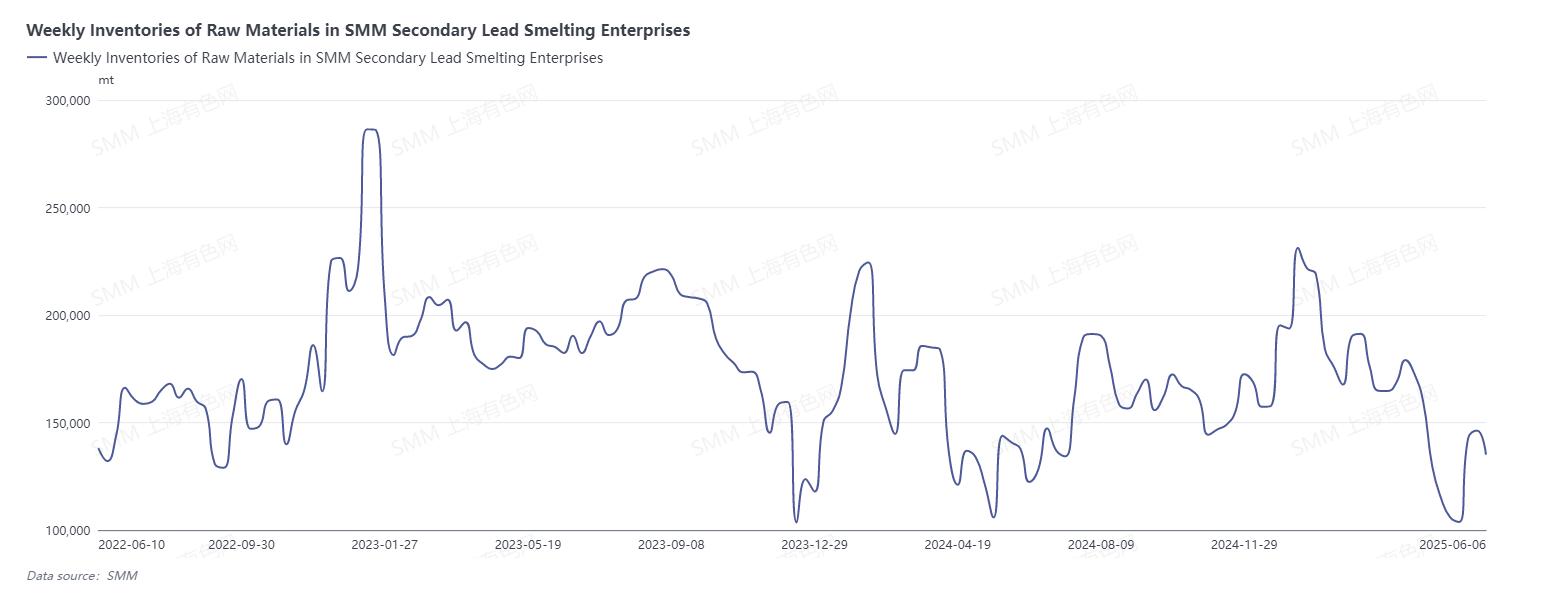

The end-use consumption of lead-acid batteries is the lifeblood of the entire lead industry chain. Currently, weak downstream consumption has led to a low replacement rate of new and old batteries and a small volume of scrap batteries in the market. According to waste lead-acid battery recyclers, the collection volume at storefronts is low, and there is a strong reluctance to sell, resulting in increasing pressure on procurement recently. Some recyclers have even stated that their daily turnover is less than 50% of previous years. Tight supply of raw materials has constrained the production of smelters.

