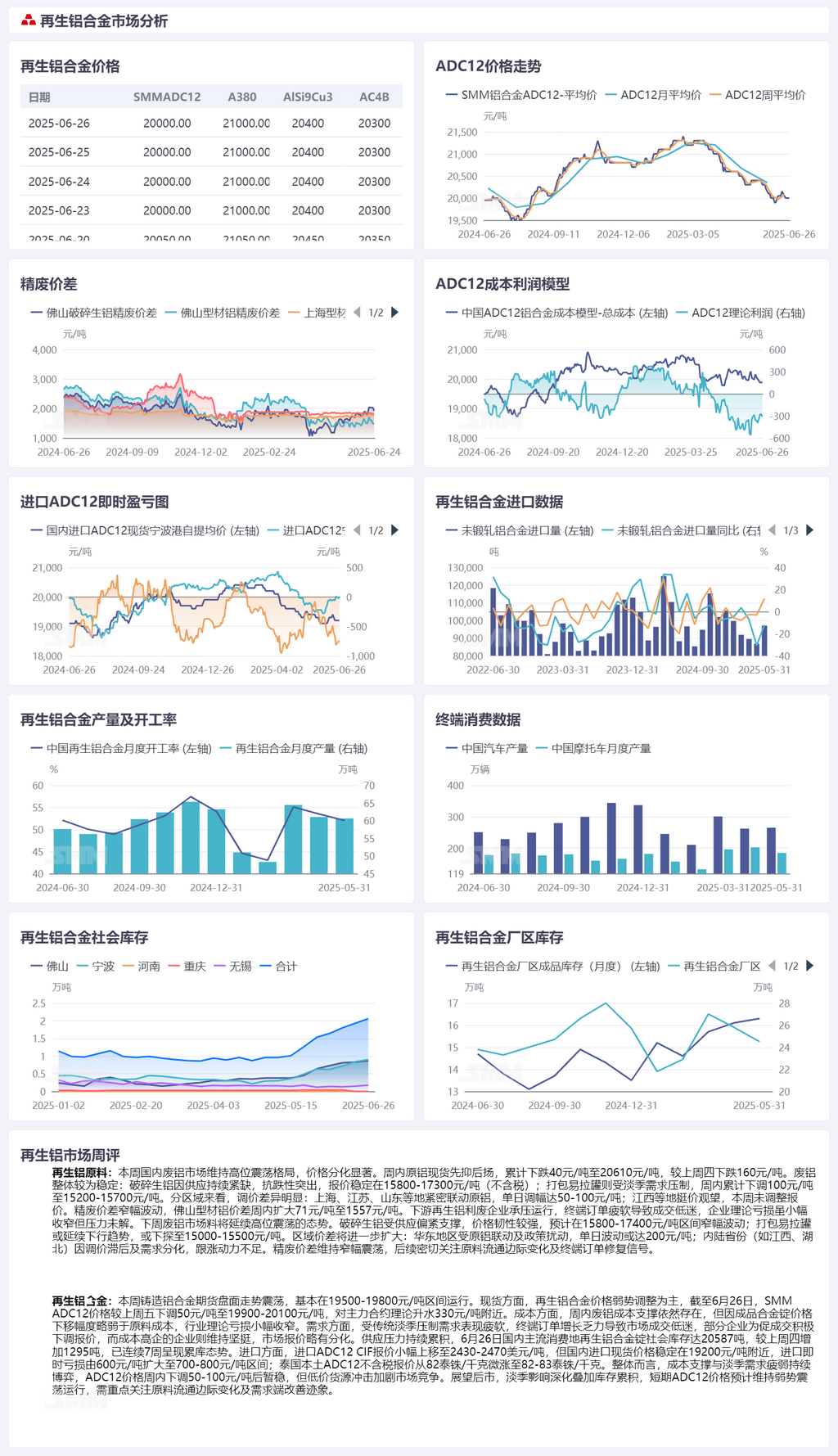

Raw Materials for Secondary Aluminum:

