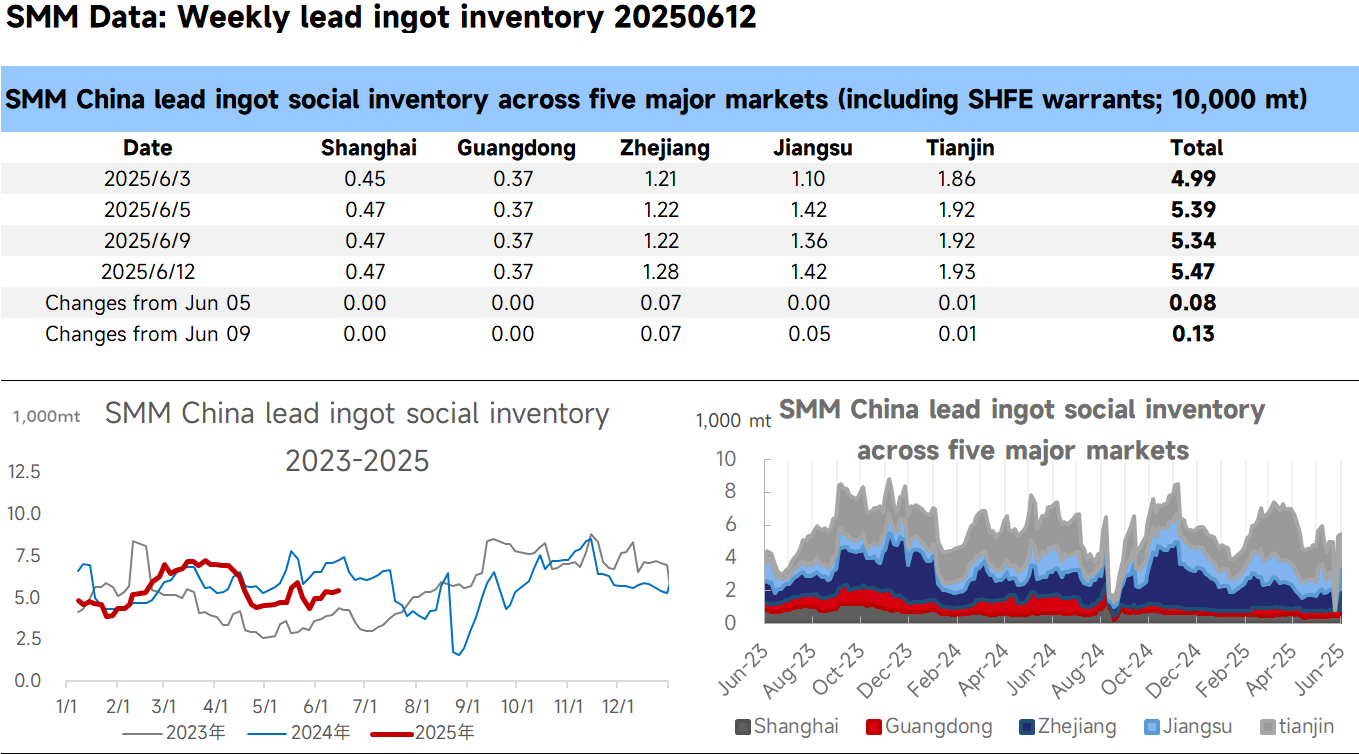

SMM News, June 12: According to SMM, as of June 12, the total social inventory of lead ingots across five locations tracked by SMM reached 54,700 mt, an increase of approximately 800 mt from June 5 and an increase of 1,300 mt from June 9.

This week, production at primary lead smelters remained stable with a slight increase, while secondary lead enterprises were generally in a state of production reduction or suspension due to factors such as environmental protection, losses, and insufficient scrap supply. This led to a regional tightening of lead ingot supply, causing lead consumption to flow into the primary lead market. As the lead consumer market was still in the off-season, trading in the spot lead market improved regionally, with the southern market seeing better trading volumes than the previous week. Meanwhile, lead prices fluctuated and strengthened, prompting primary lead smelters to actively sell their products. The spread between futures and spot prices of lead in major producing areas ranged from 180 to 220 yuan/mt. With the approaching delivery of the SHFE lead 2506 contract, some suppliers transferred their inventory to delivery warehouses. As a result, the social inventory of lead ingots increased as expected, but the increase was relatively small. Next week, the front-month contract of SHFE lead will enter the delivery phase. The expectation of suppliers transferring inventory to delivery warehouses before delivery may lead to further increases in the social inventory of lead ingots. In addition, we need to continue monitoring the impact of environmental protection inspections, scrap battery supply, and other factors on the production of secondary lead enterprises.

![SHFE Lead Rebounded Slightly After an Intraday Dip and Closed with a Small Bearish Candlestick [Lead Futures Brief Review]](https://imgqn.smm.cn/usercenter/qnyHQ20251217171721.jpeg)

![LME Lead Bottomed Out, While SHFE Lead Retreated After Rapid Rise and Consolidated [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/EhsCj20251217171721.jpeg)