On June 20, at the 2025 SMM (4th) Electric Drive System Conference & Drive Motor Industry Forum - Main Forum, jointly hosted by SMM Information & Technology Co., Ltd., Hunan Hongwang New Material Technology Co., Ltd., Louxing District People's Government, and the National-level Loudi Economic and Technological Development Zone, Ye Jianhua, GM of SMM's Industry Research Department, delivered a speech on "Price and Cost Analysis of Electric Drive Metal Materials."

Macro - Unpredictable and Complex

Chinese and US senior officials held the second round of talks in London, with the market awaiting the outcomes of the new round of talks.

►SMM Analysis

Ø On May 12, substantive progress was made in the China-US economic and trade talks in Geneva, and a joint statement was issued. The content of the trade agreement exceeded market expectations, alleviating the market's previous tension. In addition, negotiations between the US and countries such as India and Japan are currently showing a mild momentum, which is conducive to the global economic recovery and has boosted copper prices.

Ø On the evening of June 5, President Xi Jinping had a phone conversation with US President Trump at the latter's request.

Ø On June 9, Chinese and US senior officials held the second round of talks in London. The market expects a short-term easing of trade tensions. Currently, the first round of talks has concluded, with the US side sending positive signals and the Chinese side temporarily avoiding over-exerting its leverage, both leaving room for subsequent negotiations.

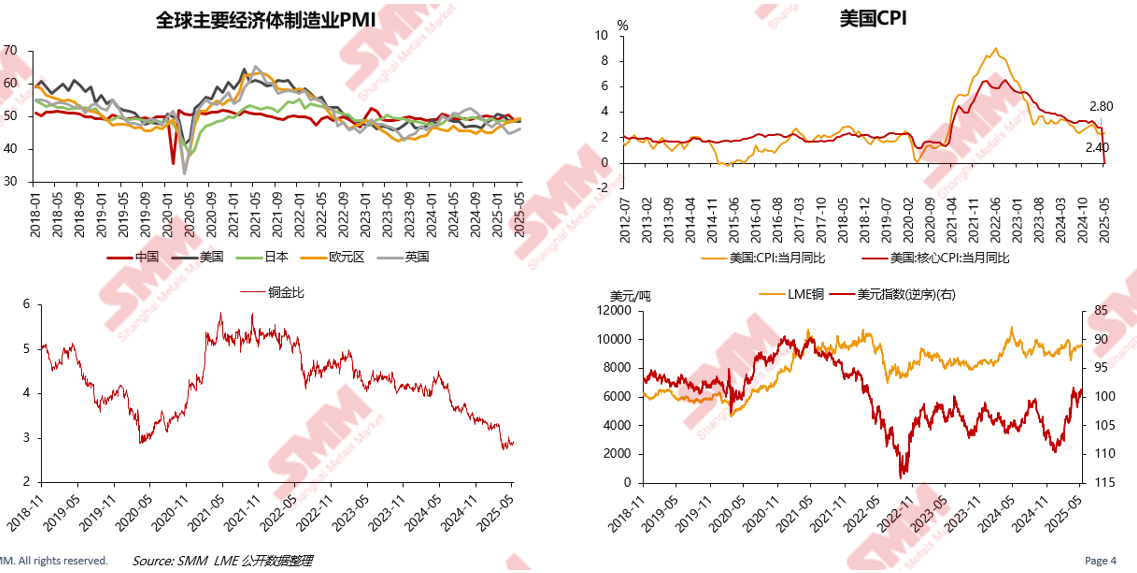

The manufacturing PMIs of major global economies are below 50. Affected by geopolitical conflicts and US tariff policies, the decline in the copper/gold ratio indicates strong market risk aversion sentiment.

He analyzed the trend changes in the manufacturing PMIs of major global economies, US CPI, copper/gold ratio, LME copper, and the US dollar index.

The "Stagnation," "Inflation," and "Recession" in the US economy are disrupting global asset prices.

He analyzed the content including the yields of US long-term and short-term government bonds, the previous value of the change in US non-farm payrolls, the University of Michigan Consumer Sentiment Index, the University of Michigan Consumer Current Conditions Index, the University of Michigan Consumer Expectations Index, the US: Markit: Manufacturing PMI (Final), and the US: Markit: Services PMI: Business Activity (Final).

