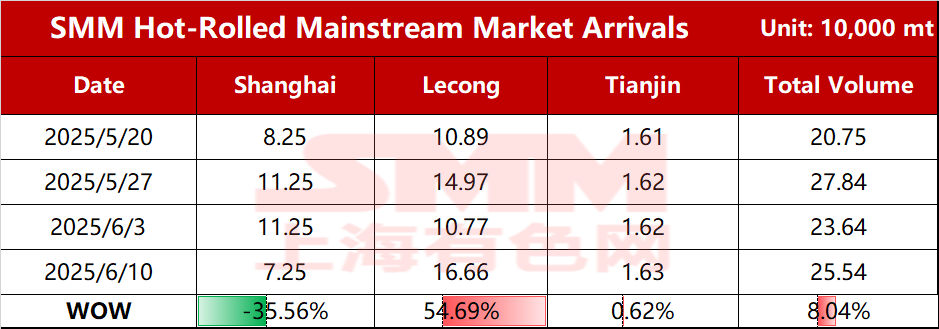

SMM Steel News on June 10: According to SMM statistics, the estimated total shipments of resources in the mainstream market this week were 255,400 mt, an increase of 19,000 mt from the shipment level WoW. By market:

Chart-1: Comparison of Arrivals in Mainstream Markets

Source: SMM Steel

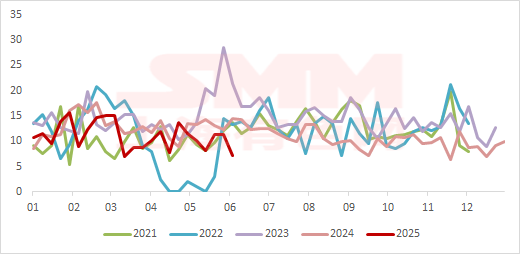

Shanghai Market: Shipments to the Shanghai market declined WoW this week. Specifically, shipments from north and east China remained stable, while shipments from north-east and south China decreased WoW. Looking ahead, with HRC prices in the doldrums recently and the Shanghai market's prices being lower than those in the south China market, some mainstream steel mills have low willingness to ship, and arrivals in the Shanghai market are expected to remain low in the short term.

Chart-2: Arrivals in the Shanghai Market

Source: SMM Steel

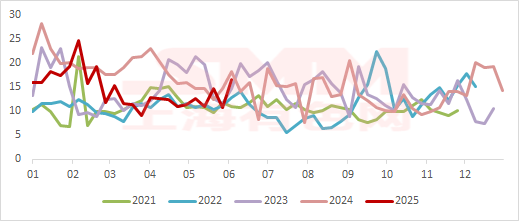

Lecong Market: Shipments to the Lecong market increased significantly WoW this week. Specifically, on the one hand, resources from north China remained stable. On the other hand, due to the price spread advantage, local mainstream resources DDH and WG showed a clear shipping preference. Looking ahead, with export order pressure for WG rebounding in the latter half of the month, domestic sales supply may increase. Meanwhile, with the price spread advantage in south China, some northern resources will also arrive at ports successively. Therefore, it is expected that arrivals in the Lecong market will remain at a relatively high level in the short term.

Chart-3: Arrivals in the Lecong Market

Source: SMM Steel

SMM releases HRC shipment data for mainstream market flows every Tuesday. To subscribe or follow more data, please scan the QR code below.

![[SMM Daily Chromium Review] Futures Rose While the Spot Market Remained Temporarily Stable, with Limited Adjustment in the Ferrochrome Market](https://imgqn.smm.cn/usercenter/rBCZR20251217171716.jpg)

![[SMM Iron & Steel] Hoa Phat Boosts Green Energy at Dung Quat Steel Complex](https://imgqn.smm.cn/usercenter/LSkpO20251217171720.jpg)