SMM News on June 22:

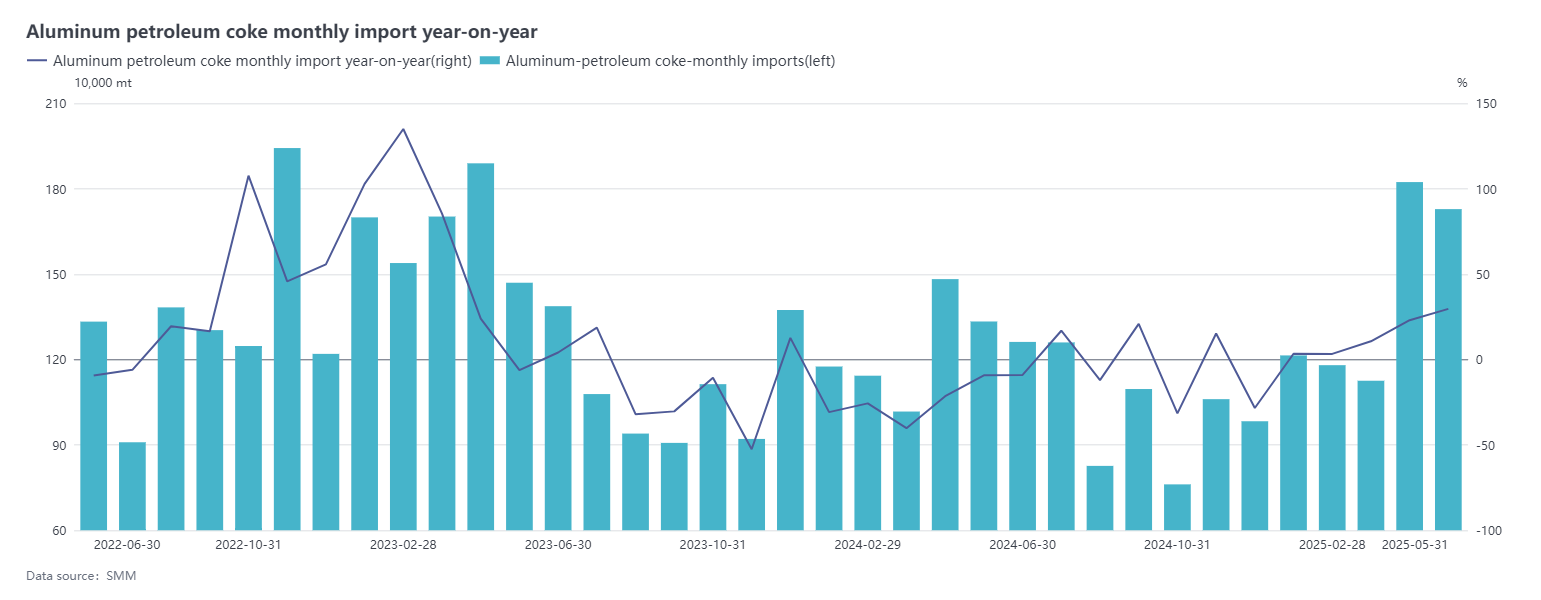

According to customs data, China imported 1.7281 million mt of petroleum coke in May 2025, down 5.21% MoM and up 29.6% YoY. The estimated import price of petroleum coke in May 2025 was $198.37/mt, up 5.29% MoM and 36.86% YoY. In 2025, China's cumulative total imports of petroleum coke reached approximately 7.0705 million mt, up 14.96% YoY.

In terms of import sources, the main countries/regions from which China imported petroleum coke in May 2025 were the US, Russia, and Saudi Arabia, with import volumes (import shares) of 671,100 mt (39%), 305,300 mt (18%), and 206,700 mt (12%), respectively.

Regarding import prices, petroleum coke import prices in May 2025 mainly increased, with the average import price being approximately $198.37/mt, up 5.29% MoM. There were a total of 17 countries/regions from which petroleum coke was imported this month, with 12 countries showing continuous import volumes. Among them, the import price of petroleum coke from Azerbaijan increased significantly, with a rise of over $300/mt. Additionally, import prices from Romania, Germany, and Argentina also showed good growth trends. On the other hand, import prices from Kazakhstan, Brazil, Saudi Arabia, and Russia declined notably, with drops in the range of approximately $30-50/mt.

Since Q2, the scale of domestic refinery maintenance has continued to expand, leading to a sustained decline in petroleum coke supply. However, with the concentrated arrival of previously shipped cargoes, port petroleum coke inventory has rapidly entered a buildup cycle. Overall, the overall supply in the petroleum coke market remains sufficient. Demand side, the market shows a weakening trend, with varying performances across different segments. The prebaked anode market mainly focuses on restocking based on rigid demand, with relatively cautious purchasing. Calcined petroleum coke enterprises mostly produce according to orders, with some enterprises actively reducing their operating rates due to profit pressures. The graphite electrode sector continues to weaken due to sluggish downstream demand, while the anode material market lacks significant growth momentum. Overall, downstream enterprises exhibit insufficient purchasing enthusiasm, suppressing demand for petroleum coke. In addition, the intensification of Sino-US trade frictions has increased market uncertainty, significantly cooling traders' buying sentiment and fostering a strong wait-and-see atmosphere. SMM expects that subsequent petroleum coke imports will decline.