Major economic indicators in Europe have begun to show signs of recovery, and large-scale infrastructure investment funds have been established to boost the economy.

He introduced the situation from the perspectives of the gradual reduction in eurozone interest rates and the slowdown in the decline of construction and retail confidence in the eurozone.

The domestic consumer market needs further stimulation, the export market will face greater challenges, and local government bond issuance is relatively fast.

He interpreted the data changes from China's export situation, consumer confidence, the continued growth of household savings, the monthly total issuance amount of local government bonds, the inventory area, commencement area, and completion area of the real estate industry.

Copper and Aluminum Supply

The increase in global major copper mine output primarily comes from expansion projects

It elaborates on the expected increments of new expansions & newly commissioned projects of major global copper mines from 2020-2030.

The rapid global expansion of copper smelter capacity makes it difficult to change the tight raw material situation

Domestically, the growth rate of refined capacity will still be higher than that of crude smelting capacity in the future, theoretically creating a gap that needs to be filled by copper anode and copper scrap.

Overseas, although there will be expansions in copper anode capacity in the future, it is fundamentally a transfer of copper concentrate raw materials. Due to the shortage of copper concentrate raw materials, it will be difficult to achieve the target of crude smelting capacity growth, potentially leading to a decline in global crude smelting production and an expansion of the actual gap with refined capacity.

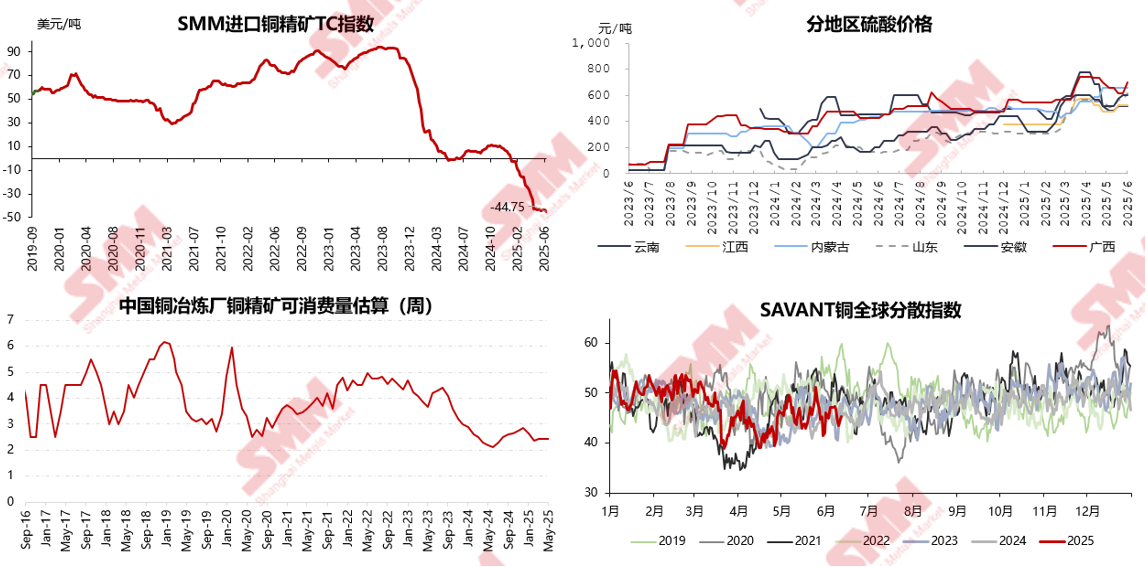

The shortage of copper concentrates intensifies, and the deterioration of the supply-demand structure in the short term is difficult to reverse

It analyzes data such as the expected global copper concentrate supply-demand balance results from 2021-2030 (including supply and demand-side interference rates), the annual long-term contract benchmark TC for copper concentrates, and the comparison of advantages in copper smelting raw materials.

Under the tight supply of copper concentrates, processing fees continue to decline, and smelter losses expand

It analyzes content such as the SMM imported copper concentrate TC index, regional sulphuric acid prices, estimates of consumable copper concentrates by Chinese copper smelters, and the SAVANT global dispersion index for copper.

