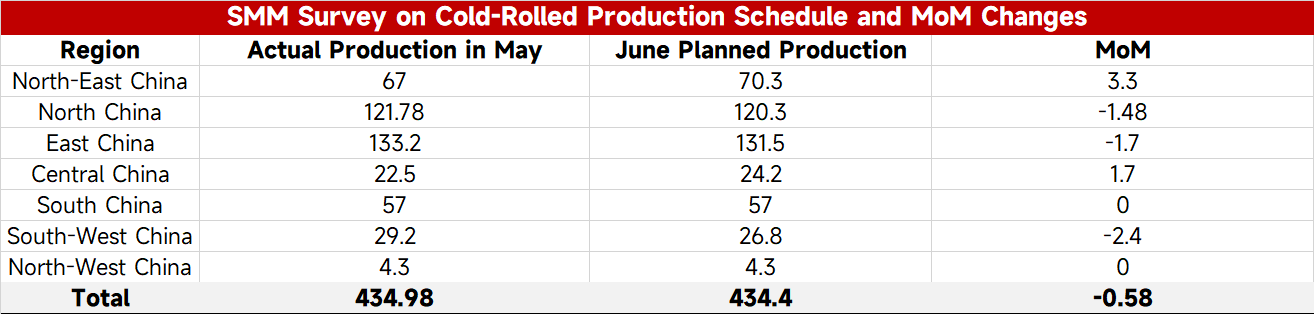

- SMM Cold-rolled Production Schedule: The daily average cold-rolled production schedule of steel mills in June was basically stable

According to the latest tracking by SMM, the planned production volume of cold-rolled commercial materials for June from 31 mainstream steel mills producing cold-rolled sheet and coil totaled 4.344 million mt, a decrease of 5,800 mt compared to the actual production volume of cold-rolled commercial materials in May, representing a decline of 0.13%. On a daily average basis, June had one fewer day than May. The planned daily average production volume of cold-rolled materials in June was 144,800 mt, up 3.20% MoM from the actual daily average production volume in May.

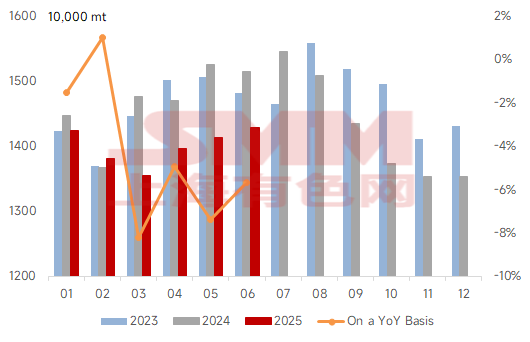

- SMM HRC Production Schedule: Daily Average HRC Production Schedule Increases by Over 5%

According to the latest tracking by SMM, the planned production volume of HRC commodity materials for June from 39 mainstream steel mills producing HRC totaled 14.2862 million mt, an increase of 264,500 mt compared to the actual production volume of HRC commodity materials in May, representing a growth rate of 1.89%. On a daily average basis, June has one fewer day than May. The planned daily average production volume of HRC commodity materials for June is 476,200 mt/day, an increase of 23,900 mt compared to the actual daily average production volume of HRC commodity materials in May, representing a growth rate of 5.28%.

In June, some steel mills that had undergone maintenance in the early stage completed their maintenance and gradually resumed production. Additionally, from the perspectives of profitability and order-taking, the current situation of hot-rolled coil (HRC) production at most steel mills is slightly better than that of building materials. Overall, steel mills' enthusiasm for HRC production remains moderate. Under these combined influences, the daily average production schedule for domestic hot-rolled coil in June increased significantly MoM from May.

- Breakdown by domestic and export trade:

Domestic trade: In June, the production schedule for HRC in domestic trade was 13.0984 million mt, with a daily average of 436,600 mt, up 19,300 mt MoM from the actual daily average production in China in May, representing a 4.6% increase.

Exports: The planned HRC exports for June were 1.1878 million mt, an increase of 101,800 mt compared to the actual exports in May, representing a MoM increase of 9.37%. The planned HRC exports for domestic steel mills in June increased slightly compared to the actual exports in May on a MoM basis.

Summary: In June, the daily average planned production of hot-rolled coil (HRC) by domestic steel mills increased MoM compared to the actual production in May. This was mainly due to the gradual resumption of production at some steel mills that had undergone maintenance earlier, coupled with the fact that the profitability of producing HRC was slightly better than that of producing construction materials and other varieties. As a result, the daily average production schedule for HRC in June increased significantly.

Looking ahead, as the off-season approaches, downstream demand will be impacted to a certain extent and weaken. In terms of supply, the production schedule for HRC in June increased MoM, in line with market expectations. The inventory pressure for HRC will gradually emerge in mid-to-late June. However, considering that current inventory levels are at a low point compared to the same period in recent years, the accumulation of short-term fundamental contradictions is limited.

In terms of news, periodic speculation surrounding external trade wars, macro policies, and rumors of production restrictions on the supply side, in the absence of unexpectedly favorable policy stimuli, the average price of HRC in June is expected to decline slightly.

![[SMM Chromium Daily Review] Awaiting Steel Tender Bids, Market Running Stable for Now](https://imgqn.smm.cn/usercenter/vhvTQ20251217171715.jpg)

![[SMM Stainless Steel Daily Review] Indonesian Nickel Ore HMP Price Adjustment Drove Stainless Steel Futures and Spot Prices Higher](https://imgqn.smm.cn/usercenter/FGavQ20251217171717.jpg)

![[Shanghai Construction Group: Newly Signed Contracts Totaled 60.374 Billion Yuan in Q1]](https://imgqn.smm.cn/usercenter/ikbxI20251217171718.jpg)