Since April 2022, the SMM survey sample for rebar production scheduling has been expanded to include 56 enterprises.

According to the SMM survey data from 56 key steel-producing enterprises:

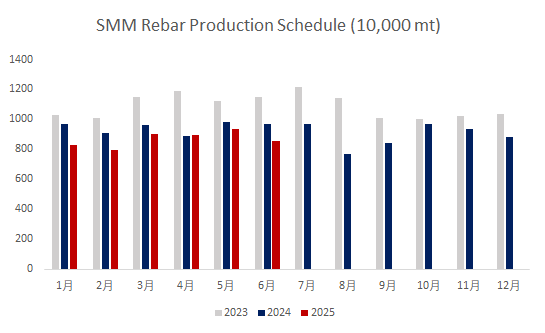

The planned rebar production in June was 8.5197 million mt, a decrease of 820,600 mt compared to the actual production in May, representing an 8.79% decline.

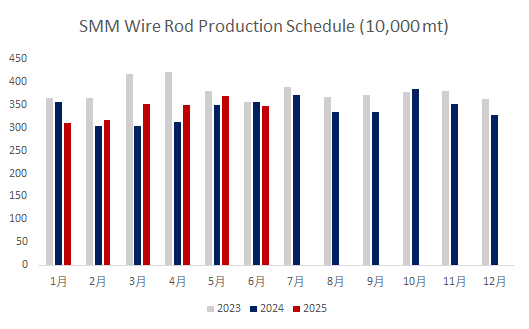

The planned wire rod production in June was 3.4809 million mt, a decrease of 208,500 mt compared to the actual production in May, representing a 5.65% decline.

Chart-1-2: Production Schedule of Rebar and Wire Rod in Mainstream Building Material Steel Mills (56 Steel Mills)

Data source: SMM

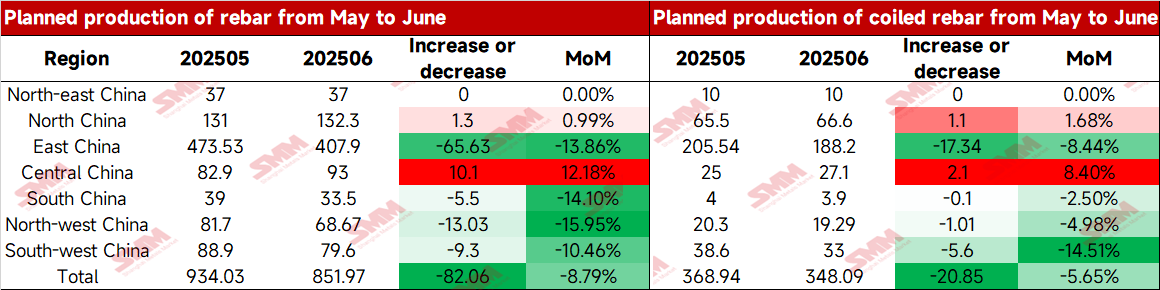

Table-1: Actual Production Schedule of Rebar and Coiled Rebar in May and Planned Production Volume in June (10,000 mt)

Data source: SMM

Looking ahead, influenced by the news of crude steel production reduction and the transition into the off-season for demand, some steel mills have successively arranged production cut plans. Secondly, with the delivery of billet orders from east China's external sales and the good order-taking and profitability of round steel, special steel, and other varieties from multiple steel mills, steel mills have diverted pig iron from the construction materials sector to other varieties, leading to a significant reduction in overall construction materials production at steel mills in June. Losses at EAF steel mills have intensified, with some steel mills planning to halt operations. It is expected that production will continue to decline in the later period. On the demand side, affected by high temperatures in the north and plum rain season in south China in June, construction site progress has been limited, and the downstream procurement pace will slow down, with demand continuing to deteriorate compared to May. On the whole, there is an expectation for further concessions on the raw material side, and steel mill profits will be maintained in the short term. However, considering the accumulation pressure on in-plant inventory during the off-season, manufacturers will adjust their production structures accordingly or arrange annual maintenance plans in advance. Under the situation of a decline in both supply and demand, it is expected that the spot trend of construction steel in June may continue to be in the doldrums, but the fluctuation range will narrow compared to May.

![[SMM Steel] Tata Steel partners with USTB to accelerate low-carbon steelmaking](https://imgqn.smm.cn/usercenter/ikbxI20251217171718.jpg)

![[SMM Hot-Rolled Coil Arrivals] Arrivals in Mainstream Markets Increased Slightly WoW This Week](https://imgqn.smm.cn/usercenter/GGaSo20251217171716.jpg)

![[SMM Zhangjiagang Hot-Rolled Coil Inventory] Zhangjiagang Inventory Turned Lower WoW This Week](https://imgqn.smm.cn/usercenter/Zznfn20251217171716.jpg)