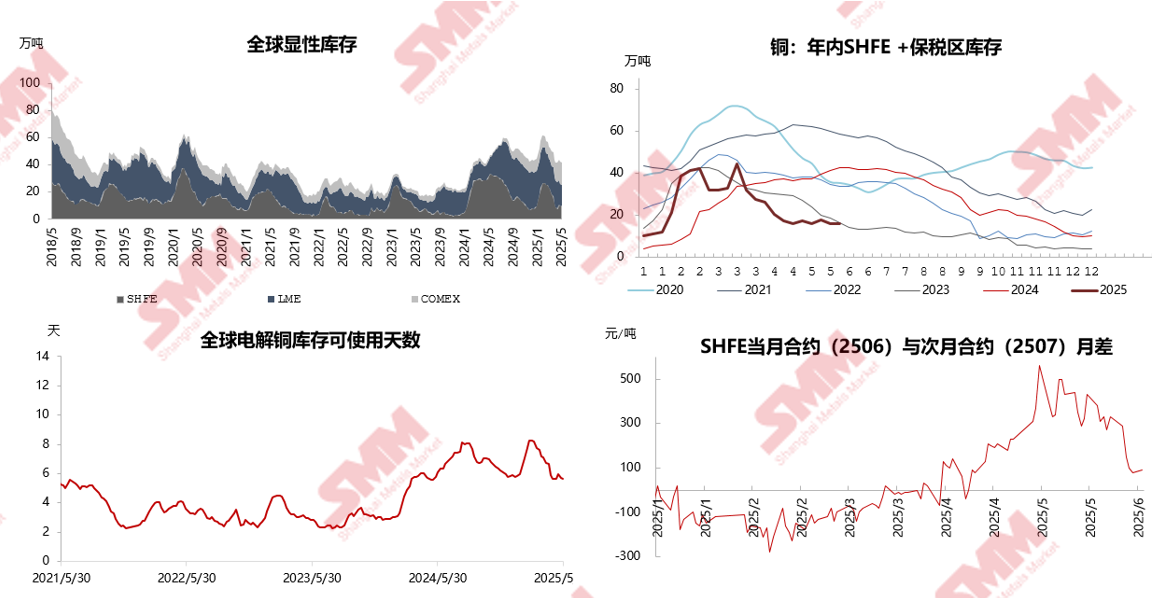

LC spread widened again in late April, with some imported B/Ls redirected to the US

In late April, the LC spread widened again, with the US continuing to attract supply. The supply gap in Chile and logistical issues in the DRC will continue to push up China's spot premium. A large number of LME Asia warrants were canceled, supporting the LME backwardation structure.

Expectations of tight supply are being realized, and the risk of copper futures squeeze increases

Entering May 2025, global visible inventory further declined, and the available days of global copper cathode continued to decrease. With strong borrowing funds in the market, there is a risk of a phased increase in copper prices in both domestic and overseas markets under the squeeze risk.

Aluminum cost narrowly declined in May, with mixed performance in cost breakdown in June

According to SMM data, the average tax-inclusive full cost of China's aluminum industry in May 2025 was 16,333 yuan/mt, down 0.3% MoM and 5.1% YoY. During the period, disruptions in the bauxite sector in mid-May boosted alumina futures prices rapidly, with a slight delay in spot price increases. Moreover, the alumina spot price trend was lower in the first half and higher in the second half of the month, resulting in limited growth in the monthly average alumina price in May. It is expected that the monthly average price will increase significantly in June.

►SMM Analysis

Entering June 2025, there is still upward momentum in the monthly average alumina price; auxiliary material costs are weakening; and electricity costs are declining. Overall, the aluminum cost may show a slight downward trend.

Overall, SMM expects the average tax-inclusive full cost of China's domestic aluminum industry to hover around 16,000-16,300 yuan/mt in June 2025.

In June, the proportion of liquid aluminum continued to rise, and there was no news of new capacity coming online as planned.

According to SMM statistics, domestic aluminum production in May 2025 (31 days) increased by 2.7% YoY and 3.4% MoM. The proportion of liquid aluminum in domestic aluminum smelters rose significantly in May, with the industry's proportion of liquid aluminum increasing by 1.48 percentage points MoM to 75.5%. This was mainly due to reduced casting ingot volumes and increased liquid aluminum proportions at enterprises in multiple northern regions. It is expected that the proportion will remain at highs in the subsequent period. Based on SMM's data on the proportion of liquid aluminum, domestic aluminum casting ingot volumes in May decreased by 6.15% YoY to approximately 913,000 mt.