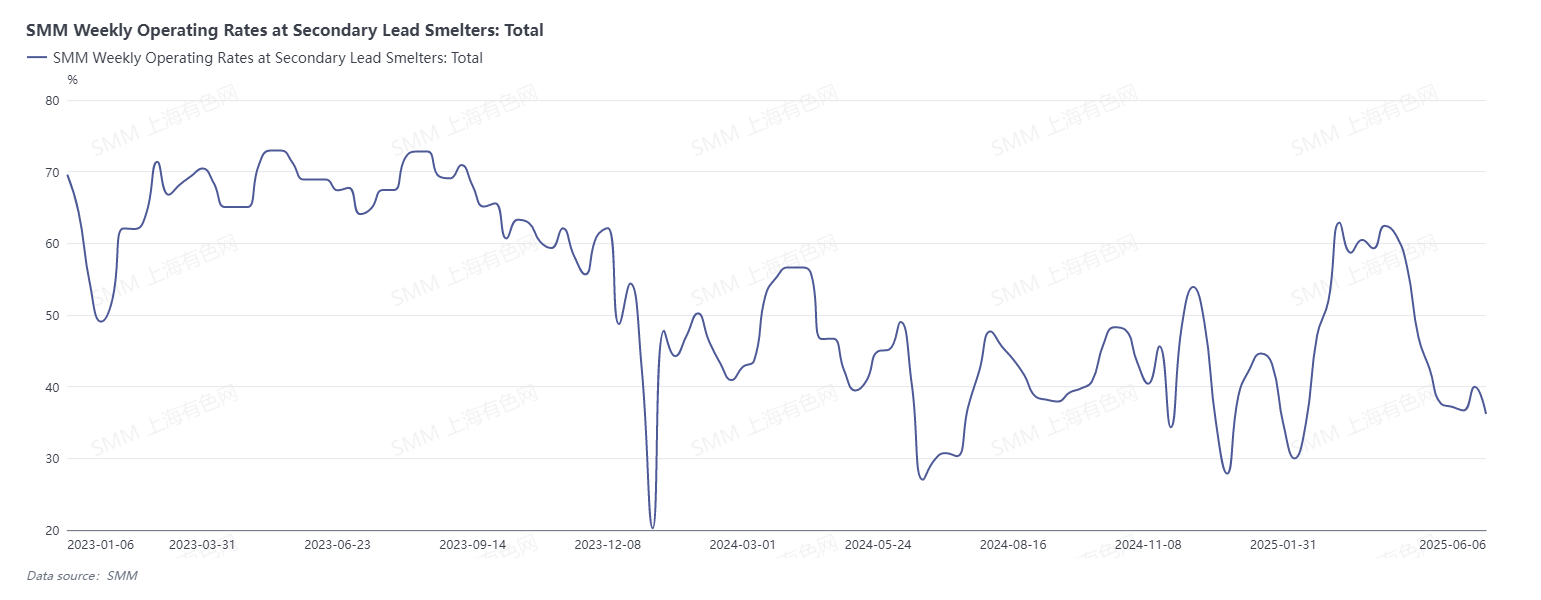

In addition, poor downstream consumption has directly led to weak enthusiasm for lead ingot procurement by lead-acid battery producers. It is reported that the lead ingot procurement volume of a well-known battery producer's production site in north China has dropped by approximately 60% compared to previous years. Amid weak demand, lead ingot suppliers are willing to expand their discounts to sell their products, while secondary lead smelters generally maintain firm quotes due to high costs and significant loss pressures. "Producing more means losing more" has become a mantra for secondary lead smelters, leading to a continuous decline in weekly operating rates.

In May, multiple enterprises in east China, central China, and north China reduced production or halted operations due to raw material constraints or losses from market conditions, with total production cuts exceeding 120,000 mt. In June, with the completion of maintenance and the implementation of production resumption plans, the impact on production is expected to increase by approximately 40,000 mt MoM.

Market sentiment regarding lead consumption in June remains bearish, and the short-term lead fundamentals are unlikely to provide conditions or momentum for lead price increases. If lead consumption in June does not improve significantly, the recovery of secondary lead smelters may exacerbate the market downturn. Of course, given the supply situation of waste lead-acid batteries, the raw material costs for secondary lead smelters are still more likely to rise than fall, and the pressure of losses may suppress their production enthusiasm, leading to lower-than-expected production increases. Overall, the "loss predicament" of secondary lead smelters is likely to persist. Given the current situation of severe overcapacity, as enterprises have said, "producing less means losing less."