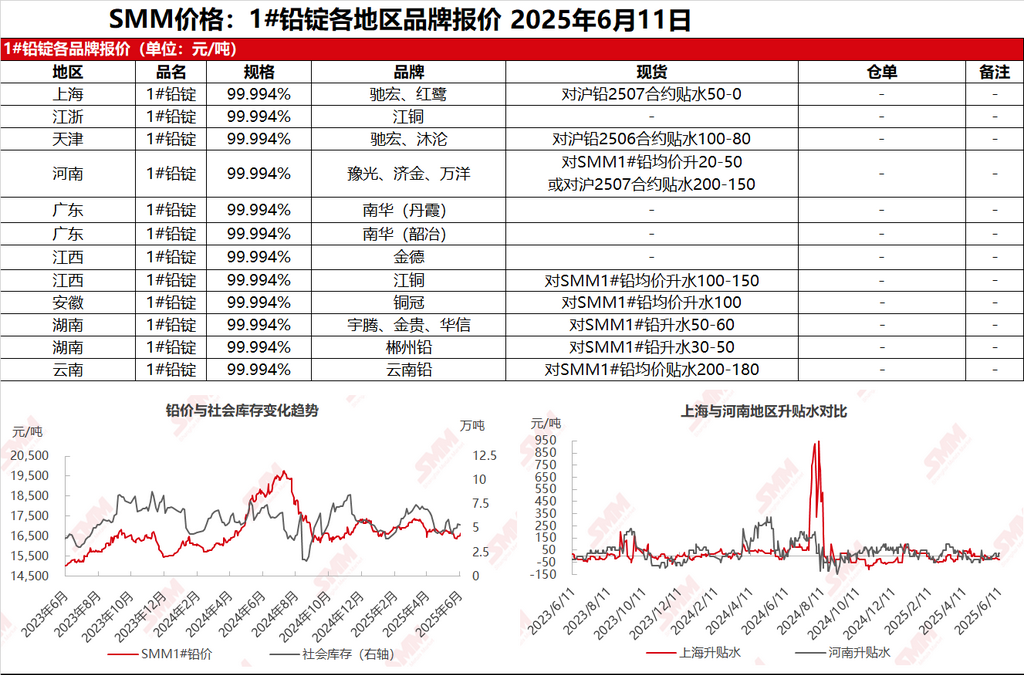

SMM June 11 report: In the Shanghai market, Chihong and Honglu lead were quoted at 16,800-16,850 yuan/mt, with quotations against the SHFE lead 2507 contract at a contango of 50-0 yuan/mt. SHFE lead maintained high-level consolidation, and with delivery approaching, some suppliers were waiting for delivery, with quotations remaining unchanged from yesterday. However, there were differences in the transactions of cargoes self-picked up from primary lead smelters, especially in south China, where transactions were improving and traded at a premium against the SMM 1# lead average price. In north China, transactions were sluggish. In addition, most secondary lead enterprises in east China were in a state of production reduction or suspension. Limited supply led some lead demand to flow into the primary lead market, and spot market transactions improved regionally.

Other markets: Today, the SMM 1# lead price remained unchanged from the previous trading day. In Henan, suppliers' quotations against the SHFE lead 2507 contract were at a contango of 200-150 yuan/mt ex-factory, with sluggish transactions. In Hunan, smelters' quotations against the SMM 1# lead were at a premium of 30-50 yuan/mt ex-factory. Due to a decline in inventory, some enterprises raised their quotations to a premium of 50-60 yuan/mt against the SMM 1# lead average price, and there was a wait-and-see sentiment due to reluctance to sell. During the day, SHFE lead fluctuated within a range. Due to production reduction or suspension in secondary lead enterprises, there were significant regional differences in supply. Some demand shifted to the primary lead market. Downstream enterprises purchased as needed and preferred cargoes self-picked up from smelters. Trading by traders was generally slow, and there were significant differences in spot market transactions.