►SMM Analysis

Entering June 2025, the operating capacity of China's domestic aluminum industry remained at highs. Considering the progress of remaining new or replacement projects this year, there are no short-term expectations for commissioning. Additionally, the rising proportion of liquid aluminum may become a significant factor affecting the spot aluminum market. Currently, aluminum smelters in multiple northern regions are increasing the proportion of liquid aluminum and reducing casting ingot volumes, which may subsequently impact arrivals in mainstream regions.

In the future, it is still necessary to monitor the trend of changes in the proportion of liquid aluminum in the aluminum industry, as well as the inventory and demand for alloyed products.

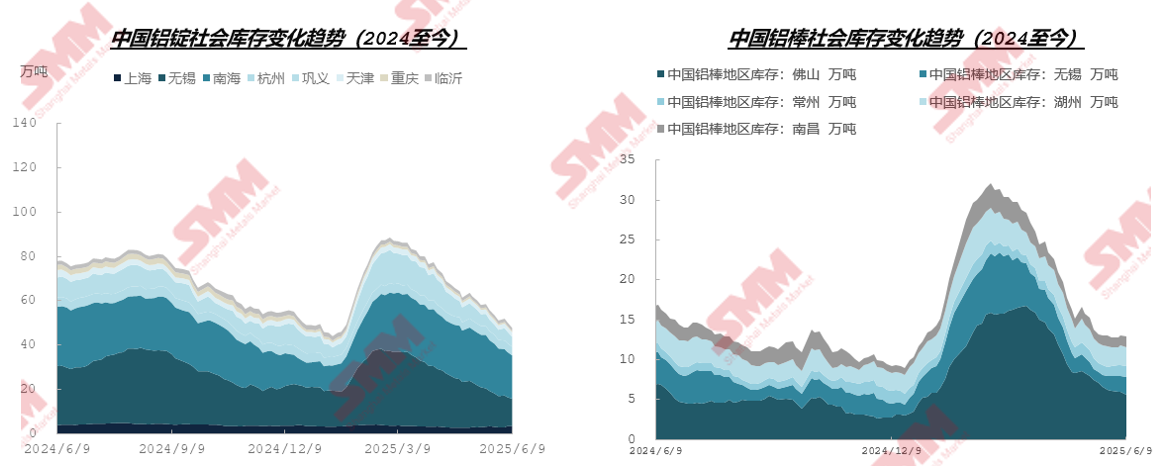

Social inventory destocking supports aluminum prices

According to SMM statistics, domestic aluminum social inventory was 477,000 mt on June 9, representing a destocking of 27,000 mt from the previous Thursday. Domestic aluminum billet social inventory was 129,500 mt, representing a destocking of 500 mt from the previous Thursday.

►SMM Analysis

Looking ahead, supported by low arrivals in the short term, inventory is expected to maintain a destocking trend and break through the 500,000 mt threshold, remaining at historically low levels. However, if downstream operating rates weaken during the off-season and demand growth cannot keep pace with the supply recovery, the destocking speed will significantly slow down. Close monitoring and verification are needed to further determine the period when domestic aluminum ingot inventory transitions to buildup during the off-season. It is temporarily expected that the inventory buildup inflection point may be delayed until late June or early July.

