SMM June 11 News:

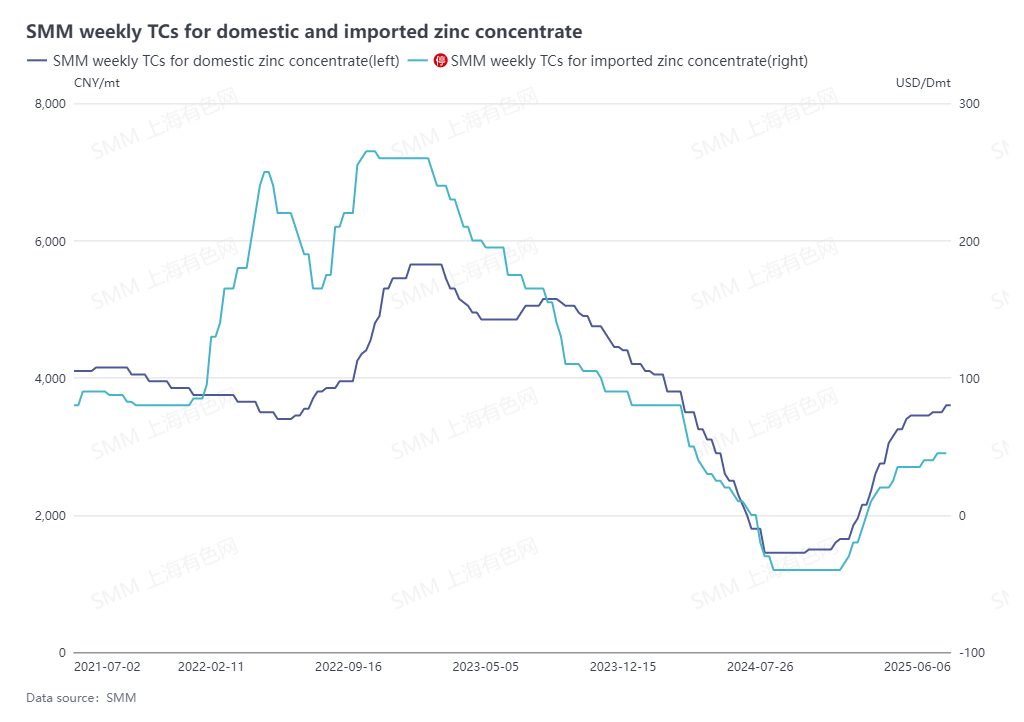

As of June 6, 2025, the SMM weekly domestic zinc concentrate TC rose to 3,600 yuan/mt (metal content), and the SMM imported zinc ore index increased by $50.35/dmt, with overall processing fees continuing to rise compared to May. Behind the sustained high production of smelters, what factors are driving the increase in zinc concentrate TCs in June? Let's analyze this from the supply side.

Domestic Ore Perspective:

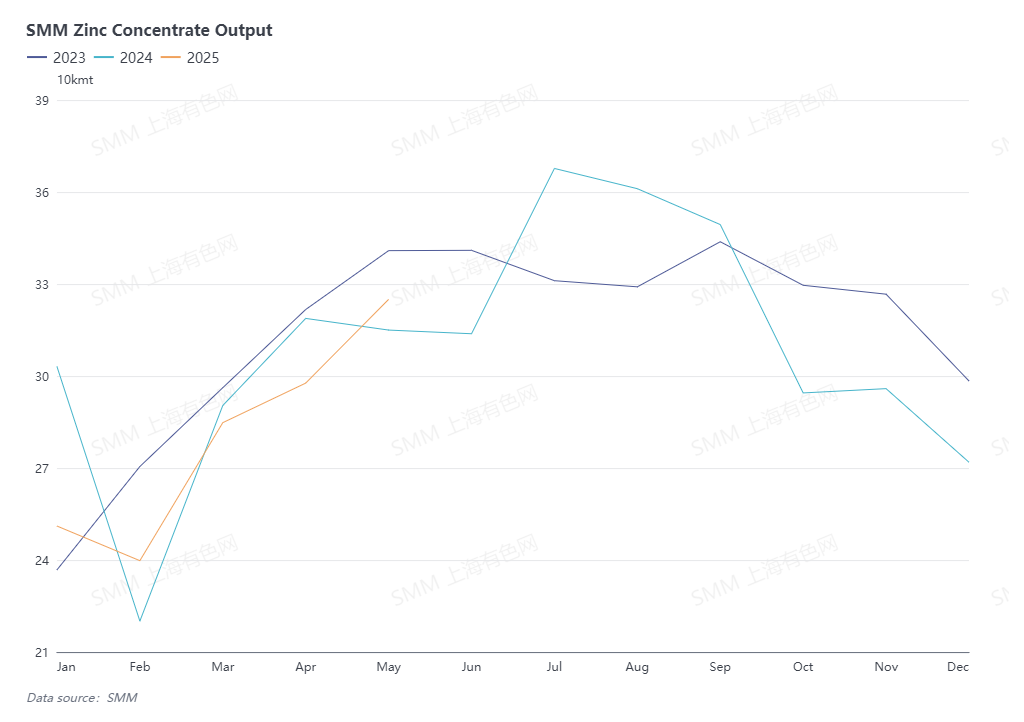

The production of mines that had previously reduced or halted operations gradually recovered. The resumption of production at mines in Xinjiang also brought significant incremental output. In May, the SMM domestic zinc ore production continued to grow on a MoM basis. As June arrives, the capacity of resumed production mines continues to climb, and it is expected that domestic zinc ore production will further increase. Additionally, despite recent environmental protection checks in some domestic regions, their impact on the production of lead-zinc mines has been limited, with the entire industry maintaining normal production operations.

Imported Ore Perspective:

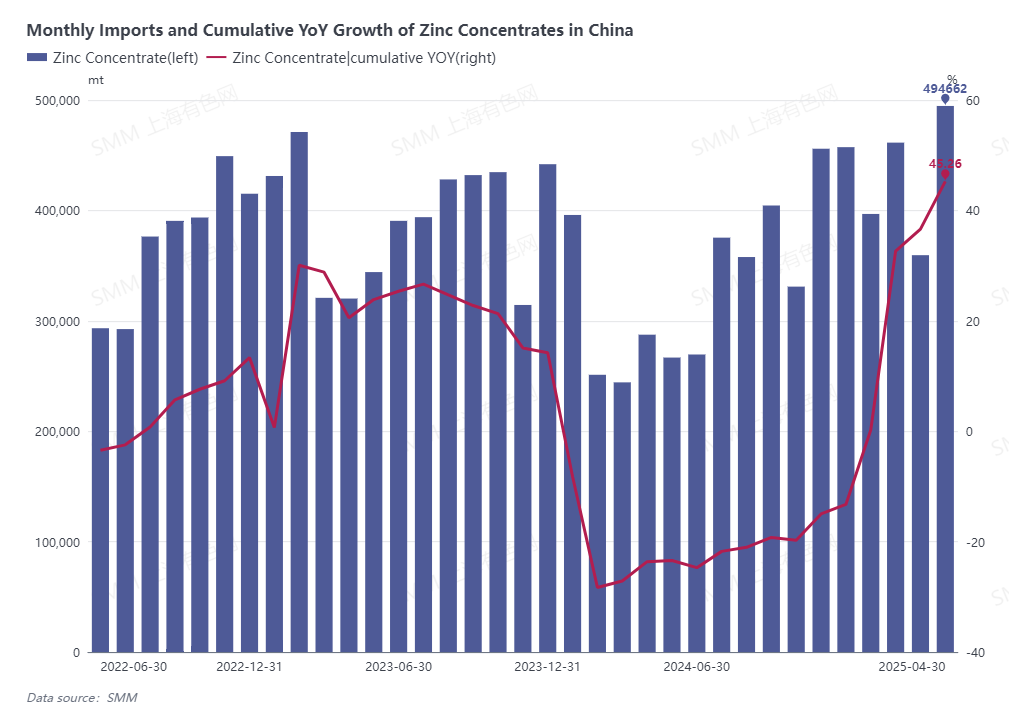

According to data from the General Administration of Customs of China, China's cumulative zinc concentrate imports from January to April reached 1.7125 million mt (mt), up 45.26% YoY, indicating a relatively high level of overall imported zinc ore. Furthermore, a large shipment of 0Z zinc ore from Russia arrived at the Manzhouli port in May, effectively supplementing the supply in north China regions such as Inner Mongolia. Combined with the continuous arrival of imported zinc ore previously ordered by smelters, this has collectively supported a relatively higher increase in zinc concentrate TCs in north China compared to south China in June.

Overall, due to the continuous supplementation of imported zinc ore, the days of raw material inventories at smelters, as tracked by SMM, remained at around 27 days in May, with raw material supply remaining relatively abundant, driving up zinc concentrate TCs in multiple regions in June. However, as new smelters that started production in June gradually ramp up and previously shuttered smelters resume production, the demand for zinc ore will become more robust. Without additional supplementation of imported zinc ore, it is expected that there may be limited room for further increases in zinc concentrate TCs in the future.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)