This week, the domestic aluminum scrap market maintained a pattern of fluctuating at highs, with significant price differentiation. Spot primary aluminum prices first declined and then rebounded during the week, cumulatively falling by 40 yuan/mt to 20,610 yuan/mt, a decrease of 160 yuan/mt compared to last Thursday. Aluminum scrap prices remained relatively stable overall: shredded aluminum tense scrap prices were resilient due to continued tight supply, with quotes stable at 15,800-17,300 yuan/mt (tax-exclusive); baled UBC prices were suppressed by off-season demand, cumulatively decreasing by 100 yuan/mt during the week to 15,200-15,700 yuan/mt. By region, price adjustments varied significantly: Shanghai, Jiangsu, Shandong, and other regions closely followed primary aluminum prices, with daily adjustments of 50-100 yuan/mt; regions like Jiangxi held prices steady and observed the market, without adjusting quotes this week. The price difference between A00 aluminum and aluminum scrap fluctuated rangebound, with the price difference for mixed aluminum extrusion scrap free of paint in Foshan expanding by 71 yuan/mt during the week to 1,557 yuan/mt. Downstream secondary aluminum scrap utilization enterprises operated under pressure, with weak terminal orders leading to sluggish transactions. Although theoretical losses for enterprises narrowed slightly, the pressure remained unresolved.

Next week, the aluminum scrap market is expected to continue fluctuating at highs. Shredded aluminum tense scrap prices are expected to remain resilient due to tight supply, fluctuating rangebound within the 15,800-17,400 yuan/mt range; baled UBC prices may continue to decline, possibly dropping to 15,000-15,500 yuan/mt. Regional price differences will further widen: east China may experience daily fluctuations of up to 200 yuan/mt due to primary aluminum linkage and policy disruptions; inland provinces (such as Jiangxi and Hubei) may lack upward momentum in price adjustments due to lagging adjustments and demand differentiation. The price difference between A00 aluminum and aluminum scrap will continue to fluctuate rangebound, with close attention paid to marginal changes in raw material circulation and signals of terminal order recovery.

Secondary Aluminum Alloy:

This week, the futures market for cast aluminum alloy fluctuated, basically operating within the 19,500-19,800 yuan/mt range. On the spot market, secondary aluminum alloy prices mainly fluctuated downward. As of June 26, the SMM ADC12 price decreased by 50 yuan/mt compared to last Friday to 19,900-20,100 yuan/mt, with a theoretical premium of around 330 yuan/mt against the most-traded contract. On the cost side, aluminum scrap costs continued to provide support during the week, but due to the slightly weaker decline in finished alloy ingot prices compared to raw material costs, industry theoretical losses narrowed slightly. On the demand side, suppressed by the traditional off-season, demand remained weak, with sluggish growth in terminal orders leading to sluggish market transactions. Some enterprises actively lowered quotes to promote transactions, while enterprises with high costs maintained firm prices, resulting in slightly differentiated market quotes. Supply pressure continued to accumulate, with social inventory of secondary aluminum alloy ingots in domestic mainstream consumption areas reaching 20,587 mt on June 26, an increase of 1,295 mt compared to last Thursday, marking the seventh consecutive week of inventory buildup. On the import front, the CIF offer for imported ADC12 rose slightly to $2,430-$2,470/mt, while the domestic spot import price remained stable around 19,200 yuan/mt. The immediate import loss widened from 600 yuan/mt to the range of 700-800 yuan/mt. The local tax-excluded offer for ADC12 in Thailand increased slightly from 82 baht/kg to 82-83 baht/kg. Overall, the tug-of-war between cost support and weak demand during the off-season persisted. After a decrease of 50-100 yuan/mt, the price of ADC12 stabilized temporarily, but the impact of low-priced goods intensified market competition. Looking ahead, with the deepening impact of the off-season and inventory accumulation, the price of ADC12 is expected to remain in the doldrums in the short term. Close attention should be paid to marginal changes in raw material circulation and signs of demand-side improvement.