Demand: Terminal demand structure shows differentiation

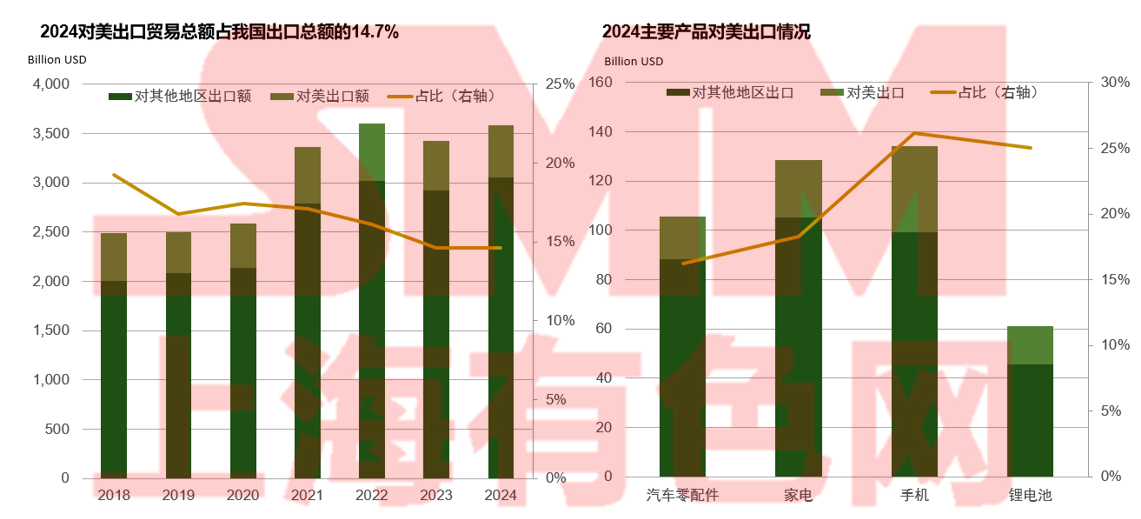

Although the degree of trade dependence on the US is declining, the US remains China's largest single trading partner.

Asia is China's main export market for copper semis and is vulnerable to US coercion. Copper scrap imports from the US will significantly decrease in 2025.

In 2024, copper semis exports to the North American market were 60,000 mt, accounting for 7.4% of total exports. In 2024, nearly 20% of China's copper scrap imports came from the US.

Aluminum processing operating rate: Entering the traditional off-season, the operating rate of aluminum processing enterprises pulls back

►Plate/sheet, strip and foil

•For aluminum plate/sheet and strip, a pattern of in the doldrums is expected to continue in June. Export orders are currently moderate, and domestic sales promotions such as the 618 event have prompted inventory destocking of end-use products. This may subsequently stimulate terminal procurement demand, indirectly benefiting the operating rate of aluminum plate/sheet and strip. However, entering the traditional off-season, the increase in downstream demand is limited, failing to offset the overall decline in demand.

•For aluminum foil, it is expected to continue in the doldrums in June, but some niche areas still show growth. Air-conditioner foil and beverage packaging foil (such as container foil) may benefit from increased consumption during the high-temperature season, driving a slight uptick in the operating rate at the beginning of the month; on the export front, the easing of Sino-US tariff barriers could spur concentrated shipments in the home appliance and electronics sectors, creating a recovery window for export-oriented products like double-zero packaging foil.

►Construction Aluminum Extrusion

•Entering June, leading building materials enterprises in central China reported that, apart from a small number of stable customers, new orders across all fields of building materials are weak, with infrastructure, doors and windows, and dealer orders showing varying degrees of decline.

►Industrial Aluminum Extrusion

•In June, due to the low purchasing sentiment among downstream component factories, companies are pessimistic about the production schedule for components in June. However, according to SMM, some newly invested capacities in Anhui are steadily ramping up, and are expected to reach full capacity in H2. Meanwhile, SMM's survey found that some small and medium-sized enterprises in Anhui and Henan are gradually exiting the PV market, retaining only some orders from long-established customers. The operating rate for PV frames in June is likely to remain at a low level. For automotive extrusion, although some companies in east and south China report that some OEMs predict an increase in demand in June, these companies believe there will be a discrepancy between actual and forecasted demand, and they do not plan to increase production for now.

►Aluminum Wire and Cable

•At the beginning of June, the industry's operating rate showed a divergent trend. Leading enterprises, relying on orders on hand, scheduled production reasonably. Although their operating rate declined MoM, they still demonstrated strong resilience, maintaining a relatively high level. Small and medium-sized enterprises, however, saw a significant weakening in their operating performance due to the end of a previous period of intensive deliveries and the rebound in the center of raw material aluminum prices, which dampened production willingness. Recently, State Grid launched the third batch of tenders for power transmission and transformation, but the market is currently in a lull between the tail end of previous order deliveries and the large-scale delivery of new orders. Market orders are showing a divergent and weakening trend, with only some State Grid orders still being delivered. New orders for overhead lines and PV in some provinces are declining, making it difficult to provide a strong boost to immediate production.

Aluminum semis exports increased 2.4% MoM in May, and subsequent exports are expected to continue growing.

According to customs data, China's unwrought aluminum and aluminum semis exports reached 547,000 mt in May 2025, up 5.60% MoM and down 3.19% YoY; cumulative exports from January to May were 2.431 million mt, down 5.1% YoY.

►SMM Analysis

According to the SMM survey, there was no significant increase in aluminum extrusion exports, and the industry as a whole continued to experience a situation with many inquiries but few actual transactions. However, based on the SMM survey, intensified competition in the domestic market has compelled enterprises to increase their efforts in exploring overseas markets. Despite the market's wait-and-see attitude, some industrial material enterprises in north China reported a small number of new orders with countries such as South Korea, Switzerland, Turkey, and Pakistan in the month, mainly exporting customized semi-finished products. In terms of building materials, some enterprises in south China, east China, and north China reported stable demand for curtain walls and doors and windows in Southeast Asia, supporting export volumes. Meanwhile, some enterprises in east China reported that their in-plant inventory included export orders that had not yet been shipped, which is expected to support aluminum extrusion exports in June. Regarding wheel hubs, according to feedback from SMM's surveyed clients, since 70% of the world's aluminum alloy wheel hub production is made in China, foreign clients find it difficult to find sufficient alternatives, and export orders in May maintained a steady and slight increase. In the short term, aluminum semis exports are expected to continue growing.

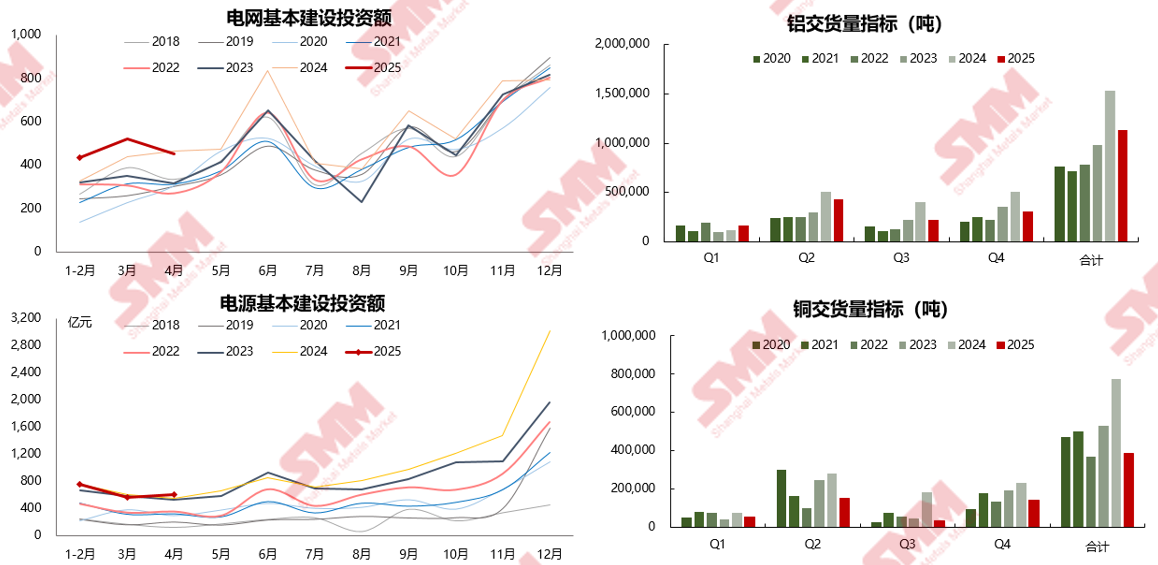

The State Grid Corporation of China plans to invest over 650 billion yuan in 2025, up over 7% from the actual investment in 2024.

The construction industry is still in a state of negative growth and cannot yet provide positive feedback for copper and aluminum consumption.

After comparing data changes in recent years, such as commercial housing sales, sources of real estate development funding, performance of real estate construction and completion areas, and changes in retail sales of building and decoration materials, it can be observed that the negative growth of construction and real estate-related data has narrowed.

The impact of tariffs on the home appliance industry is gradually becoming apparent.

►SMM Analysis:

Ø The operating rate of copper pipes declined both YoY and MoM in May, but the actual operating rate was higher than expected, mainly due to the gradual recovery of North American end-user orders that had previously stalled after the Sino-US tariff negotiations.

Ø In June, the actual domestic sales production schedule of household air conditioners increased by 29.3% YoY, while the actual exports decreased by 18.3% YoY. Export schedules dragged down the operating rate of copper pipes. It is estimated that the operating rate in June will be 80.22%, down 1.54 percentage points MoM and up 3.45 percentage points YoY.

Ø With the arrival of the off-season, the operating rates of domestic sales production schedules and copper pipe factories primarily focused on domestic sales will seasonally decline, and there are no high expectations for export demand. It is expected that the operating rate of copper pipes will gradually decline in the future market.

Demand: New energy remains the main driver of aluminum consumption growth, but the growth rate is slowing down.

In the end-use consumption of aluminum, the construction, transportation, and power electronics industries account for nearly 70% of the total consumption. In recent years, with the downturn in the real estate sector and the rapid development of the new energy industry, its share of aluminum consumption has been continuously increasing, providing a new consumption engine for domestic aluminum consumption.

►SMM Analysis

2024 was a year when domestic aluminum consumption continued to tilt towards the new energy sector. The expected growth in global PV installations and the increasing penetration rate of NEVs year by year drove up aluminum consumption in the power and transportation sectors, offsetting the decline in aluminum consumption in other traditional sectors such as construction. In 2024, the total aluminum consumption in the domestic power electronics and transportation sectors increased by 7.5% YoY, accounting for 46.3% of the total domestic aluminum consumption. In 2025, the total aluminum consumption in these two sectors is expected to continue growing by 4%, providing a new consumption engine for domestic aluminum consumption.

Based on comprehensive calculations of aluminum consumption in other sectors, SMM expects that domestic primary aluminum consumption will increase by 1.5% YoY in 2025, with the power electronics and transportation sectors leading the growth in aluminum consumption.

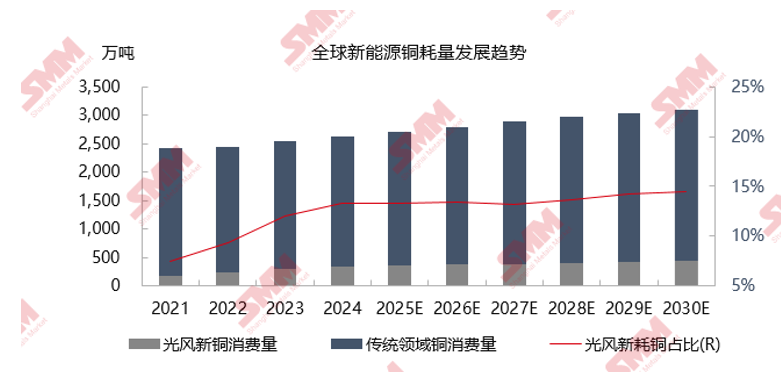

In the medium and long-term, the new energy sector remains one of the main drivers of global copper consumption growth.

It analyzed changes in global NEV production and the development trend of global new energy copper consumption from 2022-2030E.

Global Copper Cathode Balance and Price Forecast

►SMM Analysis

Ø In Q1 2025, market risk sentiment rose before the implementation of Trump's tariffs. The expectation of tariffs specifically targeting copper once drove up COMEX copper prices, leading to a significant widening of the LME-CME price spread, which persisted at a high level, with the US siphoning off a large amount of copper. Additionally, since December, the US economic data has been favorable, and inflation expectations have risen, leading to a general stabilization and rebound in commodity prices. Domestically, favorable policies were introduced at the beginning of the year, fostering a positive macro sentiment that was beneficial for copper prices. On the fundamental side, the expected expansion of the ore supply deficit and the anticipated contraction in copper cathode supply in 2025 also contributed to the rise in copper prices.

Ø In Q2 2025, with the implementation of reciprocal tariffs by the US and the strengthening of China's countermeasures, a tariff storm hit, coupled with weakening US economic data. The market traded on expectations of economic damage caused by tariffs, leading to a sharp drop in copper prices, which serve as a barometer of the global economy. Subsequently, China may introduce various favorable policies to boost domestic demand, while Sino-US negotiations may ease trade tensions. Supported by fundamentals (accelerated destocking of copper outside the US, low global inventory levels, and expectations of squeezing inventories under a strong backwardation structure) and a mitigated macro sentiment, copper prices rebounded.

Ø In Q3 2025, amid expectations of production cuts by smelters, the off-season in consumption, and the damage caused by previous tariffs, the market faced a tug-of-war between weak supply and demand, with inventory at risk of buildup. However, global inventory levels will still hover at low levels. Although there will be certain pressure on copper prices, the upside potential is limited.

Ø In the early stage of Q4 2025, the effects of relatively loose fiscal policies in both China and the US will become apparent, and expectations for global economic recovery will gradually strengthen. However, the deterioration of ore supply will leave smelters facing a raw material shortage, leading to a further decline in global copper cathode production. The center of copper prices is expected to move upward again.

Supply-Demand Balance Table: Global supply and demand to shift to a slight surplus in 2025, with demand entering a period of steady growth

►SMM Analysis

ØFrom a full-year perspective in 2025, the domestic supply side in China will gradually approach its ceiling. New capacity additions are concentrated for commissioning in Q4, with annual production growth narrowing to around 1.9%. Meanwhile, the development of new energy and other sectors in China will continue to drive primary aluminum consumption. Export orders from overseas markets remain moderate, and the decline in aluminum consumption in China's traditional construction sector is limited. SMM expects aluminum consumption in China to increase by approximately 2.4% YoY for the full year of 2025. Additionally, despite aluminum prices maintaining a trend where the overseas market outperforms the domestic market, net imports this year have exceeded expectations and increased, partly offsetting the "ceiling" constraints. However, overall supply remains tight. Coupled with a significant reduction in casting ingot volumes, the price center of aluminum will shift upward throughout the year.

ØOutside of India, consumption growth in other overseas regions is not optimistic. However, with the commissioning of new projects in Southeast Asia, the overseas supply-demand balance will shift towards inventory buildup.

Key Points on Aluminum

►SMM Analysis

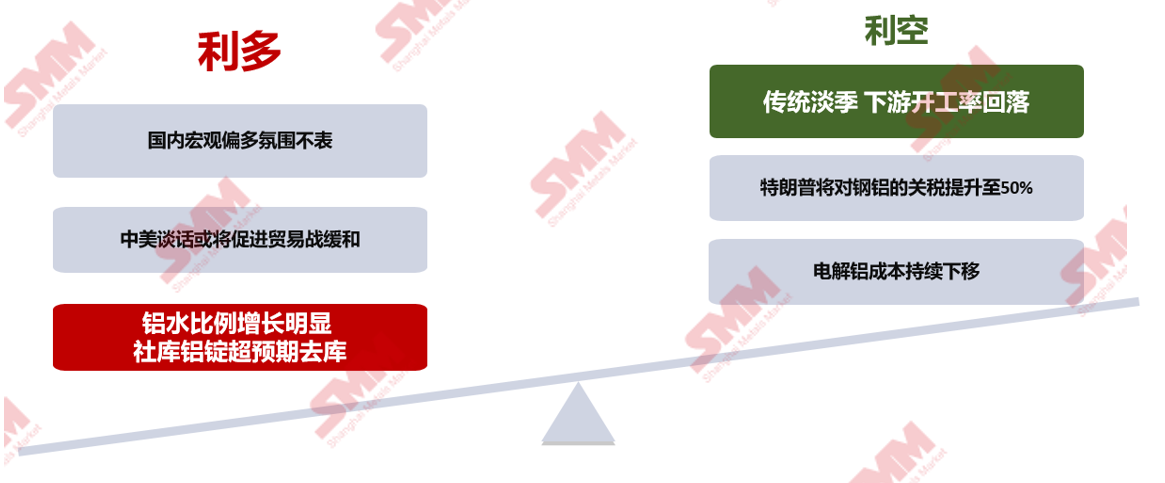

Entering June, the domestic macroeconomic environment in China is generally positive, but considering the time required for policy implementation, there has been no significant feedback from the industry yet. The negative impact of overseas trade wars still exists, and caution is needed regarding the uncertainties in overseas macroeconomic conditions. On the fundamental side, the domestic aluminum market is characterized by a mix of bullish and bearish factors. On the supply side, aluminum smelters are operating steadily, with a notable recent decrease in casting ingot volumes, affecting deliveries to major consumption centers. The unexpected destocking of social inventory has provided support to aluminum prices. On the demand side, the downstream sector is entering the traditional off-season, compounded by the impact of overconsumption in the PV sector, leading to a bearish market outlook for demand and insufficient upward momentum for aluminum prices. Given the current mixed fundamental factors, aluminum prices are expected to fluctuate considerably, with the monthly average price center around 20,150 yuan/mt. Continuous attention should be paid to the progress of tariff events, changes in aluminum ingot inventory, and variations in downstream orders.

》Click to view the 2025 SMM (4th) Electric Drive System Conference & Drive Motor Industry Forum Report Special